The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Prognosfruit 2026 will take place in Constance, Germany, from the 5th to the 7th of August 2026, with a milestone for the event, celebrating 50 years of uninterrupted editions of Prognosfruit. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in Constance, Germany, from the 5th to the 7th of August 2026. Prognosfruit 2026 is organised by WAPA in cooperation with BVEO (Bundesvereinigung der Erzeugerorganisationen Obst und Gemüse e.V.). Registration is now open on the Prognosfruit website.

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season, with a conference organised in a different country each year. In 2026, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 6, the delegates will have the opportunity to participate in juice production and fruit research visits.

“We are proud to host Prognosfruit in one of Europe’s important fruit-growing regions. Lake Constance offers the perfect surroundings to discuss the future of the apple and pear sector.” BVEO Managing Director Dr. Christian Weseloh stated.

The programme of Prognosfruit 2026, the online registration form to attend the conference, and the link to book your accommodation in Constance are all available on the Prognosfruit website. Register by 7 June 2026 to take advantage of the Early Bird Fee and book your accommodation by 22 June 2026 to take advantage of the discount rates for selected hotels in Constance! Due to the “Konstanzer Seenachtfest”, the renowned lakeside festivals taking place on 8 August 2026, the city of Konstanz experiences a high demand for accommodation at the beginning of August.

Overview of Prognosfruit 2026

Wednesday, 5 August 2026: Welcome reception at Castle Mainau, Island of Mainau by Lake Constance

Thursday, 6 August 2026: Prognosfruit 2026 Conference, at the Bodenseeforum Conference Centre in Constance

Thursday, 6 August 2026: Gala Dinner at the Konzil Constance

Friday, 7 August 2026: Technical visits to the Widemann Bodensee-Kelterei in Barmatingen for juice production and to the Kompetenzzentrum Obstbau Bodensee (fruit research station) in Ravensburg/Bavendorf

On the occasion of the Pipfruit Market Observatory of the European Commission, WAPA (World Apple and Pear Association) presented a first update of its 2025/2026 European apple and pear forecast initially released at Prognosfruit in August 2025. The revised figures show a moderate increase in both apple and pear production for this season to reach, respectively, close to 11 million T for apples and slightly above 1.8 million T for pears. This is mainly due to favourable late-summer weather conditions that improved fruit sizes and colouring for mid and late-season varieties. While production is slightly higher than initially expected, total volumes remain well below the full potential of 13 million tonnes for apples and more than 2 million tonnes for pears, confirming for pipfruit a “medium to low” average European 2025/2026 season crop.

This provisional updated estimate brings the EU apple crop from the initial 10.4 million T released in August to reach between 10.9 and 11 million tonnes, about 5 % higher than the initial August forecast. It ranks this year’s crop as the 6th of the decade, and well below the peak crop of 2018 at 13.2 million tonnes. The EU pear crop is now estimated at just over 1.8 million tonnes, slightly higher than August expectations. This marks for pears the third consecutive low crop, and the fourth lowest of the decade, far from the 2010 peak of 2.7 million tonnes.

Following challenging spring conditions with late frost, weak pollination, and early-summer drought, more favourable weather conditions were recorded in September with rains and appropriate temperatures that contributed to improved yields across several Member States. The main revisions include an indicative increase for Poland (+400,000 tonnes), Germany (+60,000 to 80,000 tonnes), Belgium (+20,000 tonnes), the Netherlands (+10,000 tonnes), and France (+20,000 tonnes). Several contributors of Prognosfruit are still updating their figures, including Italy and Austria, as well as the aforementioned countries, upon the final harvesting later in November. For pears, an increase is mainly observed in Belgium (+25,000 T), the Netherlands (+10,000 T), and France (+10,000 T), an increase partially offset by a small further decline in Italy (-9,000 T).

WAPA emphasises that the updated figures reflect normal forecast adjustments as weather developments up to the end of harvesting in November can significantly influence fruit size and yields estimated in August. The organisation underlines that such revisions are part of a transparent and adaptive forecasting process.

“While this year’s crop is slightly higher than initially anticipated, the European apple and pear market remains well balanced,” said Philippe Binard on behalf of Prognosfruit. He added, “Production continues to be below full potential, stocks are clean, and new export openings are providing a positive outlook for the season”.

Although early sales in several countries were slowed by abundant garden production and cautious consumer demand, the market is now moving into full speed, supported by healthy domestic consumption and emerging export opportunities. The EU market observatory, building on some of the findings released at Prognosfruit, underlined some positive parameters for the season development. It is reminded that the season had a clean start with no overlapping stocks nor significant imports. While the intra-EU trade dynamic is not yet at its full potential in key markets such as Germany due to strong local availability, the outlook for intra-EU trade always remains as a safe bank for the sector, next to local sales. Some quality challenges have led to higher volumes being directed to the processing sector, balancing well the fresh market potential and tightening the stocks outlook for the fresh market later in the season. Despite geopolitical headwinds, export volumes are now already in full swing with volume up 20 % year-on-year, buoyed by lower production in Turkey. This is creating opportunities for the EU exporters in the Middle East, India and North Africa (Egypt, Libya) and as well as elsewhere in Southeast Asia or Latin America, despite some exchange rate disadvantages for EU traders, some ongoing market access restrictions, and logistics constraints in the Red Sea.

The apple and pear sector will need to continue mitigating some challenges for positive development, including securing satisfactory prices to fully recover rising production costs, securing a diversified toolbox for yield performance, and addressing emerging biosecurity risks under climate change. It will remain key to stimulate consumption uptake with evolving consumer patterns, availability of appropriate packaging types, and increased competition from other agrifood products and the growth of other fruit categories on supermarket shelves.

Apples and pears remain the lead category in the fruit basket assortment and have a diversity of varieties to offer to consumers throughout the season. The category needs to be properly stimulated by the future vision for agriculture in the EU and the upcoming CAP reform to keep the sector competitive and attractive for the generational shift.

More about the future outlook for the apple and pear sector will be on the agenda of Prongnosfruit 2026, which will take place in Constance (Germany) on 5-7 August 2026.

The new orange juice blend delivers the fresh orange taste families love at a more affordable price point

Tropicana has introduced Tropicana Essentials, a new orange juice blend designed to ease the everyday hustle at a more affordable price point compared to premium orange juices.

Made with a blend of orange, apple and pear juices, Tropicana Essentials is a good source of antioxidant vitamins C and E, calcium and vitamin D and contains no added sugar. The fruit juice is available in three varieties – Orange Blend (No Pulp), Orange Blend (Some Pulp) and Orange Mango Blend (No Pulp).

“Back-to-school season can feel like a marathon, and Tropicana Essentials is exactly what families need to start the morning strong,” said Tina Lambert, chief marketing officer at Tropicana Brands Group. “Tropicana has always been committed to making great-tasting juice accessible to everyone. Tropicana Essentials continues that tradition with a nutritious, delicious, fresh taste at a more affordable price point.”

Tropicana Essentials is available now at major retailers in the US, including Target, Kroger, Albertsons and more, at a suggested retail price of USD 3.89 for a 46-fluid-ounce bottle.

At the Prognosfruit 2025 Conference, the World Apple and Pear Association (WAPA) released its annual forecast for the 2025/2026 season. Apple production across the EU’s top producing countries is expected to remain nearly identical to last year’s volumes, reaching 10.5 million t (-0.1 %), though remaining 7.5 % below the 3- and 5-year average. Golden Delicious, as the main variety of the apple category, will see a minor decrease (-0.9 % to 2.06 million t), while Gala stabilises at 1.43 million t. Red Delicious and Idared are forecast to experience notable drops of -19.2 % and -8.8 % respectively.

On the pear side, EU production is projected to grow by 1.4 % year-on-year to 1.79 million t, though it remains 2.5 % below the 3-year average. Italy’s output is expected to fall again sharply (-24.7 %), offset by substantial increases in Belgium (+32.1 %) and the Netherlands (+8.1 %). Conference pears will rise by +15.6 % to 857,368 t, while William BC production will shrink by -16.7 %.

For both apples and pears, the lower production compared to the previous years’ average reflects ongoing challenges in yield consistency, impacted by climatic havoc, the limited toolbox, the varietal transition towards better but less productive varieties, or the shift to organic.

The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Prognosfruit 2025 will take place in Angers, France, from the 6th to the 8th of August 2025, the first edition in the country since Toulouse in 2012. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in Angers, France, from the 6th to the 8th of August 2025. Prognosfruit 2025 is organised by WAPA in cooperation with ANPP (Association Nationale Pommes Poires). Registration is now open on the Prognosfruit website.

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season, with a conference organised in a different country each year. In 2025, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 7, the delegates will have the opportunity to participate in technical orchard and packhouse visits.

Given its commitment to the environment, particularly through the Eco-Responsible Orchards label, the ANPP has announced that this event will be carbon neutral, with the offsetting to be achieved through orchard plantings.

The programme of Prognosfruit 2025, the online registration form to attend the conference, and a platform to book your accommodation in Angers are all available on the Prognosfruit website.

The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Following last year’s Conference in Budapest, Prognosfruit 2025 will take place in Angers, France, from the 6th to the 8th of August 2025. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in in Angers, France, from the 6th to the 8th of August 2025. Prognosfruit 2025 is organised by WAPA in cooperation with ANPP (Association Nationale Pommes Poires). Registration is now open on the Prognosfruit website.

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season. This year, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 7, the delegates will have the opportunity to participate in technical orchard and packhouse visits.

WAPA Secretary General Philippe Binard stated: “We look forward to welcoming to Angers all apple and pear experts, with whom WAPA has built an established yet ever-growing network to gather and discuss the latest production trends and market developments. In the case of this year’s three-day programme, the analysis of the crop forecast for 2025- 2026 will be complemented by workshops on two key topics for today’s apple and pear sector: processing and sustainability”.

The draft programme of Prognosfruit 2025 and the online registration form to attend the conference are both available on the Prognosfruit website.

On the occasion of its Annual General Meeting in Fruit Logistica, the World Apple and Pear Association (WAPA) has released the Southern Hemisphere apple and pear crop forecast for the upcoming season. According to the forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple production is set to grow by 5,5 % compared to 2024, while the pear crop is expected to decrease by 3,3 %.

On Friday 7 February 2025, the World Apple and Pear Association held its Annual General Meeting. During the Meeting, which took place during Fruit Logistica in Berlin, WAPA presented the Southern Hemisphere apple and pear crop forecast for the upcoming season. This report has been compiled based on figures from Argentina, Australia, Brazil, Chile, New Zealand Apples, and South Africa, and therefore provides consolidated data from the six leading Southern Hemisphere countries.

Regarding apples, the Southern Hemisphere 2025 crop forecast suggests an increase of 5,5 % to a total of 4.746.639 t compared to last year (4.499.328 t). South Africa is expected to maintain its lead as the largest producer with 1.474.767 t (+ 3,4 from 2024), followed by Brazil (950.000 t, + 14,2), Chile (920.000 t, + 0,7 %), New Zealand (544.949 t, + 5,6 %), Argentina (537.000 t, + 5,8 %), and Australia (319.923 t, + 5,5 %). With 1.564.499 t, Gala is by far the most popular variety, with its volume growing by 6,8 % from 2024 although 2,3 % below the average of the previous 3 years. Exports are also expected to increase (+ 5,3 %) to reach 1.653.976 t. South Africa (+ 5,5 %) and Chile (+ 1 %), the two largest exporters, are both expected to increase their export volumes, reaching 641.488 t and 507.000 t respectively. Exports from New Zealand should grow by 9,7 % (376.106 t in total), with growing export quantities also forecasted for Argentina (90.000 t, + 8,2 %) and Brazil (36.547 t, + 14,6 %).

Regarding pears, the Southern Hemisphere growers predict a slight decline in the crop (- 3,3 %), bringing the total to 1.446.970 t. Argentina (616.000 t), the largest producing country, is expected to decrease its volumes by 10,9 %. South Africa (551.642 t), Chile (208.025 t), and Australia (62.467 t), on the other hand, are all expected to increase their production by 2,9 %, 3 %, and 4,2 % respectively. Packham’s Triumph remains the most produced variety (601.322 t, despite a 2,7 % decrease compared to 2024), followed by Williams’ bon chrétien pears (288.729 t). Export figures are also expected to decrease from 2024, with a total of 689.155 t (- 4,4 %).

The EU production forecast, which was first published during Prognosfruit 2024, was revised to 10.388.550 t (down 9,7 % from 2023) for apples and 1.792.839 t (+ 5,1%) for pears. European apple stocks stood at 3.687.100 t as of 1 January 2025, which is 4,3 % lower than in 2024. On the other hand, the total of 608.544 t for European pears is 4,5 % above the figures from the previous year. The US apple forecast for 2024 stood at 5.376.986 t (- 2,3 % from 2023), while the pear volumes were updated to 390.128 t (- 21,5 %). Stock figures in the USA were 3,9 % lower than in 2024 for apples (2.053.915 t) and 26 % lower for pears (106.100 t).

The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Following last year’s successful return to Trentino, Prognosfruit 2024 will take place in Budapest, Hungary, from the 7th to the 9th of August 2024. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website. Prognosfruit 2024 is organised by WAPA in cooperation with FruitVeB (Magyar Zöldség- Gyümölcs Szakmaközi Szervezet).

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season. This year, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 8, the delegates will have the opportunity to participate in a technical visit at Rauch’s processing factory in Budapest.

WAPA Secretary General Philippe Binard stated: “We look forward to welcoming the apple and pear experts and providing the opportunity for the sector representatives to gather and discuss the latest developments of the market. This year’s three-day programme, in addition to the crop forecast for 2024-2025, will focus in particular on strategies to promote the consumption of apples and pears and on the outlook for the processing industry”.

The draft programme of Prognosfruit 2024 and the online registration form to attend the conference are both available on the Prognosfruit website.

Pear orange prices in the in natura market hit a new record in February, considering Cepea historical series, which has started in October 1994 – values were deflated by IGP-DI December/23. Quotations are likely to continue at high levels in March, since the volume of early varieties in the spot market in São Paulo is still small.

In February, pear orange prices averaged BRL 87.40 per 40.8-kilo box, on tree, 9.29 % up compared to January/24 and an increase of 83 % in relation to February/23 (in this case, in nominal terms). Price rises are linked to the lower supply in this offseason period, while the supply of late and early varieties is also limited. It is worth noting that the firm industrial demand reduced even more the fruit availability in the domestic market during the entire season.

TAHITI LIME – Prices have started February in a downward trend; however, they rose during the month, leading to an increase of the monthly average. Although it is the peak season, frequent rains limited the harvest and, consequently, the supply. Moreover, weather conditions have been favoring the fruit quality.

In this scenario, the tahiti lime price average in the in natura market was BRL 20.11 per 27-kg box (harvested) in February, moving up 46.36 % and 104 % in relation to January/24 and February/23, respectively, in nominal terms.

Values are likely to remain firm in March because of the lower volume that will be harvested. Moreover, exports may increase, especially due to the proximity of Easter, which can influence to flow the product.

On the occasion of its Annual General Meeting in Fruit Logistica, the World Apple and Pear Association (WAPA) has released the Southern Hemisphere apple and pear crop forecast for the upcoming season. According to the forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple production is set to grow by 1,1 % compared to 2023, while the pear crop is expected to decrease by 2,3 %.

On Friday 9 February 2024, the World Apple and Pear Association (WAPA) held its Annual General Meeting. During the Meeting, which took place during Fruit Logistica in Berlin, WAPA presented the Southern Hemisphere apple and pear crop forecast for the upcoming season. This report has been compiled with the support of CAFI (Argentina), APAL (Australia), ABPM (Brazil), Fruits from Chile (Chile), New Zealand Apples and Pears (New Zealand), and Hortgro (South Africa), and therefore provides consolidated data from the six leading Southern Hemisphere countries.

Regarding apples, the Southern Hemisphere 2024 crop forecast suggests an increase of 1,1 % to a total of 4.775.530 t compared to last year (4.725.574 t). South Africa is expected to maintain its lead as the largest producer with 1.396.659 t (+ 4,6 from 2023), followed by Brazil (1.100.000 t, in line with 2023), Chile (912.000 t, – 8,4 %), New Zealand (557.871 t, + 14,7 %), Argentina (501.000 t, – 4,8 %), and Australia (308.000 t, + 5,8 %). With 1.578.148 t, Gala is by far the most popular variety, with its volume remaining in line with 2023 although 11,4 % below the average of the previous 3 years. Exports are also expected to increase (+ 8 %) to reach 1.551.696 t. South Africa (+ 5,1 %) and Chile (+ 5,3 %), the two largest exporters, are both expected to increase their export volumes, reaching 572.280 t and 493.000 t respectively. Exports from New Zealand should grow by 22,2 % (381.729 t in total), while lower export quantities are forecasted for Argentina (70.000 t, – 4,1 %) and Brazil (32.000 t, – 10,6 %).

Regarding pears, the Southern Hemisphere growers predict a slight decline in the crop (- 2,3 %), bringing the total to 1.465.800 t. Argentina (614.000 t), Chile (203.000 t), and Australia (72.000 t) are expected to decrease their production by 6 %, 5,4 %, and 2,7 % respectively. South Africa’s production levels are forecasted to increase to 567.334 t (+ 3,4 % from 2023), as well as New Zealand’s (+ 8,4 %, with 9.066 t in total). Packham’s Triumph remains the most produced variety (508.000 t, with a slight 1,3 % decrease compared to 2023), followed by Williams’ bon chrétien pears (300.082 t). Export figures are expected to be in line with 2023 with a total of 654.323 t.

European apple stocks stood at 3.851.098 t as of 1 January 2024, which is 4,6 % lower than in 2023. Similarly, the total of 582.587 t for European pears is 4,4 % below the figures from the previous year. On the other hand, stock figures are higher in the USA, both for apples (2.138.376 t, + 33,6 %) and for pears (169.474 t, + 14,9 %).

During the Annual General Meeting, Jeff Correa (Pear Bureau Northwest – USA) was elected as the President of the association, taking over from Dominik Woźniak (Society for Promotion of Dwarf Fruit Orchards / Rajpol – Poland). Nick Dicey (Hortgro – South Africa) will join him as the Vice-President. Regarding his new role, Mr Correa commented: “I’m honoured that I have been elected as the next Chairman of WAPA. I look forward to working with the WAPA staff and membership to advance the data sharing, market insights, and explore new avenues that will benefit the organization and its members”. Finally, the Annual General Meeting confirmed that the next edition of Prognosfruit will be held in Budapest, Hungary, on 7-9 August 2024.

With the first part of this year’s harvesting on its way, the World Apple and Pear Association (WAPA) has started revising its annual Apple and Pear Crop Forecast based on the latest insights from its members on the season. The first EU apple estimates, which were released on 3 August 2023 during the Prognosfruit Conference, indicated a 3,3 % decrease compared to last year, to a total of 11.410.681 t. The EU pear crop for 2023 was estimated to decrease by 12,9 % compared to last year’s crop with a total of 1.745.632 t.

The early forecast is released during Prognosfruit, when harvesting is just about to start. The crop can therefore still be impacted by nature and climatic factors up to late October, with either a positive or negative impact on the quantity and quality of the harvest. Historically, these adjustments to the forecast amounted to small percentage variations.

The first updates from Prognosfruit’s network of national producing associations indicate that climate change- related conditions negatively affected the crop in the weeks following the publication of the original estimates. The climatic havoc included droughts, floodings, hail, warm nights, and an increased risk of pests across the EU. In other cases, rains and colder nights have positively impacted the size development and colouring respectively in some producing regions.

Regarding this season, while the apple harvesting is still expected to carry on for several weeks, based on the first regional adjustments (both upward and downward) WAPA estimates that the 2023 apple crop is expected to settle at just below 11 million t (about 4 % lower than the original forecast).

In regard to pears, a further decline of the forecast in Italy, Spain, Belgium, and the Netherlands will lead to a lower crop, even lower than in 2021. The final pear crop is expected to be around 1.720.000 T, about 6 % lower than the initial forecast.

WAPA will continue to monitor closely the harvesting developments in Europe, with the objective of consolidating the most accurate and recent figures into its final Crop Forecast later this year once harvesting is completed.

The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Following last year’s successful return as an in-person event, Prognosfruit 2023 will take place in Trentino, Italy, from the 2nd to the 4th of August 2023. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in Trentino, Italy, from the 2nd to the 4th of August 2023. Prognosfruit 2023 is organised by WAPA in cooperation with APOT (Associazione Produttori Ortofrutticoli Trentini). Registration is now open on the Prognosfruit website.

Alessandro Dalpiaz (APOT) commented on the event’s return to Trentino: “We are honoured to host in Trentino the most important international conference dedicated to apples and pears. Prognosfruit is certainly an important opportunity to present to the participants the ability of an organised system to deal with environmental issues, geopolitical crises, and market uncertainties. Prognosfruit also represents an occasion to bring the attention of the participants to those understated yet relevant values of mountain areas, with their arts, traditions, stories, and landscapes that attract and make millions of visitors think every year”.

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season. This year, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 3rd, the delegates will have the opportunity to participate in technical and cultural visits to Melinda’s Underground Warehouses, San Romedio Sanctuary, and Valer Castle.

WAPA Secretary General Philippe Binard stated: “Last year’s edition reminded us all how important Prognosfruit and its three-day programme are for the apple and pear sector. Prognosfruit provides the opportunity for the delegates to meet up and discuss the latest developments and the future of the market, which is especially important in challenging times like the ones the sector is currently dealing with”.

The draft programme of Prognosfruit 2023 and the online registration form to attend the conference are both available on the Prognosfruit website.

FoodTech venture fund Sparkalis has taken a minority stake in Fooditive, a next-gen food technology business specialising in sustainable plant-based ingredients. Fooditive’s innovations include an upcycled calorie-free natural sweetener with the taste and functionality of sugar, which is derived from apple and pear side streams.

Following the investment, Sparkalis Managing Director Filip Arnaut has joined Fooditive’s advisory board. There are now 11 foodtech experts sitting on the board. They will provide advice and insights to support Fooditive’s mission to create plant-based ingredients that are healthier for consumers, better for the planet and kinder to animals.

Fooditive, based in the Netherlands, has risen to prominence for successfully harnessing its precision fermentation technology to produce groundbreaking innovations such as vegan casein and bee-free honey. It also recently became the first food industry signatory to the Washington Compact, a new agreement on conducting business operations in outer space.

About Fooditive BV Based in Rotterdam, The Netherlands, Fooditive is a plant-based ingredient manufacturer committed to making healthy food available for all with its 100% natural ingredients. Since it was established in 2018, Fooditive has used its unique fermentation process to create a world-renowned sweetener, made from side-streams of apples and pears. The sweetener’s unique approach provides not only taste but also functionality and a sustainable impact. As the world begins to recognize the value in veganism and sustainability, Fooditive has also recently launched a new plant-based protein that can be used in the food industry to replace dairy in food and beverage applications.

About Sparkalis Sparkalis is an independent corporate venture fund, and a sister company of PURATOS, the global leader in the B2B bakery, patisserie and chocolate sectors. Sparkalis’s mission is to work with start-up founders, innovative and business-driven entrepreneurs to transform exciting ideas into successful business realities. Sparkalis is committed to investing in innovative solutions to create, with future partners, a healthier and better ‘food print’ for today’s and tomorrow’s generations around the world.

Prognosfruit’s 2022 European apple and pear crop forecast reveals that apple production is set to increase by 1 % compared to 2021, while the upcoming pear crop is estimated to increase by 20 % compared to last year’s record low crop of the decade and by 5 % compared to the 3-year average. On 4 August 2022, more than 200 international representatives from the apple and pear sector joined Prognosfruit 2022 in Belgrade, Serbia, the first in-person Prognosfruit event after two online editions, to discuss the 2022 production forecast for apples and pears.

The World Apple and Pear Association (WAPA) released the 2022/2023 European apple and pear crop estimate on the occasion of the 47th edition of the Prognosfruit, which took place on August 3-5 in Belgrade, Serbia, returning as an in-person event after two years of online editions. Philippe Binard stated: “The apple production in the EU27 and UK is estimated to increase by 1 % to reach 12.167.887 T compared to last year. This year’s crop is also forecasted to be 9 % above the average of 2019-2020- 2021”. The European crop continues its adaptation to the varieties and quality specifications demanded by consumers. Dominik Wozniak, President of WAPA, indicated: “The prospects for the upcoming season are positive, although the sector will have to be prepared to face a variety of challenges including significant rising costs impacting the competitiveness of the sector, intense weather conditions, logistical issues, inflation, and difficulty to secure seasonal workers, with the ultimate goal of increasing consumption thanks to the quality of the products of the season and reverse the recent negative trend”.

Philippe Binard added: ”The EU pear crop for 2022 is estimated to increase by 20 % compared to last year’s record low crop of the decade and by 5 % compared to the 3-year average, rising to 2.077.000 T, mainly due to Italy and France more than doubling their production compared to 2021 (reaching 473.690 T and 137.000 T respectively), although, in the case of the former, the crop remains below its full potential.”. WAPA will continue to monitor the developments of the Northern Hemisphere crop and will issue updates when available.

The 2022 Prognosfruit Conference gathered more than 200 apple and pear sector experts from 23 countries. The event, organised by WAPA and Serbia Does Apples, featured the forecast and market analysis for the European apple and pear market as well as an overview of the latest trends in processing, organic, and the cider market. Luc Vanoideek (COPA COGECA-VBT) commented: “ The Belgrade meeting was the ideal opportunity to learn more about the development in the EU neighbourhood, including Serbia, Moldova, Ukraine, Turkey, as well as the Central Asia and Caucasus region” He further explained: “The additional contributions from representatives of China, India, and the USA provided to the conference a global outreach with the full picture of the whole Northern Hemisphere crop forecast.”

Prognosfruit is the compass for the apple and pear sector. Philippe Binard concluded: “The strong attendance at this first in-person Prognosfruit Conference after two years of online meetings is a clear sign that the sector representatives also very much appreciate the sense of community and networking opportunities that Prognosfruit provides. We look forward to continuing this tradition next year in Trento, Italy from 2 to 4 August 2023”.

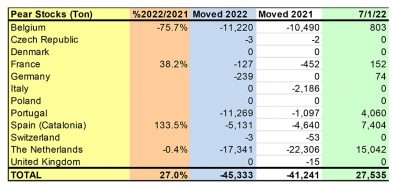

WAPA, the World Apple and Pear Association, has released the apple and pear stock figures from 1 July 2022. The figures show that in Europe apple stocks increased by 16.5 % compared to 2021 to reach 535,521 T, while pear stocks increased by 27 % to 27,535 T. In the USA, pear stocks reached 10,403 T (75.2 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 535,521 T as of 1 July 2022, which is 16.5 % above the figure of 2021. This trend can be explained by the increases concerning Jonagold (108.4 % up from 2021), Gala (+ 29.4 %), Red Jonaprince (+ 25.3 %), and Golden Delicious (+ 13 %), although several varieties reported a decrease compared to 2021, most notably Gloster, which halved its stocks compared to 2021 and Granny Smith (- 33.8 %). Pear stocks stood at 27,535 T on 1 July 2022, 27 % above the volume of 2021 thanks to Rocha (+ 4,060 T compared to 2021) and Conference pears (+ 1,970 T). Pears stocks in the USA stood at 10,403 T (75.2 % above 2021), with Anjou pears reaching 9,223 T and Red Anjou pears also increasing from 2021 ( + 957 T).

European pear stocks (Photo: WAPA)US pear stocks (Photo: WAPA)

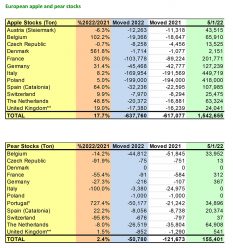

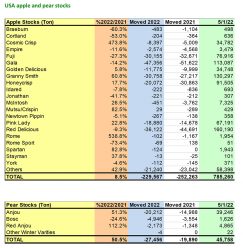

WAPA, the World Apple and Pear Association, released the apple and pear stock figures from 1 May 2022. The figures show that in Europe apple stocks increased by 17.7 % compared to 2021 to reach 1,542,655 T, while pear stocks increased by 2.4 % to 155,401 T. In the USA, apple stocks as of 1 May 2022 stood at 785,260 T (+8.5 % compared to 2021), while pear stocks reached 45,758 T (50.5 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 1,542,655 T as of 1 May 2022, which is 17.7 % above the figure of 2021. This trend can be explained by the increases concerning Red Jonaprince (65.6 % up from 2021), Gala (+ 56.1 %), Jonagold (+ 40.8 %), and Golden Delicious (+ 27.7 %), although several varieties reported a decrease compared to 2021, most notably Gloster (- 71.3 %) and Granny Smith (- 19.8 %). On the other hand, pear stocks stood at 155,401 T on 1 May 2022, 2.4 % above the volume of 2021. While the Italian varieties were down to zero, Portugal’s Rocha pears increased substantially (+ 30,678 T above 2021’s levels).

European apple and pear stocks (Photo: WAPA)

In the USA, apple stocks in May stood at 785,260 T (+ 8.5 % compared to 2021). Cosmic Crisp (+ 473.8 % compared to 2021), Granny Smith (+ 60.8 %), and Pink Lady (+ 22.8 %) compensated for the decrease in several major varieties, such as Fuji (- 27.3 %) and Red Delicious (- 9.3 %). Pears stocks in the USA stood at 45,758 T, which is 50.5 % above last year, with Anjou pears increasing by 51.3 %.

USA apple and pear stocks (Photo: WAPA)

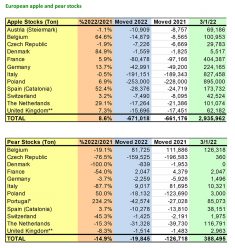

WAPA, the World Apple and Pear Association, released the apple and pear stock figures from 1 March 2022. The figures show that in Europe apple stocks increased by 8.6 % compared to 2021 to reach 2,935,962 T, while pear stocks decreased by 14.9 % to 388,495 T. In the USA, apple stocks as of 1 March 2022 stood at 1,275,346 T (+ 1.6 % compared to 2021), while pear stocks reached 111,912 T (37.7 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 2,935,962 T as of 1 March 2022, which is 8.6 % above the figure of 2021. This was mainly driven by the increases concerning Red Jonaprince (54 % up from 2021), Jonagold (+ 27.9 %), Golden Delicious (+ 23.3 %), and Gala (+ 18.4 %), and despite the decrease in some major varieties, including Granny Smith (- 20 %) and Cripps Pink (- 14.9 %). On the other hand, pear stocks stood at 388,495 T on 1 March 2022, 14.9 % below the volume of 2021. The decrease in the Italian varieties (Abate Fetel – 97.8 % and Kaiser – 95.2 %) was partially mitigated by the stark increase in Portugal’s Rocha pears (+ 59,614 T compared to March 2021).

In the USA, apple stocks in March stood at 1,275,346 T (+ 1.6 % compared to 2021). The decrease among several large varieties, such as Fuji (- 20.8 %), Red Delicious (- 11.7 %), and Gala (- 9 %) was compensated by the 216.5 % increase in Cosmic Crisp apples, which reached 51.576 T, and the 36.5 % increase in the Granny Smith variety. Pears stocks in the USA stood at 111,912 T, which is 37.7 % above last year.

European apple and pear stocks (Photo: WAPA)

USA apple and pear stocks (Photo: WAPA)

Fooditive, a pioneer in developing plant-based ingredients, is gearing up for a game-changer in the industry: a Novel Food licence from the European Food Safety Authority (EFSA) for its sweetener. The Dutch company has developed from a concept to a company worth of 26 million euros in 2022 and is making significant progress. Founded on the belief that sustainability is more than a trend, Fooditive provides innovative and natural ingredients to food and beverage manufacturers.

The company’s unique process allows them to develop a remarkable sweetener, made from side streams of apples and pears. The production process has been enhanced and evolved from batch to continuous fermentation, to be able to deliver on the high demand from the food industry by producing up to 30 tonnes of sweetener per week. For this purpose, 83 tonnes of apples and pears are being upcycled, raw material that is considered as side streams, third-grade by juice manufacturers or simply the “ugly fruit”.

The sweetener – the first of Fooditive’s cutting-edge products – sparked a sugar-free, plant-based revolution. The company hopes to make a ground-breaking step towards establishing the sweetener in the market by forming a successful collaboration with a production partner in the Netherlands.

Fooditive has already been offering the sweetener for research and development purposes to players in the food industry to determine which applications their sweetener performs best in. After three years’ worth of learning and development, feedback, and support from the food industry, the company will submit the sweetener as 5-D-Keto-Fructose in the process of applying for Novel Food certification from the European Food Safety Authority.

Global competitor

Following the recent study by ReportLinker, Fooditive is the only start-up and Dutch company that is considered as one of the global competitors for food sweeteners in the industry competing alongside with several of the leading ingredient market vendors. Fooditive provides an innovative sweetener to companies, for different product applications where it can deliver not only the sweet taste but also the functions of sugar.

The sweetener is developed from the extraction of fructose through fermentation and its conversion to 5-D-Keto-Fructose through bio-refining techniques. Fooditive has accomplished this through its innovative approach to offer solutions by valorizing side-streams and starting from different raw materials, including cherries and bananas, to transform them into valuable, healthy ingredients.

Exciting journey

The Fooditive team is aware that the road ahead will be long and challenging. However, they know that completing its goal of securing EFSA approval for such a unique ingredient comes with a slew of benefits. Investors, venture capitalists, food attorneys, and consultants are invited to join the company’s journey on this effort to deliver this game-changer to the market.

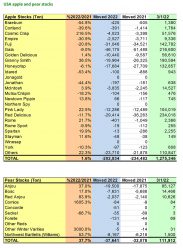

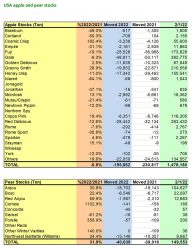

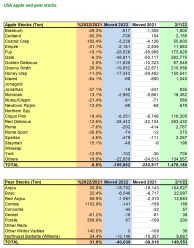

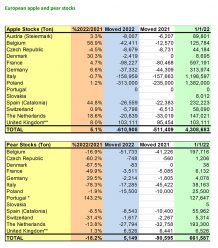

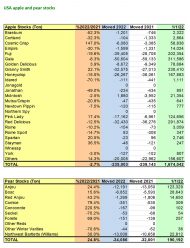

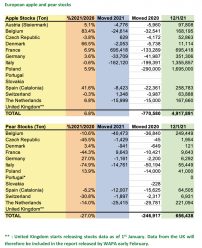

WAPA, the World Apple and Pear Association, released today the apple and pear stock figures from 1 February 2022. The figures show that in Europe apple stocks increased by 7.2 % compared to 2021 to reach 3,606,980 T, while pear stocks decreased by 30 % to 408,340 T. In the USA, apple stocks as of 1 February 2022 stood at 1,478,180 T (- 0.8 % compared to 2021), while pear stocks reached 149,553 T (31.9 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 3,606,980 T as of 1 February 2022, which is 7.2 % above the figure of 2021. This was mainly driven by the increases concerning Red Jonaprince (35.9 % up from 2021), Golden Delicious (+ 22.5 %), Gala (+ 19.9 %), and Jonagold (+ 17.2 %), while several varieties decreased, including Cripps Pink (- 17.3 %) and Granny Smith (- 13.2 %). On the other hand, pear stocks stood at 408,340 on 1 January 2022, 30 % below the volume of 2021, mostly because of the large decrease in Italy (- 83.2 %).

In the USA, apple stocks in January stood at 1,478,180 T (down 0.8 % compared to 2021). The overall stability is due to the fact that Granny Smith’s 26.9 % increase over 2021 compensated for the decrease among several large varieties, such as Fuji (- 19.1 %), Red Delicious (- 12.6 %), and Gala (- 9.3 %). Pears stocks in the USA stood at 149,553 T, which is 31.9 % above last year.

(Photo: WAPA)(Photo: WAPA)

On the occasion of its Annual General Meeting, the World Apple and Pear Association (WAPA) has released the Southern Hemisphere apple and pear crop forecast for the upcoming season. According to the forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple and pear production is estimated to decrease by 7 % and 6 % respectively in 2022 compared to the previous year.

On 24 February 2022, on the occasion of its Annual General Meeting, the World Apple and Pear Association (WAPA) has released its 2022 apple and pear crop estimate for the Southern Hemisphere. This report has been compiled with the support of ASOEX (Chile), CAFI (Argentina), ABPM (Brazil), Hortgro (South Africa), APAL (Australia) and New Zealand Apples and Pears, and therefore provides consolidated data from the six leading Southern Hemisphere countries. WAPA’s Secretary General Philippe Binard commented “This forecast is released for the global apples and pears sector on the background of many uncertainties, including the geopolitical tension, the increasing costs for production, the impact of the rise of logistic costs and limited container availability, labour shortage and the increasing concerns of declining consumption due to economic situation”

The 2022 Southern Hemisphere apple crop forecast suggests a decrease of 7 % to a total of 4.864.000 T compared to last year (5.217.000 T), mainly due to the 30 % decrease in Brazil and the 11 % decrease in Argentina. Australia and Chile are also forecasted to decrease their production by 3 % and 2 % respectively. New Zealand and South Africa are the only countries where apple production is expected to increase (15 % and 4 % respectively). Chile is expected to remain the largest Southern Hemisphere apple producer in 2022 (1.455.000 T), followed by South Africa (1.163.000 T), Brazil (900.000 T), New Zealand (590.000 T), Argentina (445.000 T), and Australia (311.000 T). With 1.706.000 T, Gala remains by far the most popular variety, although its production is expected to decrease by 7 % compared to 2021. Despite the decrease in production, exports are forecasted to remain stable overall at 1.744.762 T, with the larger volumes exported by New Zealand (+ 17 %) and South Africa (+ 6 %) compensating for the 65 % decrease in Brazilian apple exports.

Regarding pears, the Southern Hemisphere growers predict a 6 % decrease of the crop, which will drop to 1.229.000 T. This is mainly due to the 13 % decrease in Argentina, the 11 % decrease in Chile, and the 6 % decrease in Australia. New Zealand and South Africa, on the other hand, are expected to increase their production by 31 % and 5 % respectively. Argentina remains the largest producer in the Southern Hemisphere (522.000 T), followed by South Africa (492.000 T), Chile (122.000 T), Australia (81.000 T), and New Zealand (11.000 T). Packham’s Triumph remains the most produced variety (444.000 T, despite a 4 % decrease compared to 2021), followed by Williams’ bon chrétien pears (306.000 T). Export figures are expected to decrease by 6 % compared to 2021 to a total of 641.207 T, mainly because of a 14 % decrease in Argentinian exports.

In the Northern Hemisphere, the stocks in the USA stood at 1.478.180 T (- 1 % compared to last year) for apples and 149.553 T for pears (+ 32 % compared to last year) on the 1st of February. In Europe, apple and pear stocks stood at 3.606.980 T (7 % up from last year) and 408.340 T (30 % down from last year). Philippe Binard commented: “Season developments clearly demonstrate the impact of logistics and costs on international trade also for Northern Hemisphere suppliers, with the USA concentrating sales for apples and pears in North America. European markets continue to be affected by the Belarus embargo, while the recent developments in Ukraine will also impact sales to all the destinations in Eastern Europe, including Russia, for all global apples and pears suppliers. It is important to continue building efforts to stimulate the consumption”. WAPA’s Annual General Meeting also hosted a discussion on CO2 emissions and how apple and pear production can reach carbon neutrality or even have a positive contribution to the environment. WAPA will continue to cooperate on this topic with its members in a dedicated working group based on the input and expertise of the University of Bolzano (Italy).

Finally, the Annual General Meeting also confirmed that Prognosfruit will return as an in-person event in the first half of August 2022 in Belgrade (Serbia). The exact date of the event will soon be announced.

WAPA, the World Apple and Pear Association, released the apple and pear stock figures from 1 February 2022. The figures show that in Europe apple stocks increased by 7.2 % compared to 2021 to reach 3,606,980 T, while pear stocks decreased by 30 % to 408,340 T. In the USA, apple stocks as of 1 February 2022 stood at 1,478,180 T (- 0.8 % compared to 2021), while pear stocks reached 149,553 T (31.9 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 3,606,980 T as of 1 February 2022, which is 7.2 % above the figure of 2021. This was mainly driven by the increases concerning Red Jonaprince (35.9 % up from 2021), Golden Delicious (+ 22.5 %), Gala (+ 19.9 %), and Jonagold (+ 17.2 %), while several varieties decreased, including Cripps Pink (- 17.3 %) and Granny Smith (- 13.2 %). On the other hand, pear stocks stood at 408,340 on 1 January 2022, 30 % below the volume of 2021, mostly because of the large decrease in Italy (- 83.2 %).

In the USA, apple stocks in January stood at 1,478,180 T (down 0.8 % compared to 2021). The overall stability is due to the fact that Granny Smith’s 26.9 % increase over 2021 compensated for the decrease among several large varieties, such as Fuji (- 19.1 %), Red Delicious (- 12.6 %), and Gala (- 9.3 %). Pears stocks in the USA stood at 149,553 T, which is 31.9 % above last year.

(Photo: WAPA)

(Photo: WAPA)

WAPA, the World Apple and Pear Association, released the first apple and pear stock figures of 2022. The figures show that in Europe apple stocks increased by 5.1 % compared to 2021 to reach 4,308,683 T, while pear stocks decreased by 18.2 % to 661,587 T. In the USA, apple stocks as of 1 January 2022 stood at 1,674,042 T (- 2.7 % compared to 2021), while pear stocks reached 190,192 T (24.8 % above 2021).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 4,308,683 T as of 1 January 2022, which is 5.1 % above the figure of 2021. This increase was mainly driven by Golden Delicious (up 19.5 % from 2021), Jonagold (+ 15.8 %), and Gala (+ 15.7 %), which compensated for the decrease in several varieties, most notably Granny Smith (- 12.5 %) and Cripps Pink (- 11 %). On the other hand, pear stocks stood at 661,587 on 1 January 2022, 18.2 % below the volume of 2021, mostly because of the large decrease in Italy.

In the USA, apple stocks in January stood at 1,674,042 T, down 2.7 % compared to 2021. This is due to a decrease among the largest varieties, such as Fuji (- 19.6 %), Honeycrisp (- 15.5 %), Red Delicious (- 12.5 %), and Gala (- 8.3 %), and despite significant increases for Cosmic Crisp (+ 147 %) and Pink Lady (+ 17.4 %). Pears stocks in the USA stood at 190,192 T, which is 24.8 % above last year.

(Photo: WAPA)

(Foto: WAPA)

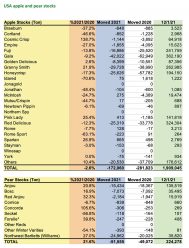

WAPA, the World Apple and Pear Association, released the first apple and pear stock figures of the season. The figures show that in Europe apple stocks increased by 6,8 % compared to 2020 to reach 4,917,891 T, while pear stocks decreased by 27 % to 656,438 T. In the USA, apple stocks as of 1 December 2021 stood at 1,909,045 T (- 2,6 % compared to 2020), while pear stocks reached 224,278 T (21,6 % above 2020).

WAPA, the World Apple and Pear Association, collects every month the stock figures for apples and pears from Europe and the United States. WAPA can reveal that European apple stocks stood at 4,917,891 T as of 1 December 2021, which is 6,8 % above the figure of 2020, which reflects the 11 % increase in the crop. On the other hand, pear stocks stood at 656,438 T on 1 December 2021, 27 % below the volume of 2020, mostly because of the large decrease in Italy. In Europe, the final pear crop is 26 % lower than a year ago. For the USA, apple stocks in December stand at 1,909,045 T, down 2,6 % compared to 2020. This level is reflecting the lower crop in Washington States this year, which stands at just below 3.000,000 T, 4 % less than last year. Pears stocks in the USA stand at 224,278 T, which is 21,6 % above last year.

European apple and pear stocks (Photo: WAPA)

USA apple and pear stocks (Photo: WAPA)

WAPA, the World Apple and Pear Association, released the updated Northern Hemisphere Apple and Pear Crop Forecast. As crops have now been fully harvested since the first figures were released in August 2021, minor adjustments were made in different countries, although the new estimates are still in line with the original forecast. As the Northern Hemisphere season is getting into full swing, stocks depletion figures will be provided as well by the Association.

During the month of December, WAPA has been consolidating the forecast of apples and pears production for the Northern Hemisphere released during the month of August. As the season is now in full swing and harvest is completed, WAPA is reporting on the latest development for apples and pears in the Northern Hemisphere, while already looking to prepare the Southern Hemisphere 2022 forecast, which will be announced during the last week of February on the occasion of the WAPA Annual General Assembly. Overall, the countries survey by WAPA covers a production of 81 Mio T of apples and 23 Mio T of pears.

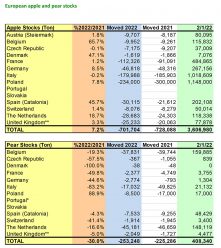

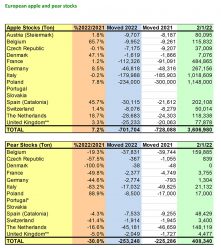

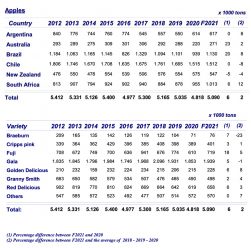

The updated estimates for European apple production of the 21 top EU producing countries and the United Kingdom increased by 160.000 T to stand at 11.895,000 T, which is 1,36 % more than what originally forecasted at 11.735,000 T. The forecast for the season is ultimately 11 % (or 1.195,000 T) up from the last year. The new figure is influenced by an increase in Poland (+ 130.000 T to 4,3 Mio T) as well as in Belgium (+ 48.000 T to 240.000 T) and Austria (+ 5.000 T to 120.000 T) but compensated by a decrease in France (- 12.000 T to 1.363.000 T) and the Netherlands (- 5.000 T to 245.000 T). Italy remains stable at 2.044.000 T, with 2.000 T less compared to the initial forecast of August. On the varieties side, the main changes concern Red Jonaprince (+ 53.000 T to 475.000 T), Jonagold (+ 26.000 T to 444.000 T), Idared (+ 24.000 T to 709.000 T), Red Delicious and Pinova (+ 14.000 T each, reaching 654.000 T and 197.000 T respectively), and Cripps Pink (+ 7.000 T to 240.000 T). On the other hand, Gala decreased (- 10.000 T to 1.553.000 T). Other EU countries and Switzerand represent around 200.000 T. In the USA, the apple crop is confirmed to be stable at 4,644.000 T (6 % down to last year), despite some readjustment within the breakdown by states and varieties. The major varieties in the USA are Gala (863.000 T), Red Delicious (625.000 T), and Honey Crisps (542.000 T). Varietal shift continues in the US orchards, with positive development with new varieties such as Ambrosia and Cosmic Crisp. In the US neighbourhood, Mexico’s production in 2021 was down by 2 % at 700.000 T, while Canada’s production dropped 11 % to 360.000 T. The Chinese apple crop was estimated in August just below 45 Mio T, dominated by the Shaanxi (12,5 Mio T) and Shandong (9,5 Mio T) provinces, which together account for close to 50 % of the Chinese apples production. The crop in EU neighbourhood was set at 8 Mio T, covering Turkey (4 Mio T), Russia (1,4 Mio T), Ukraine (1,3 Mio T), Moldova (600.000 T), Serbia (535.000 T), and North Macedonia (140.000 T). In Central Asia, the apple crop is around 2,5 Mio T, out of which 50 % is in Uzbekistan (1.250.000 T), followed by Azerbaijan (300.000 T), Tajikistan (250.000 T), Kazakhstan (200.000 T), and Kyrgystan (150.000 T). Production in India is forecasted at 2,65 Mio T. In the Southern Hemisphere, the final apple crop was set at 5.230.000 T.

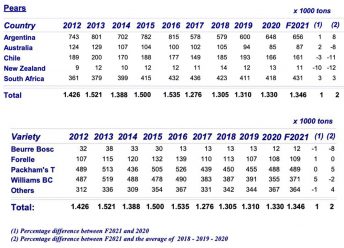

In regard to pears, the European pear production is estimated to reach 1.666,000 T in 2021/2022, which is 3,87 % (or 61.000 T) above the August forecast. This increase is resulting from an increase in Belgium (+ 59.000 T to 354.000 T) and the Netherlands (+ 15.000T to 340.000 T) but compensated among others by a decrease in France (- 1.000 T to 56.000 T) and a further decline in the Italian crop due to the severe consequences of the climatic havocs experienced in the main producing regions (- 11.000 T to 202.000 T, while the orchard potential is over 700.000 T). On the varieties, Conference is set to increased by 68.000 T to 873.000 T while Abate should decrease by 12.000 T to

53.000 T. Regarding USA pear production, there is a slight increase from 525.000 T to 529.000 T, driven by Oregon and Washington State, while production in California is severely impacted by the lack of water and labour shortage . The main varieties for the seasons are Williams BC (270.000 T), Anjou (170.000 T), and Bosc (60.000 T). Elsewhere in the Northern Hemisphere, China reported a forecast of pear production of 18,5 Mio T, Turkey of 539.000 T, and India of 89.000 T. In the Southern Hemisphere, the 2021 pears crop ended with a total volume of 1.346.000 T.

Philippe Binard, Secretary-General of WAPA commented: “This year, given the difficult climatic conditions, forecast of production was not easy to be made, in particular regarding the uncertainties on the impact of frost and other spring weather conditions for the quality and the size of products. Looking back, the work undertaken in the different countries was rather precise, as only limited variations were noted. Those were primarily influenced by the good conditions during the summer months in the Northern Hemisphere”. Mr Binard added: “In addition to the apple and pear production forecast, WAPA collects stock figures from the major producing countries throughout the season. As of December, WAPA is resuming the collection of data for the stocks as now the crop is fully harvested and stocks data are now able to be calculated in a reliable manner”.

WAPA can reveal that EU apple stocks stood at 4,865,028 T as of 1 December 2021, which is 6.9 % above the figure of 2020, which reflects the 11 % increase in the crop. On the other hand, pear stocks stood at 654,484 T on 1 December 2021, 26,9 % below the volume of 2020, mostly because of the large decrease in Italy. In Europe, the final pear crop is 26 % lower than a year ago. For the USA, apple stocks in December stand at 1,909,045 T, down 2,58 % compared to 2020. This level is reflecting the lower crop in Washington States this year, which stands at just below 3.000,000 T, 4 % less than last year. Pears stocks in the USA stand at 224,278 T, which is 21,6 % above last year.

In regard to the current season, Domink Wozniak, President of WAPA commented: “Several factors influence the development of this Northern Hemisphere season. The rise in costs for production input, packaging, energy or labour as well as the predicted inflation will have an impact on prodcuer’s margins and competitiveness. Moreover, logistics challenges in terms of availability and costs are some of the new factors influencing trade patterns. Mixed fortune is also expected on market access considering for the European exporters the Belarus embargo as of January 1st combined with the on- going Russian embargo. For the USA, the effects of counter-sanctions in the Steel and Aluminium dossiers are affecting in particular US exports to distant markets such as India . USA trade is expected to primarily focus in North America to the Mexican and Canadian neighbours. In Asia, all exporters are confronted with increased burdens to access China due to increased COVID related controls and logistics hurdles in the port”. On the global stage, one should consider the role of new players such as Serbia, Moldova, Ukraine, Turkey, or Iran. China is also developing its export potential with exports now exceeding one million tons on apples, primarily to South East Asian neighbour. Mr Wozniak added: “Overall in the Northern Hemisphere, the local sourcing will remain a priority in many places considering on-going uncertainties on the world market. However, the growth of apple and pear production in the North Hemisphere, in particular in EU neighbourhood and Central Asia, makes it important to continue diversify the variety assortment for taste expected by consumers. Raising the quality and meeting new sustainability expectations of policy and consumers would facilitate a new boost of the consumption of apples and pears. At the same time, the global apple and pear community should continue searching for new opportunities for the apple and pear consumption in many markets around the world”.

WAPA is slated to host Prongosfruit in Belgrade (Serbia) on 10 and 11 August 2022, in cooperation with Serbia Does Apples. Information will be provided end of March 2022 on the Prognosfruit website (www.prognosfruit.eu).

The price for pear oranges has been on the rise in Brazil since the beginning of the season, in June, influenced by the low supply of oranges in the market. In the second fortnight of October, pear orange prices surpassed BRL 50.00/40.8-kilo box, on tree, setting a new nominal record in the series of Cepea. The monthly average in October (in São Paulo State) closed at BRL 49.88/box, on tree, 10.1 % up from that in September/21 and 28.3 % above that in October/20, in nominal terms.

Agents in the Brazilian citrus sector did not expect supply in the 2021/22 season to be high, based on the effects of the weather on blooming and flower set. However, along the season, weather issues increased, with rainfall below the ideal and frosts in some locations at the end of July.

Although rains were more frequent in October, agents reported that the oranges were mostly small-sized, which kept the prices for larger-sized fruits on the rise – since this standard is required in the in natura segment. From November onwards, quality may increase, and a higher number of late oranges is expected to be available in the market. On the other hand, high purchases from the industry are also expected to control supply in the in natura market.

TAHITI LIME – In the Brazilian market of tahiti lime, the return of rains favored production and raised supply. Besides, the quality of the fruits continued low, and the exports pace was slow in October. Thus, prices for this variety dropped in the orchards in SP, averaging BRL 23.15/27-kilo box, harvested, 21.8 % down from that in September.

ORCHARDS – The rains that hit São Paulo State in October favored blooming in orange orchards, largely in dryland or those that had not bloomed yet. According to citrus farmers, the scenario varied among regions, according to the volume of rain and the production system (irrigated or dryland), but, in general, all agents agree that blooming was satisfactory.

As in previous seasons, this year’s flowering has been irregular and heterogeneous. While in some regions, orchards bloomed earlier (in September), in others, flowering was observed in October. However, the early flowers were compromised by the hot and dry weather in many areas, which led some of the fruitlets to fall, even in irrigated orchards.

Citrus farmers believe this will be another season of multiple blooming, which would hamper both the harvesting and management of trees because of the different development stages of flowers – as it happened in most Brazilian regions in the last years.

Although flowering brought some relief to citrus farmers in all regions, it is important to consider that plants are still debilitated, due to the long drought, which may hamper fruit fixing. Thus, the success of the recent blooming will depend on the weather from now onwards (high moisture interleaved with sunny periods) and preventive care for blossom-end rot. According to Cptec/Inpe (weather forecast agency), rains may be lower than the average in November and in December, which may be a reflex of the La Niña phenomenon, and hamper flower set.

Prognosfruit’s 2021 European apple and pear crop forecast revealed that while apple production is set to increase by 10 %, the upcoming pear crop is expected to decrease by 28 %. On 5 August 2021, more than 150 international representatives from the apple and pear sector joined the Prognosfruit 2021 Online Conference, the second virtual edition of the event in its 46 years, to discuss the 2021 production forecast for apples and pears.

Philippe Binard (Photo: freshfel)

The World Apple and Pear Association (WAPA) released the 2021/2022 European apple and pear crop estimate on the occasion of the 46th edition of the Prognosfruit. WAPA Secretary General Philippe Binard stated: “The apple production in the EU for the 21 top producing countries contributing to this report is estimated for the 2021/2022 season to be 11.735,000 T. Overall, this year’s crop is estimated to be 10 % higher than last year, but 1 % only up from the 3-year average. It is therefore perceived to be a season with a balanced outlook”.

Philippe Binard added ”While the EU apple crop is larger, the EU pear crop for 2021/2022 is estimated to decrease by 28 % compared to last year to 1.604.000 T and by 27 % compared to the three-year average. This is the smallest decade crop for pears” On the varieties, this translates into a decrease of Conference pear by 18% to 805.000 T. Abate is also impacted with a crop reduced to 66.000 T, down by 73 %”.

WAPA will continue to monitor the developments of the Northern Hemisphere crop and will issue updates when available.

The words ‘healthy’ and ‘natural’ are not often linked to sugar substitutes, but Fooditive BV wants to change that. Over the past decade, the Netherlands-based food ingredient manufacturer has been pear-suing sustain-apple solutions to combat global sugar intake. In 2018, this became a reality with its plant-based and chemical-free sweetener. Since then, Fooditive has focussed on improving the health status of products that use sugar replacements by providing an affordable alternative to other options on the market.

As put by Fooditive’s Product Development Manager, Niki Karatza, “developing a sweetener that could successfully replace sugar in food products required us to first understand the true essence of sugar. We managed that by diving into the science behind sucrose, its taste and its unique functionalities.”

This was achieved through an innovative process: the reverse engineering of sucrose. By starting with the end product and working backwards, it allowed Fooditive to analyse the ingredients’ properties and therefore understand how it could mimic the characteristics of sugar in its sweetener. Combining this knowledge with apple and pear waste led to the creation of Fooditive Sweetener®, which is 70 % as sweet as sugar and does not raise insulin or blood glucose levels.

With sustainability and transitioning to a circular economy as Fooditive’s core principles, it obtains the raw materials for its sweetener in two ways. Firstly, it collaborates with Dutch farmers to salvage both organic and non-organic unwanted apples and pears, and secondly, it collects the side streams of these fruits from other production processes. Once gathered, a continuous fermentation process, which means that more sweetener can be yielded in a shorter amount of time, is used to extract fructose and convert it into keto-fructose; this end product is the sweetener.

For 2021, founder and food scientist Moayad Abushokhedim has set a weekly goal to produce around 30 tonnes of Fooditive Sweetener® by upcycling 83 tonnes of third-grade fruit. With this projection, it will become more widely accessible to consumers in a range of products including Gigi Gelato and Hero jam in the Netherlands.

In Germany, Fooditive was nominated for the Healthy Living Award 2020 for its innovation and positive contribution to the organisation’s eathealthy-philosophy. Fooditive Sweetener® will also feature in the Seicha GmbH drinks as of this year.

“Since the founding of Seicha, my brother and I have been searching for a natural sweetener that has a pleasing taste and no calories. With Fooditive, we have finally found a suitable partner, with which we will revolutionise the beverage industry in Europe. Seicha will launch the world’s first organic certified Zero Iced Tea in Q2 2021. The organic iced tea will be launched in three flavours: Green Tea & Ginger; Rooibos Tea & Mango Passion Fruit; and Black Tea & Orange Vanille.” (Co-founder, Benjamin Böning)

With new products in the works and many other companies going bananas for Fooditive Sweetener®, 2021 is set to be an even more promising year, as the company continues to make healthy food and drinks affordable for everyone, all the while fighting food waste.

About Fooditive: Fooditive BV was founded in 2018 with the aim to make healthy food affordable. Its core business model relies on delivering natural and healthy innovation to food companies, with the Fooditive sweetener as its main product. The company’s philosophy is based on three values: plant-based, sustainability, and innovation. Keeping healthy and nutritious products in mind, we aim to provide food that is tasty, low in calories, high in fibre, and has a high supply chain impact. Fooditive implements the three pillars of sustainability into the business model: caring for people by providing healthy alternatives and raising health awareness; operating within a circular economy by reusing, reducing, and recycling; and minimizing environmental impact by using side streams to create products. Finally, to be able to deliver on the demand, we work with many types of partners to get the best out of new types of side-streams affordably and easily.

The World Apple and Pear Association (WAPA) has released the Southern Hemisphere apple and pear crop production forecast for the upcoming season. According to the forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple production is estimated to increase by 6 % in 2021 compared to the previous year, while pear production is projected to stabilise.

The World Apple and Pear Association (WAPA) has released its 2021 apple and pear crop estimate for the Southern Hemisphere. This report has been compiled with the support of ASOEX (Chile), CAFI (Argentina), ABPM (Brazil), Hortgro (South Africa), APAL (Australia) and New Zealand Apples and Pears, and therefore provides consolidated data from the six leading Southern Hemisphere countries. WAPA’s Secretary General Philippe Binard commented on the usefulness of gathering the insights from these major producers: “Elaborating this collective data has previously proved a valuable exercise for the global apple and pear industry and a reliable source of information when the season progressively shifts from the Northern to the Southern Hemisphere”.

Regarding apples, the aggregate Southern Hemisphere 2021 crop forecast suggests an increase of 6 % (5.090.000 T) compared to last year (4.818.000 T), with increases in Australia, Brazil, and South Africa of 23 %, 20 % and 6 % respectively, a decrease in New Zealand of 5 %, and stable figures in Argentina and Chile. The aggregate increased by 2 % compared to the average of crops between 2018 and 2020. Chile remains the largest Southern Hemisphere apple producer in 2021 with 1.512 million T, with Brazil in second place (1.130 million T), followed by South Africa (1.013 million T), Argentina (617 million T), New Zealand (547 million T), and Australia (271 million T). Gala remains the main variety (39 %), followed by Fuji (14 %) and Red Delicious (13 %). Export figures are estimated to stabilise at 1.691.562 T, with stable figures for Chile (650.773 T), a 4 % increase for South Africa (476.000 T), and a 7 % decrease for New Zealand (372.000 T).

Southern Hemisphere 2021 apple production (Photo: WAPA)

Regarding pears, the Southern Hemisphere growers predict a stabilisation of the crop at 1.346.000 T and an increase of 2 % compared to the overall average of years 2018-2020. The increase in South Africa, Australia, and Argentina of 3 %, 2 %, and 1 % respectively are expected to compensate for the 3 % and the 10 % decrease in Chile and New Zealand. As in previous years, Packham’s Triumph and Williams BC/Bartlett are the major varieties, with 36 % and 28 % respectively. Forecasted export figures for pears are reported to increase by 6 % compared to the previous year and reach 708.690 T, with a 12 % increase for Argentina (373.996 T), a 2 % increase for South Africa (214.361 T), and a 3 % decrease for Chile (108.315 T).

Prognosfruit’s 2020 European apple and pear crop forecast revealed that most European countries are expecting an overall stable apple and pear crop for the coming season. On 6 August 2020, more than 150 international representatives from the apple and pear sector joined the Prognosfruit 2020 Online Conference, the first ever virtual version of the event in its 45 years to discuss the 2020 forecast.

During the conference, the World Apple and Pear Association (WAPA) released the 2020 European apple and pear crop estimate. In 2020, the apple production in the EU for the 21 top producing countries contributing to this report is estimated to be just slightly below last year’s result, with a 1 % decrease and a crop of 10.711,000 T. Overall, this year’s crop is estimated to be 4 % lower than the 3- year average. On the other hand, the EU pear crop for 2020 is estimated to increase by 12 % compared to last year to 2.199.000 T. However, a revision of some of the figures presented at Prognosfruit is to be expected in the upcoming weeks. WAPA will continue to monitor the developments of the Northern Hemisphere crop and will issue updates when appropriate.

The virtual conference featured a presentation of the forecast for apples and pears by WAPA Secretary General Philippe Binard, a market analysis by AMI Market Analyst Helwig Schwartau, an overview of the latest trends in processing by Austria Juice CEO Franz Ennser and for organic by Europäisches Bioobst-Forum President Fritz Prem, as well as two panel discussions for apples and pears respectively.

Earlier this year, the Prognosfruit 2020 organisers announced the cancellation of the event, scheduled to take place in Belgrade (Serbia), due to the uncertainties of the COVID-19 pandemic. However, due to popular demand the event was rescheduled as a a virtual conference. Belgrade will now host Prognosfruit in 2021 instead.

(Photo: WAPA)

Over the years, Prognosfruit has become the leading annual meeting point for the European apple and pear sector. Each year the conference gathers around 300 leaders from the apple and pear sector in a different European country in early August. Prognosfruit is an opportunity not to be missed to debate the latest sector developments and be informed on the annual apple and pear crop forecast.

For the first time since the initiation of Prognosfruit in 1976, the organizers of the 2020 edition have had to take the difficult decision to regretfully cancel this year’s conference. Prognosfruit was scheduled to take place later this year in Belgrade (Serbia) from 5-7 August 2020.

The global COVID-19 pandemic has prevented Prognosfruit from being organized this year under normal conditions. So far, there is no indication when the current travel restrictions within the European Union and on the external borders of the European Union will be lifted. Furthermore, at the time of the conference some quarantine rules might still be in place as well as other restrictions on transport and social distancing.

It has been agreed with Serbia Does Apples, the local organizer of conference planned conference in 2020 in Belgrade, that Prognosfruit 2021 will take place in Serbia.

In the meantime and regarding the 2020 forecast, WAPA will release the apple and pear forecast as usual. The modalities of disclosing the 2020 forecast will be announced in July.

The World Apple and Pear Association (WAPA) held its Annual General Meeting on the last day of the Fruit Logistica fair in Berlin (Germany), 7 February 2020. Representatives of the key global apple and pear producing and exporting countries met to discuss the Southern Hemisphere production forecast, the final update of the Northern Hemisphere production forecast that was released in August 2019, and the season developments.

WAPA discussed and released the consolidated crop forecasts for the forthcoming southern hemisphere apple and pear seasons (see SH Statistics aggregate in email). Collected from industry associations in Argentina, Australia, Brazil, Chile, New Zealand and South Africa, the forecast showed that the 2020 apple and pear Southern Hemisphere crops are expected to reach 5.003.000 T and 1.276.000 T, respectively. For apples, this represents a small decrease of 1 % compared to the 2019 crop. Export is expected to remain stable at 1.725 million T. The pear crop is expected to decrease by 3 % compared to 2019. Export is expected to decrease by 2 % to 691.660 T. The Northern Hemisphere crop and stocks data were also updated. Overall, the forecasts continue to demonstrate the huge variation in crop sizes due to the consequences of climatic havocs impacting the production. Furthermore, the Eurasian apple growing developments and global reporting initiatives were discussed.

Other topics on the agenda were marketing, promotion and consumption trends, and research and innovation activities among the members. The discussion underlines the efforts of the sector to cope with the new market requirements and expectations to reduce pesticide dependency. It also focussed on the development of new sustainable strategies regarding water usage, biodiversity, carbon emissions, adapting packaging to the plastic debate and continuing to promote the health benefits of apples and pears to consumers around the world.

The 2019 European apple and pear crop forecast estimates that most European countries are expecting a rather low apple and pear crop for the coming season. On 8 August 2019, close to 300 representatives of the international apple and pear sector met at the Prognosfruit Conference in Alden Biesen, Belgium. During the conference, the 2019 European apple and pear crop estimate was released. This year, the apple production in the EU is set at 10.5 million T as a result of climatic events and the alternation of last year’s bumper crop. This is a decrease of 20 % compared to last year’s record high crop and of 8 % compared to the average crop of the three previous years. The pear crop is predicted at 2 million T, a decrease of 14 % compared to 2018. Nevertheless, comparisons with previous years need to be handled with much caution, given last two years’ exceptional variation.