The World Citrus Organisation (WCO) is finalising preparations towards the second edition of the Global Citrus Congress, which will take place on 16 and 17 November 2021. The virtual event, which managed to gather over 1000 delegates from across the globe in its first edition in 2020, will once again bring together the citrus community to discuss the current trends, challenges, and opportunities for the citrus sector. More than 500 participants from across the globe have already registered to attend the virtual congress.

Following the success of the first Global Citrus Congress in 2020, this year the event will take place online on 16 and 17 November 2021. The opening session of the first day (Tuesday 16 November from 3:00 to 6:00 p.m. CET) will provide an in-depth discussion on production and marketing trends for fresh and processed citrus, including a panel discussion with key producing countries over the ongoing Northern Hemisphere 2021 citrus season. During the second day of the congress (Wednesday 17 November), 3 regional modules will zoom into specific issues of the citrus business in Asia (8:00 to 10.00 a.m. CET), Europe (3:00 to 5:00 p.m. CET), and North America (5:00 to 7:00 p.m. CET). Asia’s module will focus on key market developments and branding trends, with speakers including Wayne Prowse (Fresh Intelligence), Neil Barker (BGP International), and Hannes de Waal (Sundays River Citrus Company) among others. The European track of the Congress will in turn discuss post-harvest trends in citrus with key sector representatives from Agrofresh, Apeel, Citrosol, Decco, Jansen, and the Dutch Fresh Produce Centre. During Europe’s session, WCO’s General Delegate Philippe Binard will also discuss citrus consumption trends and promotion strategies with key market leaders from across the chain. Finally, the North America’s section will delve into the US citrus market trends with a focus on easy peelers, lemons, and limes. The strategies and challenges for key producing regions California and Florida will also feature in the programme.

WCO Co-Chair and Director of AILIMPO Jose Antonio Garcia affirmed: “We have been working intensely to improve on the first edition of the Global Citrus Congress by elaborating an attractive agenda with a stronger presence of business-led interactive debates. We want to consolidate the Congress as a must-attend event for the citrus sector, and we hope we held it physically in 2022”. WCO Co-Chair and CEO of the Citrus Growers’ Association of Southern Africa Justin Chadwick added: “After the success of the first edition in 2021, the Global Citrus Congress is on the right track to become the key annual event for the community to strengthen the position of citrus fruit in an ever-competitive, challenging environment”.

The Global Citrus Congress will take place online. The sessions will be live and free of charge to attend thanks to the support of our sponsors. Registrations are still open at https://www.citruscongress.com/. The opening session will be available both in English and Spanish.

The global pandemic has affected the packaging solution industry by leading to a significant price increase and shortage of raw materials and components used in packaging equipment. To compensate for the rising costs and continue to provide the highest quality solutions, Sidel is implementing a commodity-induced price adjustment on its equipment by an average of 5 % effective September 6, 2021. Deficiency of raw materials and components may impact equipment delivery time as well.

Since the outbreak of COVID-19, Sidel has been striving to keep the same price level for its equipment despite the fact that the price of raw materials has increased significantly since 2020. Moreover, this increase is not expected to recover in the foreseeable future.

Additionally, the pandemic, combined with other external factors, has resulted in a significant shortage of microchips globally. This shortage is an outcome of supply-related disruptions, including forced closure of factories, together with an unanticipated increase in demand for personal electronics such as cell phones and laptops as people were required to work or study remotely. Both supply shortage of microchips and increase in consumption of personal electronics lead to supplier delays which might impact the overall Sidel delivery channels for the near future.

The global pectin market is estimated to reach USD 1.87 billion by 2026 and is anticipated to grow at a CAGR of 6.4 % from 2018 to 2026. Pectin market is projected to witness significant growth over the forecast period. Increasing health consciousness among consumers and various health benefits of pectin products is expected to drive the global market over the forecast period.

Pectin are plant-derived compounds, a structural heteropoly saccharide that is contained in primary cell walls of the terrestrial plants. It is mainly extracted from citrus fruits, apples, apricots, cherries, oranges, and carrots. Commercially, it is available in the form of white to light brown powder. The industry is characterized by companies characterized by medium level of integration in the value chain. Packaging and shipping play an important role in integrating the value chain. This helps the companies to incorporate their businesses in a cost-effective way.

Suppliers include companies which are involved in the production & distribution of processes raw materials such as apple, citrus, and others. The rising shortage of raw materials and increased import for Brazil and European countries is resulting in high bargaining power to the suppliers. In addition, low threat of backward integration from manufacturers, except some of the major and giant market players is also resulting in high bargaining power of suppliers.

The pectin market witnesses an external threat of substitution from natural gum and Citri-fi. Citri-fi is natural functional fibers, which are derived from citrus fruits. They offer hydrocolloidal properties, which is significant for high water holding capabilities. There are also some synthetic alternatives such as polyurethane, but these are usually not considered suitable for skin contact applications. However, the various advantages of pectin over these products are expected to lower the threat.

Pectin extracted from this raw material are used for high cholesterol high blood pressure, & blood sugar, joint pain, weight loss, prevent colon & prostate cancer, high triglycerides, gastroesophageal reflux disease (GERD) and diabetes. In addition, some people also use pectin to prevent poisoning caused by strontium, and other heavy metals.

Despite the shortage in the supply of raw material, some of the major players are also trying to increase their production capacity to meet the demand. For instance, Cargill acquired FMC’s plant to boost their pectin production capacity. The market is highly fragmented and competitive. In addition, it also experiences the presence of small-scale as well as giant players. The key and major companies are investing in R&D activities and frequently involved in merger and acquisition to increase their market share and product portfolio. Some of the companies that have a significant influence in the industry include DuPont Nutrition & Health, FMC Corporation, CPKelco, Herbstreith & Fox, Devson Impex Private Limited, Cargill Incorporated, B&V srl. and Yantai Andre Pectin Co. Ltd.

Growth in food & beverage industries, in emerging economies, is expected to drive the Asia Pacific market. The market is projected to grow rapidly in the Asia Pacific region, owing to the changing lifestyle of consumers in emerging economies including, China and India. The rising health consciousness among consumers and the presence of major players in North America is projected to positively drive the growth of the market over the forecast period.

Firmenich, one of the world’s largest privately-owned fragrance and taste companies, became the first company in the world to successfully upgrade its global EDGE Certification for gender equality in the workplace to the next level: “Move” status. Recognizing the Group’s ever more inclusive culture, the leading business certification standard for gender equality awarded Firmenich Move status for its progress in expanding diverse representation at all levels and a strong sense of belonging among its diverse workforce. Firmenich continues to lead in workplace equality, having been the 7th company in the world and the first in its industry to achieve global certification in 2018 at Assess level.

“I am very proud that Firmenich is one of only two companies that have achieved Global EDGE MOVE certification, raising the bar for gender equality under EDGE’s demanding benchmarks for continuous improvement,” said Gilbert Ghostine, CEO Firmenich. “EDGE recognizes our concrete achievements in embedding equality worldwide, as an employer of choice and a trusted and reliable partner for our customers. I am particularly pleased that we set the standard at the very top of the organization with gender parity on our world-class executive team.”

“The remarkable leap forward Firmenich has made in two years at the global level from the first level to the second level of EDGE Certification, EDGE Move, demonstrates that intentional, prioritized and measured actions undeniably accelerate progress towards gender balance, diversity and inclusion,” said Aniela Unguresan, Co-founder of EDGE Certified Foundation. “Specifically, Firmenich’s global EDGE Move certification illustrates the company’s progress in terms of gender representation and proactive management of pay equity across its main countries of operation.”

“Firmenich continues to set the standard for excellence as the best place to work in our industry. Since our first global EDGE certification in 2018, we have achieved significant milestones, from no gender pay gap worldwide to systematically implementing diverse talent pools,” said Mieke Van de Capelle, Chief Human Resources Officer at Firmenich. “While I am very proud of our achievements, we are focusing on new frontiers with targeted action that goes beyond gender. It’s about embracing the power of inclusion of minority groups, securing effective representation and engagement of people with different abilities, ethnic and socio-economic backgrounds and sexual orientation.”

Building on its achievements, the Group’s new Environmental, Social and Governance (ESG) strategy sets ambitious 2030 people goals, including commitments on human rights, ethnic pay equity, creating 5,000 job opportunities for youth and continuing to raise the representation of differently-abled people in its workforce to 10 %.

Since 2018, Firmenich has raised women’s representation in its global workforce to 41 % and eliminated gender pay gaps. Expanded flexible working opportunities worldwide, effective recruitment and promotion practices, as well as continuous training and mentoring, have enhanced equal representation at all levels including critical pathways to senior management. Half of Firmenich’s Executive Committee is female.

EDGE Certification at the global level entails a global evaluation of Firmenich data and processes, as well as a comprehensive survey of its employees worldwide. Firmenich emerged from the rigorous assessment as an employer that is clearly meeting and exceeding core certification criteria around hiring, pay, retention, development and engagement of its employees.

About EDGE Certification EDGE is the leading global assessment methodology and business certification standard for gender equality. It measures where organizations stand in terms of gender balance across their pipeline, pay equity, effectiveness of policies and practices to ensure equitable career flows as well as inclusiveness of their culture. Launched at the World Economic Forum in 2011, EDGE has been designed to help companies not only create an optimal workplace for women and men, but also benefit from it. EDGE stands for Economic Dividends for Gender Equality and is distinguished by its rigor and focus on business impact. EDGE assessment methodology was developed by the EDGE Certified Foundation, which continues to act as the guardian of EDGE methodology and certification standards. Its commercial arm, EDGE Strategy, works with companies to prepare them for the EDGE Certification. EDGE Certification’s diverse customer base consists of 200 large organizations in 44 countries across five continents, representing 29 different industries and employing globally more than 2.4 million employees.

Nestlé S.A. announced that it has reached an agreement to sell its regional spring water brands, purified water business and beverage delivery service in the U.S. and Canada to One Rock Capital Partners in partnership with Metropoulos & Co. for USD 4.3 billion. The Company’s international premium brands including Perrier®, S.Pellegrino® and Acqua Panna® are not a part of the deal. The transaction is expected to close following the completion of customary closing conditions.

The sale includes the following brands in the U.S. and Canada, which had sales of around CHF 3.4 billion in 2019: Poland Spring® Brand 100 % Natural Spring Water, Deer Park® Brand 100 % Natural Spring Water, Ozarka® Brand 100 % Natural Spring Water, Ice Mountain® Brand 100 % Natural Spring Water, Zephyrhills® Brand 100 % Natural Spring Water, Arrowhead® Brand Mountain Spring Water, Pure Life® and Splash. It also comprises the U.S. direct-to-consumer and office beverage delivery service ReadyRefresh®.

The agreement follows Nestlé’s announcement last year that it would conduct a strategic review of parts of the North American waters division and sharpen the focus of its global water portfolio.

Commenting on the transaction, Mark Schneider, Nestlé CEO, said: “We continue to transform our global waters business to best position it for long-term profitable growth. This sale enables us to create a more focused business around our international premium brands, local natural mineral waters and high-quality healthy hydration products. We will also boost our innovation and business development efforts to capture emerging consumer trends, such as functional water.”

Nestlé reiterated its commitment to make its entire water portfolio carbon neutral by 2025. In 2020, Nestlé announced renewed sustainability commitments which build on existing efforts to enhance water stewardship and tackle plastic waste.

Oranges

Global orange production for 2020/21 is forecast to rise 3.6 million metric tons (tons) from the previous year to 49.4 million as favorable weather leads to larger crops in Brazil and Mexico, offsetting declines in Turkey and the United States. Consequently, consumption, fruit for processing, and fresh exports are also forecast higher. …

The now, next, and future of the global food and drink industry

The events of 2020 caused a fundamental reset in human behaviour. Recognising this transformation, Mintel’s 2021 Global Food and Drink Trends are inspired by recent shifts in consumer purchases and attitudes across industries. Through collaboration with consumer analysts and insights from Mintel Trends, a global team of food and drink experts have identified new opportunities in line with three of the Mintel Trend Drivers: Wellbeing, Value, and Identity.

In 2021 and beyond, expect food and drink companies to create mental and emotional wellbeing solutions, deliver on new value needs, and use brands to celebrate people’s identities.

Feed The Mind

Innovative food and drink formulations will offer solutions for mental and emotional wellbeing that will create a new foundation for healthy eating.

Quality Redefined

Brands will be challenged to respond to new definitions of trust, quality, and ‘essential’.

United By Food

Food and drink brands can balance a person’s need to feel unique and special with the desire to be part of communities of like-minded individuals.

Please download the free 2021 Global Food and Drink Trends here.

Mintel, the experts in what consumers want and why, has announced seven trends set to impact global consumer markets in 2021, including analysis, insights, and recommendations centered around consumer behavior, market shifts, innovative brands, and opportunities for companies and brands to act on in the next 12 months:

Health Undefined: An awareness of wellbeing is at the forefront of consumers’ minds, but a playbook doesn’t exist. Brands have a responsibility and opportunity to set new rules.

Collective Empowerment: Consumers around the world are making their voices heard loud and clear in the push for equity, agency, and rights.

Priority Shift: Consumers are seeking a return to the essentials, with a focus on flexible possessions and a reframing of what ownership actually means.

Coming Together: Consumers are coming together in like-minded communities in order to connect with and support each other, driven by the impact of the global pandemic.

Virtual Lives: Physical separation due to the pandemic, increased need for escapism, and improved technology are driving consumers towards digital experiences.

Sustainable Spaces: COVID-19 has subtly but significantly shifted consumer awareness of our relationship with the spaces in which we live, accelerating demand for sustainability.

Digital Dilemmas: While there are many benefits to a more digitally-connected life, concerns about its negative impacts are putting consumers in a predicament.

Please download the FREE 2021 Global Consumer Trends under www.mintel.com.

In terms of sustainability, Symrise ranks among the top ten companies in the world according to the current ranking of renowned non-profit organization CDP (previously known as the Carbon Disclosure Project). CDP makes a yearly assessment of what participating companies do to fight climate change, protect water supplies and conserve forests. For forest conservation, the Holzminden Group is actually doing better than in the previous year and has achieved a spot on the A list in all three categories – the best possible result. This year, more than 9,600 companies took part voluntarily in the assessment.

Only ten companies out of the 9,600 that took part achieved the highest grade in all three categories. Symrise was one of them, making an improvement on last year’s rating. Last year, the Group made it onto the A list for climate and water, but got an A minus for forests. Many factors play a role in the CDP’s decision. The non-profit organization pays attention to whether the company in question is an environmental pioneer and how it deals with environmental risks. It also considers ambitious goals and the completeness of the data disclosed to be important. Based on the results, the CDP divides the participants into categories from A, the highest, to D.

Symrise aims at climate-positive operations by 2030

Symrise has been following ambitious sustainability objectives for years. Conservation of forests has played an important role in this. The company wants to counteract deforestation throughout the entire value chain as well as work for the conservation and reforestation of forests. This is why the Group uses resources from sustainable forestry. To guarantee this, Symrise ensures that its strategic raw materials are fully traceable.

Climate protection is also very important to Symrise. The Group wants climate-positive operations by 2030 and to actively help limit global warming to below 1.5 °C. During the last ten years, the company has already reduced its greenhouse gas emissions in terms of value added by more than half. Symrise is also very conscious of saving water and makes its contribution to keeping the resource available. By 2025, all production sites in regions affected by drought will improve their water efficiency by 15 percent compared to 2018.

Purpose built and designed with significantly more capacity, efficiency and data harvesting to drive growth

Treatt, an ingredients manufacturer and solutions provider to the global flavour, fragrance and consumer goods markets, has partnered with Siemens Digital Industries (DI) to build a world class digital manufacturing facility at its £41m new global headquarters.

Treatt’s purpose-built site in Bury St Edmunds replaces the existing complex in the town which has served as the company’s headquarters since 1971.

The new facility will bring together, under one roof, over 200 people in its science led distillation, manufacturing, logistics, technical and office-based functions in a once in a generation relocation upgrade to provide the scalable platform for further growth.

The factory will be controlled by Siemens SIMATIC PCS 7 system which will offer Treatt more data, flexibility, scalability, availability, safety, and security in its production process.

Crucially it will automate its entire production process, enabling Treatt to increase efficiency and productivity, consistency, reliability, throughput, and repeatability.

The new factory is built and designed to have significantly more operational capacity in an optimally designed production space.

Mark Higham, General Manager, Process Automation, Siemens DI, said, “It is important for us to work very closely with Treatt to ensure we deliver the best solutions for their new headquarters.”

Siemens SIMATIC PCS 7 distributed control system is a flexible and scalable platform which addresses the wide-ranging needs of the process industries. It has an open system architecture covering the entire production process ensuring the efficient interaction of all automation components in the factory.

Higham added, “Considering that Treatt is bringing all its functions of distillation, manufacturing and logistics operations under one roof then SIMATIC PCS 7 was a perfect fit.”

Some of the features of SIMATIC PCS 7 are its consistent approach to data management, the application of global standards, powerful and compact hardware and proven software libraries. These common features minimise the engineering overheads, reduce costs, shorten time to market and increase the flexibility of the plant.

Daemmon Reeve, Group CEO of Treatt said “As a science led innovator of ingredients designed to enable our customers to differentiate in the marketplace, we are excited to work with Siemens to drive a wide range of benefits into our world class manufacturing business.”

“Treatt sources a wide range of natural raw materials from supply partners around the world. As expected, nature provides variation in flavour profile from season to season and our job is to ensure consistency in the wide-ranging extracts we create for customers through complex distillation and extraction processes, so their beverages have the critical consistency in flavour profile.”

Treatt has a bespoke and dedicated analysis system which is now aligned and fully integrated with the Siemens SIMATIC PCS 7 system to capture the results and data for future use as the company drives into further areas of digitalisation for the business.

In addition, Siemens has won a three-year service contract to support the new production facility.

Bruce Sinclair, Engineering & Site Services Manager, Treatt commented “The three-year service support contract is necessary as our operations team will be reliant on the new control systems for increased and efficient productivity. It is essential for us that maintenance of the new systems remain at a high standard set by the suppliers of the technology for longevity and competence.”

Siemens has already begun providing support with upskilling Treatt’s employees to use the new systems and their instrumentation engineer has completed a two-week training course at a Siemens site.

“Moving to the new site will be beneficial for our operation and our customers will see very clearly how our science led, customer partnership model is transforming Treatt into a crucial partner for those customers wanting true authenticity in natural extracts to enable them to win, that is what motivates us” says Reeve.

Higham, added, “I am delighted that our projects team are partnering with Treatt to deliver this advanced control system which will provide the backbone for their production processes and support their digitalisation journey.

“With digitalisation, we help manufacturers become more agile, and provide tools for reducing operations costs whilst increasing efficiency and reducing time to market. In addition, our fully integrated safety and security concepts ascertain a safe production environment for employees and the facilities where they are deployed.”

Siemens has teamed up with a fully certified Process Instrumentation Approved Partner for the deployment of the full range of its instrumentation portfolio across all lines of production at the plant.

Jon Tayler, Director at Process Instrument Sales Ltd, commented: “Our strategy for Treatt was to provide a technically correct and commercially effective solution for the instrumentation requirements of the demanding process systems, whilst ensuring efficiencies, safe working practices and environmental criteria.

“Our long-standing relationship with Treatt, as their approved partner, meant that we are able to be an essential element of the Total Integrated Solution that Siemens promotes for seamless process control and monitoring, which is what the engineering team at Treatt have set out to achieve.”

As well as its UK operation Treatt has a manufacturing site in the USA and a sales office in China, with a network of agents throughout the world.

As Head of Global IT, the IT specialist Robert Kubotsch is taking on overall responsibility for information technology at Kautex Maschinenbau. With this appointment, the global leader in extrusion blow molding machines has filled another key position to steer and support its process of change. Robert Kubotsch will harmonize the existing IT systems and optimize them for cooperation between the global Kautex team, customers and partners. Isolated solutions which have been used to date will be replaced with a uniform IT structure at all locations, and the availability of IT services and infrastructure at crucial points will be improved.

Robert Kubotsch previously worked for an international plant and machinery manufacturer. In this role he was responsible for the maintenance and further development of IT at various locations. His experience of various projects across different sectors has given him a keen understanding of the business processes involved in running a machinery manufacturing enterprise, and its ever-expanding IT requirements.

Kautex Maschinenbau has been involved in a process of strategic realignment and restructuring for over two years. The company is bringing about harmonized processes and standards in line with the BeOne motto, as well as placing even greater emphasis on customer focus in all business areas. The production solutions are becoming more intelligent, modular, and flexible, and the aim is primarily to generate added value for customers.

These changes are accompanied by increasing digitalization in communication, production, and service. Data management, communication systems and comprehensive remote services place high demands in terms of the efficiency, standardization and global availability of IT. Kautex announced enhanced investment in this area some time ago. Robert Kubotsch and his team will now put the philosophy into action.

The World Citrus Organisation (WCO) Secretariat, together with its partner Fruitnet Media International, is finalising preparations for the first edition of the Global Citrus Congress, which will take place on 5 November 2020. The Global Citrus Congress will bring together the citrus community to discuss the current trends, challenges and opportunities for the citrus sector. More than 300 participants from across the globe have already registered to attend the virtual congress.

The programme of the first edition of the Global Citrus Congress 2020 will highlight the key areas of interest for the sector. This will include production and marketing trends, facilitating cooperation between suppliers and retailers to add value to the citrus category, new technologies and supply chain innovation helping citrus producers and marketers to respond to consumer demands towards increased sustainability, and harnessing the nutritional power of citrus to develop more effective marketing campaigns. Confirmed speakers include top representatives from the global citrus community, including Ms Naomi Pendleton from AM FRESH Group, Mr Jose Luis Molina from Hispatec, Mr John Chamberlain from Limoneira and Stephan Wesit from Rewe.

WCO Co-Chair and Director of AILIMPO Jose Antonio Garcia affirmed, “There is no doubt that this first edition of the Global Citrus Congress will provide an excellent opportunity to discuss the challenges of the future and consolidate the role of the World Citrus Organisation as a meeting point for the great citrus fruit family. Cooperation, communication and constructive debate are the key to tomorrow’s success as these are the objectives of the Global Citrus Congress”. WCO Co-Chair and CEO of the Citrus Growers’ Association of Southern Africa Justin Chadwick added “As the World Citrus Organisation goes from strength to strength in terms of membership, this Congress will share important global citrus information and the views of leading actors in the sector. It is an event not to be missed”.

The Global Citrus Congress will be available live in both English and Spanish, and is free to join online and open to anyone with a smartphone or laptop and a high-speed internet connection. Registrations are still open at www.citruscongress.com.

Company to establish new operating units and global beverage category leads, supported by new platform services organization

Workforce to be aligned to focus on growth; reductions expected through voluntary and involuntary separation program

The Coca-Cola Company announced strategic steps to reorganize and better enable the Coca-Cola system to pursue its Beverages for Life strategy, with a portfolio of drinks that are positioned to capture growth in a fast-changing marketplace.

The company is building a networked global organization, combining the power of scale with the deep knowledge required to win locally. The company will create new operating units focused on regional and local execution that will work closely with five marketing category leadership teams that span the globe to rapidly scale ideas.

This structure will be supported by the company’s newly created Platform Services organization, which will provide global services and enhanced expertise across a range of critical capabilities.

“We have been on a multi-year journey to transform our organization,” said Chairman and CEO James Quincey. “The changes in our operating model will shift our marketing to drive more growth and put execution closer to customers and consumers while prioritizing a portfolio of strong brands and a disciplined innovation framework. As we implement these changes, we’re continuing to evolve our organization, which will include significant changes in the structure of our workforce.”

Operating units

The company’s nine new operating units will help streamline the organization by replacing current business units and groups. The operating units will be highly interconnected, with more consistency in structure and a focus on eliminating duplication of resources and scaling new products more quickly.

The company’s current model includes 17 business units that sit under four geographical segments, plus Global Ventures and Bottling Investments. Moving forward, the operational side of the business will consist of nine operating units that will sit under four geographical segments, along with Global Ventures and Bottling Investments.

The company’s operating leaders will report to President and Chief Operating Officer Brian Smith.

Global category leads

Innovation, marketing efficiency and effectiveness are top priorities for the company. The Coca-Cola Company is conducting a portfolio rationalization process that will lead to a tailored collection of global, regional and local brands with the potential for greater growth. To drive these initiatives and support the operating units, the company is reinforcing and deepening its leadership in five global categories with the strongest consumer opportunities:

Coca-Cola

Sparkling Flavors

Hydration, Sports, Coffee and Tea

Nutrition, Juice, Milk and Plant

Emerging Categories

The leaders of these categories will work across the networked organization to build the company’s brand portfolio and win in the marketplace. Global category leads will report to Chief Marketing Officer Manolo Arroyo.

Platform Services

The company announced the creation of Platform Services, an organization that will work in service of operating units, categories and functions to create efficiencies and deliver capabilities at scale across the globe. This will include data management, consumer analytics, digital commerce and social/digital hubs.

Platform Services is designed to improve and scale functional expertise and provide consistent service, including for governance and transactional work. This will eliminate duplication of efforts across the company and is built to work in partnership with bottlers.

Platform Services will be led by Senior Vice President and Chief Information and Integrated Services Officer Barry Simpson.

Aligning the company’s workforce to new priorities

The company’s structural changes will result in the reallocation of some people and resources, which will include voluntary and involuntary reductions in employees. The company is working on this next stage of design and will share more information in the future.

In order to minimize the impact from these structural changes, the company today announced a voluntary separation program that will give employees the option of taking a separation package, if eligible.

The program will provide enhanced benefits and will first be offered to approximately 4,000 employees in the United States, Canada and Puerto Rico who have a most-recent hire date on or before Sept. 1, 2017. A similar program will be offered in many countries internationally. The voluntary program is expected to reduce the number of involuntary separations.

The company’s overall global severance programs are expected to incur expenses ranging from approximately $350 million to $550 million.

With an aging population globally, consumers are increasingly looking for solutions that help them to live their lives to the fullest while maintaining high levels of health and wellness regardless of their age.

While 7 out of 10 global consumers in an Innova Consumer Survey said that they had made changes over the past year to improve their health, these changes were not just for physical health, with consumers balancing physical, mental, and emotional aspects. Changes to improve physical wellbeing continued to lead, with 53 % of respondents saying that they had made a change. However, numbers were also significant for consumers saying that they had taken steps to improve mental health and emotional wellbeing (44 % of respondents) and for consumers saying that they had sought more spiritual time (32 % of respondents).

As a result, nutrition that supports both physical and emotional wellbeing is thriving and can target the needs and preferences of different generations with more specific holistic approaches to help identify opportunities and optimize innovation.

Being aged 60+ continues to be redefined, as this age group strives to remain healthier and more active while potentially working until later in their lives than previous generations out of choice or necessity. Future seniors, however, will come from Generation X and Millennials, raised in a different era to the Silent Generation and Boomers who make up the over 60s of today.

Innova’s 2019 research study indicates that 76 % of consumers aged between 26 and 55 years agreed that healthy aging started with what they ate and drank, while 56 % said that they had increased their consumption of functional foods/drinks over the previous year.

Healthy aging claims are starting to appear more regularly on food products and beverages as younger generations prefer functional food & beverages to classic supplement formats. Global research by Innova Market Insights indicates that while 29.7 % of over 55s cited tablets and 26 % cited capsules as their preferred form of intake for supplements in 2019, among those aged 26 to 35 years, nearly 30 % preferred supplements in the form of food products and 27.7 % as beverages, falling slightly to 22.1 % and 25 %, respectively, for those aged 36 to 45.

This presents opportunities to redefine supplements and how they are used, while we are also seeing blurring boundaries between supplements and food/drinks.

It is clear that products with active health claims are increasingly featuring in the marketplace to cater to a variety of needs. Food and beverage launches with active health claims tracked by Innova Market Insights are seeing a growth of +11 % (Global, 2018 vs. 2019). There is a particular focus on healthy aging or aging well, both for seniors and for younger demographics who already engaging with preventative care.

Joint health, energy/alertness, immune health, and bone health are some of the fastest-growing active health claims for global food and beverage launches in recent years as links between particular nutrients and health benefits are increasingly made.

Brain health is another area of growing interest, particularly in terms of aging well, while targeting physical appearance via nutrition and diet is also seeing rapidly rising levels of interest.

On 7th September 2020 at 13:30 BST, Myrthe de Beukelaar, Market Analyst at Innova Market Insights, will present Health & Happiness: a Holistic Approach to Healthy Aging webinar as part of Vitafoods Virtual Expo event. Join Myrthe to learn more about how consumers are increasingly looking for solutions to live their life to the fullest. Register here.

Orange Juice

Global orange juice production for 2019/20 is estimated to slip 23 percent to 1.6 million tons (65 degrees brix) as production in Brazil and Mexico tumbles as a result of fewer oranges expected to be available for processing. Consumption is projected to be flat (though not down) and global trade is estimated lower with the expected drop in exports from Brazil and Mexico. …

The global packaging producer, Ecolean has been awarded the prestigious Gold Medal Recognition 2020 for its sustainability work. The certificate is awarded by the independent and trusted provider of sustainability ratings, EcoVadis. In the overall rankings, Ecolean is placed in the top 5 percent of a total of 60,000 companies assessed from 155 countries.

Ecolean’s high score is based on the company’s strategic work with clear objectives within significant areas of sustainability such as environment, including renewable energy and climate impact and social aspects – as well as via monitoring and transparent reporting of sustainability data of its lightweight packages and filling machines. For Ecolean, this is the first year the company participates in the ratings by EcoVadis.

EcoVadis is an independent provider of business sustainability ratings, which evaluates companies’ sustainability work in global supply chains annually. The assessment focuses on four key areas: environment, labor and human rights, ethics and sustainable procurement. EcoVadis uses international standards such as the Global Reporting Initiative and the UN Global Compact.

About Ecolean

Ecolean develops and manufactures innovative packaging systems for the dairy and liquid food industry. Ecolean’s modern lightweight packaging is consumer convenience and environmental concern in one. Ecolean is a global company with its headquarters in Sweden. Established in 1996, the company has commercial activities in over 30 countries, with China, Pakistan and Russia being its largest markets. Ecolean has 450 employees.

Pectin market value is expected to surpass USD $1.8 billion by 2026, owing to a growing necessity for organic and herbal cosmetic products among the young population.

Global pectin market research studies the types of application (food & beverages: jams, dairy, non-dairy beverages, confectionery), their type (high methylated ester pectin, low methylated ester pectin, and amidated pectin), their function (gelling agents, thickener, stabilizer, fat replacer and others), regional outlook, price trends, growth potential, competitive market share and provides forecasts for 2019–2025. Global Market Insights, Inc., forecasts more than a 7.6 % CAGR for the worldwide pectin industry up to 2025.

Driven by the growing need for plant-based ingredients, the global pectin market is projected to observe significant gains over the forthcoming years. Plant-based ingredients are witnessing this upsurge since they offer immense health benefits.

Pectin products help to control blood sugar levels. These products also help to maintain proper bowel health. Owing to these multiple benefits, pectin products are best suited for nutritional needs, which is likely to foster their market share in the coming years.

Along with health concerns, rising applications of the product in confectionery fillings and sweets would possibly augment the market outlook. Additionally, the increasing usage of pectin in fruit juices and milk drinks as a stabilizer would add up to the industry’s expansion. Pectin helps decrease syneresis in marmalades and jams.

With respect to the raw material segment, apples have dominated the market outlook in recent years. The product is anticipated to witness similar growth in the forthcoming timeframe. This development is attributed to the use of apple pomace in production. Apple peel is one of the major wastes in preserve manufacturing. This peel contains about 1.3 percent of pectin. Apple peel yields more pectin in comparison to sugar beet and citrus peels. In addition, it has better gelling characteristics which further makes it a major raw material in the beverage and food market.

With reference to the geographical landscape, the Asia-Pacific pectin market is predicted to observe significant growth throughout the forthcoming years. Rapidly transforming customer lifestyles is the key factor augmenting the market outlook in the region.

In addition, the increasing demand for consumables that are organic in nature is likely to add up to the growth of the overall market trends. China would possibly lead the market expansion in the region. The country is among the largest producers of pectin. It is also observing mounting demand for health and wellness products due to the increasingly growing middle-class population. Furthermore, rising applications of citrus-based products in the cosmetics sector would further outline the market growth in the region.

Some of the key players in the pectin market includes Cargill, Dupont, Krishna Pectins Pvt Ltd, AEP Colloids, Silvateam S.p.a, CP Kelco U.S., Inc., TIC Gums, Inc. (Ingredion), Compania Espanola de Algas Marinas, S.A., Merck KGaA, Lucid Colloids Ltd., Herbstreith & Fox, Nikunj Chemicals, Pure Ingredients, Cifal Herbal Private Ltd, California Ingredients Inc, Calleva Ingredients Limited etc.

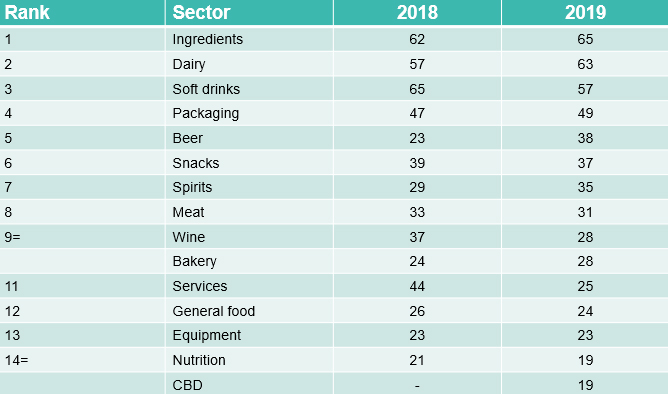

2019 broke records again for the number of food and drink transactions around the world, with 789 registered on the Zenith Global mergers and acquisitions database, an average of 15 each week.

The total is 12 more than in 2018 and 41 % higher than 5 years ago. The number has increased every year since a dip in 2013.

The most active sectors were ingredients on 65, dairy on 63, soft drinks on 57 and packaging on 49. Beer on 38 was ahead of spirits on 35 and wine on 28.

Global food and drink acquisitions by sector 2018-2019 (Photo: Zenith Global)

The top 15 sectors were the same as 2018, with the exception of CBD replacing confectionery. The combination of plant-based (15) with dairy-free (14) and meat-free (11) totalled 40. Bottled water and water coolers added up to 23. Vertical farming was a newcomer with 8.

The biggest increases were for CBD (+19) and beer (+15). Many of the main categories saw declines, led by services (-19), confectionery (-18) and wine (-9).

For many consumers, the desire to nurture and protect the environment has motivated the decision to follow a vegan diet. However, the ‘low carbon’ diet could potentially attract a greater following than veganism due its relatively more flexible approach to reducing the greenhouse gas emissions associated with our diets, says GlobalData, a leading data and analytics company.

In fact, when asked what they find to be an appealing food and drink claim, 60 %* of global consumers answered ‘low carbon footprint’, compared with 39 %* of global consumers who answered ‘vegan’.

Lia Neophytou, Consumer Analyst at GlobalData, says: “Whereas veganism does not permit the consumption of any animal or animal-derived products, the low carbon diet allows for the consumption of any food/drink items as long as they align with the broader goal of reducing the carbon emissions of one’s overall diet. This could include reducing meat and dairy consumption, increasing one’s intake of local foods, and reducing food and packaging waste.”

This diet also recognizes that not all vegan foods have a low carbon footprint. For example, exotic fruits which require importation from abroad. It is for this reason that Lele’s vegan café in London recently announced that it will no longer include avocado in its dishes to avoid ‘indirectly fuelling illegal deforestation and environmental degradation’.

The appeal of a low carbon diet therefore spans consumers who are already vegan and those who simply want to reduce their carbon footprint, hence its broader appeal.

Neophytou concludes: “In future, ‘low carbon’ certifications could become mainstream and serve as a way of verifying the environmental impact of food and drink. This goes beyond simply indicating the absence of animal or animal-derived products which vegan certifications signal.”

*GlobalData’s 2019 Q3 global consumer survey

Compared to the rest of Europe, Germans attach particular importance to naturalness when buying food. Only taste and consumer friendliness are more important to German citizens. Consumers in France and the UK also pay particular attention to these two factors, followed by value for money and naturalness. In the future, the demand for natural foods could increase, especially in China. These are the results of six studies carried out by Symrise over the past two years. The Group surveyed around 15,000 consumers ages 16 to 70 from 12 countries in Europe, Asia, North America and Latin America.

The importance of naturalness differs greatly from country to country. At the same time, the researchers also identified overarching common aspects. They found that the explicit use of the word “natural” has a great influence on the perception and acceptance of a product or its ingredients. In addition, consumers around the world reject ingredients with scientific-sounding names because they do not perceive them as natural. In order for the consumer to understand and trust the content of the label, it needs concrete and transparent information. Another finding was that consumers prefer familiar methods of food preparation. Artificial sweeteners are also considered unhealthy and too sweet.

“Many consumers today want to buy the most natural food possible,” says Stefanie Hartwig, Global Marketing Engagement Manager at Symrise. “At Symrise, we respond to this preference with our code of nature® platform. This means that we value natural ingredients, gentle processing and authentic taste in our products.”

Germans want understandable ingredients

Especially in Europe, consumers are very interested in the ingredients of food. They thoroughly read even long lists of ingredients as long as they can understand them. In general, respondents attach importance to ingredients they know. On the other hand, they mostly reject unfamiliar ingredients. This also applies to very general disclosures such as the ones on vegetables. Concrete content information significantly improves acceptance. The disclosure of food additives in the form of E numbers, as practiced in the European Union, is also poorly received by consumers, especially in Germany.

In Asia, the proportion of consumers interested in natural foods varies relatively widely. While in Japan almost half of consumers prefer natural raw materials, in Thailand the proportion is about a third and in China about a quarter. China holds the greatest future potential. There are particularly good prospects in the yogurt drink and flavored water categories, if manufacturers simultaneously consider the need for health and safety.

“Natural foods offer an enormous growth market with great opportunities for manufacturers,” says Mathias vom Weg, SVP Global Purchasing Flavor at Symrise. “The challenge is to ensure naturalness throughout the value chain. We focus on transparency and traceability. With clear guidelines, we ensure that our suppliers meet our requirements for naturalness.”

Similar perception of naturalness in North America and Latin America

In the USA, consumers particularly expect naturalness in the yogurt (68 percent), soup (55 percent) and flavored water (50 percent) product categories. Respondents there primarily associate naturalness with the terms “fresh,” “natural,” “local ingredients” and “free of additives and preservatives.” This also applies to Latin America. Consumers there understand naturalness as describing a product that is real and pure without additives. Especially in beverages, Latin American consumers value natural taste, natural sweeteners and a healthy product.

As experts in what consumers want and why Mintel is best suited to accurately predict the future of consumer behaviour and what that means for companies and brands. Announced early in November, Mintel is taking a bold approach with its predictions about the future of global consumer markets by incorporating seven key factors that drive consumer spending decisions:

Wellbeing: Seeking physical and mental wellness.

Surroundings: Feeling connected to the external environment.

Technology: Finding solutions through technology in the physical and digital worlds.

Rights: Feeling respected, protected, and supported.

Identity: Understanding and expressing oneself and one’s place in society.

Value: Finding tangible, measurable benefits from investments.

Experiences: Seeking and discovering stimulation.

Here, Matthew Crabbe, Director of Mintel Trends, APAC, explores the seven drivers and how they will impact markets, brands and consumers over the next decade.

Wellbeing

“Wellbeing is no longer about simply wanting to look after oneself in broad terms, nor is it about the extremes of a total lifestyle change. Instead, a holistic approach is becoming a key motivator of consumer behaviour, underpinned by convenience, transparency, and value. Over the coming 10 years, there will be opportunities for brands to become wellbeing partners with customers. While the mass-market and ‘one-size-fits-all’ approach will still have value, we will see further adoption of bespoke solutions. Clean air and water will become selling points, while conscious movement and mindful exercise will become as important as physical fitness.”

Surroundings

“The increased global population and climate crisis are forcing people to reduce their consumption, waste, and energy use. They are learning to share limited space more efficiently and to work more collaboratively. Better and more affordable telecommunication technology allows for flexible work conditions, as consumers increasingly become digital nomads. Over the next 10 years, social tensions will increase as competition for resources rises. This could result in greater stratification of society and failure to tackle the need for more efficient use of resources and better urban planning. There will be greater pressure on cities to continue to expand, encroaching into remaining wildernesses and rural farming areas, exacerbating the cost of producing food – making even basic products more expensive for most people.”

Technology

“Mobile technology continues to blur the lines between time, travel, and location for work, learning, and leisure. Elements of virtual and augmented reality (VR/AR) will revolutionise industries like tourism and entertainment, while virtual esports will rival physical sports in popularity. Over the coming decade, consumers will push back against cashless payments and fully unmanned stores, demanding more privacy and seeking more ‘human’ interaction. We’ll also see technologies developed to mitigate the effects of climate migration and displacement, amidst the broader challenges of economic inequality and an ageing society.”

Rights

“‘Cancel culture’ is growing as consumers feel increasingly empowered to call out companies, brands, and people they disagree with, greatly shifting influence into the hands of the collective consumer. Youth activism will take the lead in drawing public awareness of causes and will push legislative leaders to develop and enact ideas to make real change. Meanwhile, a more human-centric approach to data is emerging, empowering people to control how their personal data is collected and shared. Consumers are beginning to realise the true value of this data and they are demanding more for it. Looking ahead, blockchain technology will change data ownership, empowering consumers to put the control back in their hands by determining who has access to their information online.”

Identity

“Consumers are moving away from the rigid definitions of race, gender, and sexuality, and a movement is emerging toward more fluid, self-selected identities. But as the movement grows, rising feelings of loneliness and isolation are making people feel like they are, in fact, losing their identity. While people are more connected today than ever before, feelings of loneliness and isolation are on the rise and will reach epidemic proportions by 2030. Expect to see companies, brands, social organisations, and governments create technology-based solutions to help combat this. And as identities change, so too will socialising. In the future, people will increasingly be living with members of their ‘tribe’ – dictated by their mindsets and hobbies – rather than their family.”

Value

“The current era is one of excessive and unsustainable consumption. Social media’s ‘swipe up’ culture has perpetuated the chase for buying more and buying better. However, with climate change as one of the defining issues of modern society, consumers are taking a closer look at their own consumption habits. While consumers are in search of a more mindful approach to their spending, they also desire something that is authentic and unique to them. Expect to see a move towards slower, minimal consumerism that emphasises durability and functionality. Rapid urbanisation will shrink available space in the home, office, and shared environments, demanding consumers buy less ‘stuff’.”

Experiences

“While the demand for stimulation is not new, the role it plays in consumer decision-making is evolving. No longer should ‘the experiential’ be diminished as a mere marketing tool or a fad; instead, consumers are experiencing powerful emotional connections to brands that are creating a point of differentiation. Technology is driving experiences, but the constant connectivity is also causing demand for offline interactions to become more extreme and boundary-pushing. Looking ahead, collective experiences will gain more and more popularity. People will start to redefine what experiences they want as individuals. This will include the experience of doing nothing as people make more mindful decisions about what to do with their time.”

The newly founded World Citrus Organisation (WCO) was officially launched at Fruit Attraction, Madrid. With this official presentation, citrus fruits are finally placed at the same level of coordination worldwide as other fruit categories, such as pears & apples, kiwis, avocado or red fruits, which already have their own global platforms. The WCO will act as the global platform for dialogue and action between the citrus producing countries worldwide. The core aim of the WCO is to facilitate member countries to better face common challenges and seize opportunities for the collective benefit of the citrus sector, in a spirit of cooperation and transparency.

Led by AILIMPO, the Spanish Lemon and Grapefruit Interbranch Association, and the Citrus Growers’ Association of Southern Africa (CGA), sector representatives from Argentina, Chile, Italy, Morocco, Peru, Spain, and South Africa decided to join forces to create a global citrus platform where together they may address the many multifaceted changes experienced by the citrus market over recent years. Other countries that were unable to attend the meeting have also committed to the project, and the remaining global producers are invited to join the organization.

The primary objective of the WCO is to facilitate collective action in the citrus sector, for both fresh and processed categories. Most recently the sector has been faced with an extensive array of significant issues of global concern including growth in production, overlapping of seasons, changing climate conditions resulting in varied quality and biosecurity challenges, increased competition within the citrus category and between other fruit categories and food products as well as stagnating fruit consumption. The WCO will facilitate member countries to better face these common challenges and identify opportunities for the collective benefit of the citrus sector.

Specifically, the WCO’s mission is to:

Discuss common issues affecting citrus producing countries.

Exchange information on production and market trends to prepare for the next decade to come.

Foster dialogue on policy issues of common concern.

Identify and promote Research and Innovation projects specific to the citrus sector.

Liaise with public and private stakeholders on citrus-related matters to highlight the importance of citrus producers and the need for a fair return.

Promote the global consumption of citrus.

During the official presentation in Madrid, the Director General of Agricultural Production and Markets of the Spanish Ministry of Agriculture, Esperanza Orellana, congratulated the citrus sector for the initiative, emphasizing the importance for Spain, leader in the production and export of citrus fruits, to be at the forefront of this project. The Counsellor of the Region of Murcia, Antonio Luengo, also greeted the participants and expressed his support for the new organisation. “It is important that the world citrus community works together to face common challenges and learn from each other,” he said, adding that, leaving aside the competitive factor, it is essential to share information and experiences for the collective benefit of the sector, which is of key strategic importance for Murcia and for Spain.

Freshfel Europe, the European Fresh Produce Association, whose Secretariat is based in Brussels, Belgium, will coordinate and administer the WCO. The next meeting, where the formalities for the foundation and future structure of the organisation will be formalized, will take place at FruitLogistica 2020 in Berlin.

As one of the only industries that can connect environment at a personal level to the individual, by also talking about health, Food and Beverage brands have an opportunity to drive change through the way they communicate with consumers on these converging topics, to meet this growing and pressing need.

This year’s global research study conducted by Tetra Pak, in partnership with Ipsos, investigates the convergence of health and environment and reveals six new segments of consumers. Each group has unique attitudes around both health and environment, which present clear opportunities for targeted products and messaging for Food and Beverage brands.

Europe’s drinks industry saw a rise of 73.9 % in overall deal activity during Q2 2019, when compared to the four-quarter average, according to GlobalData, a leading data and analytics company.

A total of 40 deals worth $76.18m were announced for the region during Q2 2019, against the last four-quarter average of 23 deals.

Of all the deal types, merger and acquisition (M&A) saw the most activity in Q2 2019 with 24, representing a 60 % share for the region.

In second place was venture financing with ten deals, followed by private equity deals with six transactions, respectively capturing a 25 % and 15 % share of the overall deal activity for the quarter.

In terms of value of deals, M&A was the leading category in Europe’s drinks industry with $55.98m, while venture financing deals totaled $20.2m.

Europe drinks industry deals in Q2 2019: Top deals

The top five drinks deals accounted for 80.9 % of the overall value during Q2 2019.

The combined value of the top five drinks deals stood at $61.65m, against the overall value of $76.18m recorded for the quarter. The top announced drinks deal tracked by GlobalData in Q2 2019 was Cafento Coffee Factory S.L’s $33.58m acquisition of Java Republic.

In second place was the $20.39m asset transaction with The Glenturret by Lalique Group and in third place was Five Seasons Ventures and New Ground Ventures’ $4.73m venture financing of YFood Labs.

The $1.68m venture financing of Champagne EPC by Cedric Sellin, Cedric Sire and Kima Ventures and AG Barr’s stake acquisition of Elegantly Spirited for $1.27m held fourth and fifth positions, respectively.

Total drinks industry merger and acquisition (M&A) deals in Q2 2019 worth $2.11bn were announced globally, according to GlobalData, a leading data and analytics company.

The value marked an increase of 74.6 % over the previous quarter and a drop of 44.1 % when compared with the last four-quarter average, which stood at $3.78bn.

Comparing deals value in different regions of the globe, North America held the top position, with total announced deals in the period worth $2.01bn. At the country level, the US topped the list in terms of deal value at $2bn.

In terms of volumes, Europe emerged as the top region for drinks industry M&A deals globally, followed by North America and then Asia-Pacific.

The top country in terms of M&A deals activity in Q2 2019 was the US with 18 deals, followed by the UK with seven and Spain with four.

At the end of Q2 2019, drinks M&A deals worth $3.32bn were announced globally, marking a decrease of 87.2% year on year.

Drinks industry M&A deals in Q2 2019: Top deals

The top five drinks industry M&A deals accounted for 98.2% of the overall value during Q2 2019.

The combined value of the top five drinks industry M&A deals stood at $2.08bn, against the overall value of $2.11bn recorded for the quarter. The top announced drinks industry M&A deal tracked by GlobalData in Q2 2019 was E. & J. Gallo Winery’s $1.7bn asset transaction with Constellation Brands.

In second place was the $300m acquisition of Dogfish Head Brewery by The Boston Beer and in third place was Cafento Coffee Factory S.L’s $33.58m acquisition of Java Republic.

The $21.62m asset transaction with McLeod Russel India by Luxmi TeaLimited and Lalique Group’s asset transaction with The Glenturret for $20.39m held fourth and fifth positions, respectively.

The global cold pressed juice market is segmented by category into conventional and organic; by type into fruits, vegetables and blends; by distribution channels into store based and non-store based and by regions. The global cold pressed juice market is estimated to grow at a CAGR of around 10 % over the forecast period i.e. 2019-2027.

The cold pressed juice market is anticipated to maintain a significant growth rate on the back of rising disposable income levels, awareness among consumers concerning healthy food & drinks, and easy availability of cold pressed juices. On the basis of category, cold pressed juice market is segmented into conventional and organic. Out of which organic is expected to be dominant segment as a result of shifting trends towards consummation of organic juices and increasing per capita income in developing economies across the globe.

North America cold pressed juice market is anticipated to witness fast growth. This growth is attributed to the rise in the implementation of latest technologies in packaged food & beverages industry, changing lifestyle of consumers, and existence of well-established industrial infrastructure in the region. Growing awareness among consumers regarding health benefits of sugar-free and organic juices are some another factors that drives the growth of regional market.

Growing Concerns Regarding Various Health Issues

Growing concerns regarding various health issues, while simultaneously growing number of health benefits associated with consuming cold pressed juices are estimated to boost the growth of cold pressed juice market. Rising health awareness among consumers is gradually causing a shift towards the consumption of beverages that are calorie-free, caffeine-free, and free from artificial ingredients. Numerous factors such as changing lifestyle, changing food patterns, and rising health consciousness among younger section of the society are likely to result in considerable growth of cold pressed juice market during the forecast period.

However, use of organic flavors and adoption of the high pressure processing (HPP) manufacturing processes, makes them expensive. Thus, in terms of cost, cold pressed juices are anticipated to witness significant hindrance in term of the market growth in comparison to its substitutes.

The report titled “Cold pressed juice Market: Global Demand Analysis & Opportunity Outlook 2027” delivers detailed overview of the cold pressed juice market in terms of market segmentation by category, by type, by distribution channels and by regions.

Further, for the in-depth analysis, the report encompasses the industry growth drivers, restraints, supply and demand risk, market attractiveness, BPS analysis and Porter’s five force model.

This report also provides the existing competitive scenario of some of the key players of the global cold pressed juice market which includes company profiling of Coca Cola / Odwalla, Hain Blue Print Inc., Starbucks / Evolution Fresh, Suja Life, LLC, Pressed Juicery, Juice Generation, Florida Bottling, Drink Daily Greens, Liquiteria and Other Prominent Players. The profiling enfolds key information of the companies which encompasses business overview, products and services, key financials and recent news and developments. On the whole, the report depicts detailed overview of the global cold pressed juice market that will help industry consultants, equipment manufacturers, existing players searching for expansion opportunities, new players searching possibilities and other stakeholders to align their market centric strategies according to the ongoing and expected trends in the future.

Tetra Pak announced the appointment of Charles Brand to the position of President of Tetra Pak Europe & Central Asia (E&CA) Region and he will continue to be a member of the company’s Global Leadership Team.

Charles joined Tetra Pak in 1985 as an Electronics Development Engineer and has since held several key senior roles in the company, like Vice President of R&D for Tetra Rex® , Managing Director of one of the key business units of Tetra Pak and Managing Director Tetra Pak Taiwan, before taking on his last position as Executive Vice President, Product Management & Commercial Operations. On his appointment, Charles Brand said, “I am delighted to lead our activities in the E&CA region. This role is a great opportunity for me to continue to position Tetra Pak as a leader in the industry and in supporting the evolving needs of our customers across the region, with a focus on our common sustainability and digitalisation agendas.” Charles holds an MSC in Electrical Engineering degree from the Technical University of Lund in Sweden.

Topping the 2019 global index of the 100 most sustainable companies, as announced during the World Economic Forum in Davos, Switzerland

One month short of its official 145th anniversary, global bioscience company Chr. Hansen is ranked the most sustainable company in the world by Corporate Knights, a specialized Toronto-based media and investment research firm.

This was announced during the World Economic Forum in Davos, Switzerland, on January 22, 2019, upon the release of Corporate Knights’ 15th annual Global 100 Most Sustainable Corporations in the World ranking. More than 7,500 companies have been analyzed against global industry peers on a number of quantitative key performance indicators. Chr. Hansen scored 100 % on the ‘clean revenue’ indicator, reflecting that the company’s products have clear environmental and certain social benefits, as stated in Corporate Knights’ definition.

The power of good bacteria

“We are extremely proud and humble to receive this amazing honor. I believe that one of the reasons why Chr. Hansen has been ranked as #1 is because the world is beginning to understand the power of good bacteria and the impact it can have on some of the major challenges the world is facing, such as food waste, antibiotic overuse and the need for a more sustainable agricultural sector to feed a growing world population while preserving our planet for future generations,” says CEO Mauricio Graber.

“Chr. Hansen is dedicated to promoting a wider adoption of natural solutions, and we are truly proud of our products which are consumed by more than 1 billion people every day. Having a global reach like that is indeed a great responsibility as well as an opportunity to make a positive difference for people, animals and plants. We are fortunate to have customers all over the world who are with us on this journey – determined to promote sustainable and natural products to the end-user,” Graber elaborates.

“We have, among other things, been recognized for our efforts to measure our impact on the UN Global Goals; 82 % of our revenue directly supports these goals, and PWC has reviewed our methodology to document this.”

Sustainability – an integral part of the business

Chr. Hansen has been supplying natural ingredients to the food industry since 1874. The understanding and respect for nature’s scarce resources has always been an integral part of the company’s DNA.

Today sustainability remains at the core of Chr. Hansen, reflected by the name of the corporate strategy 2022: ‘Nature’s No. 1 – Sustainably’. The strategy focuses on developing natural solutions for the global food, health and agricultural industries in a sustainable manner. The UN Global Goals are used as a framework to link the impact of the corporate strategy to sustainable development, and the performance is measured and reported on an annual basis.

“Working for a better world is deeply rooted in our product portfolio and organizational culture. As a company this gives us a very strong purpose that is closely linked to sustainability, and which our employees fully identify with. They are proud of working for a meaningful cause and contributing to a higher purpose every day,” underlines Mauricio Graber.

“However, we are far from done. We still have a long way to go on our sustainability journey, but we sincerely hope that we can use this accolade to raise more awareness of the power and potential of good bacteria as part of a sustainable solution to a number of challenges facing our planet,” he concludes.

The world market for aseptically packed products amounted to 152 billion litres in 347 billion packs during 2017, according to the new Global Aseptic Packaging report from leading food and drinks consultancy Zenith Global Ltd and packaging experts Warrick Research Ltd. Volumes have risen by 2.7 % a year since 2012, with South East Asia achieving the fastest annual growth rate of 7 %, followed by China on 6 %.

Beverages such as fruit juice accounted for 39 % of aseptically packed products, with white drinking milk responsible for 38 % and other dairy/food products making up the remainder. Aseptic filling has also become established for soups, sauces, tomato products and baby foods.

“While European companies still dominate the global aseptic filling equipment industry, the Chinese market is increasingly supplied by Chinese equipment manufacturers, some of whom have also successfully entered other Asian markets,” commented David Warrick, Director at Warrick Research Ltd. “Volumes have been static in much of Europe, contrasting with rapid growth in many Asian countries,” added Arunkumar Anbalagan, Senior Insights Analyst at Zenith Global Ltd.

Other findings of the 2018 Global Aseptic Packaging report include:

There are over 16,000 operational aseptic filling systems worldwide, serviced by more than 30 suppliers.

The largest markets for aseptic packaging are China and South East Asia. China is set to become the leading country by 2022, followed by South East Asia and West Europe.

Value added dairy products are a fast growing area of demand for aseptic filling systems. In some regions, fillers are used for both ambient and chilled dairy products.

Environmental issues have become more important in many regions. Developments include the introduction of electron beam sterilisation as an alternative to chemical sterilisation. Demand is increasing for re-use or recycling.

By 2022, Zenith and Warrick estimate that the world market will reach 176 billion litres and 410 billion packs. The majority of additional demand will come from South East Asia as well as China.

What will be the next hype after the turmeric latte?

Turmeric latte, or “golden milk”, was 2017’s dairy-based sensation. The golden-hued drink featured on menus of trendy cafés, and also emerged in chilled packaged formats. According to Mintel Global New Products Database (GNPD), hot beverage launches in Europe containing turmeric have more than quadrupled since 2013, growing by 359 % between 2013 and 2017.

Julia Büch, Food & Drink Analyst at Mintel, explains the trend:

“The turmeric latte is inspired by a traditional Indian remedy based on hot milk and turmeric infused with spices such as pepper, cinnamon and ginger. The drink has purported health benefits, but equally, its appeal comes from the photogenic and intense, social media-friendly colour. Milk has not traditionally been a trendy or social media-worthy drink, but colourful, flavourful offerings such as the turmeric latte could change that.”

And there is clear consumer interest in such beverages: 35 % of Germans aged 16-34 would like to see more flavoured milk launches, such as chocolate or spices. Even 77 % of German consumers aged between 35 and 54 say that they like to explore new flavours. The near future will see dairy brands looking to other new colours and textures to create the next trendy, attention- getting and ‘social media-worthy’ dairy drink.

Julia elaborates:

“Future formulations could include fizzy milk, new colors and new textures. Fizzy milk, for example, is already a popular concept in China and other parts of Asia. Colourful matcha or spirulina could be the next buzz-worthy ingredient in the West, where they are currently less known. As Mintel’s 2018 Global Food and Drink Trend ‘New Sensations’ explains, the next evolution will bring texture into the limelight. Already, we can see new foaming ingredients that infuse drinks with an unexpected texture such as the tea macchiato from China – a drink that blends tea with whipped cream cheese.”

Indeed, although matcha has been around for centuries, it is only now booming in Europe. Hot beverage launches containing matcha have increased more than tenfold in Europe between 2014 and 2017 and its vibrant green colour is already finding use in eye-catching matcha lattes. Spirulina is one of Mintel’s Trend ingredients for 2018, and is quickly becoming a trendy ingredient in the food service industry and with blue ‘mermaid lattes’ appearing across Instagram feeds.

Global launches of carbonated soft drinks with dairy ingredients, or ‘fizzy milk’, have also grown over the past five years, albeit from a small base. Asia Pacific currently accounts for 86 % of fizzy milk launched in 2017. The combination of carbonation and dairy can create a creamy texture that is rare in carbonated drinks. This novel texture innovation is primed to be ‘the next big thing’ according to Mintel research’.

Global consumption of ready-to-drink coffee reached 5,500 million litres in 2017, a 19 % increase since 2012, according to a new report from global food and drink experts Zenith. Further growth is forecast, with sales expected to exceed 6,600 million litres in 2022.

“Japan is by far the biggest market, with 55 % of global volume, and is relatively mature with a significant proportion heated in vending machines,” commented Zenith Chairman Richard Hall.

“Much of the dynamism is coming from North America, with annual growth of 13 % and the introduction of many new trends such as cold brew, nitrogen infusion, carbonation and black coffees,” he continued. “Iced coffees are also gaining ground worldwide from low levels because of their taste, refreshment, convenience and quality.”

In terms of regional shares, Asia Pacific leads with 83 % of total volume, followed by North America and Europe with 10 % and 3 % respectively. Consumption has increased across all regions since 2012, spurred by new product development and increasing interest in healthier beverage choices.

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.