The 2023-2024 Florida all orange forecast released by the USDA Agricultural Statistics Board is 20.5 million boxes, unchanged from the October forecast. If realised, this will be 30 percent more than last season’s final production. The forecast consists of 7.50 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 13.0 million boxes of Valencia oranges. An 8-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma, and the 2022-2023 season, which was affected by Hurricanes Ian and Nicole. Average fruit per tree includes both regular bloom and the first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

Total forecast production of oranges1 updated to 307.22 million boxes

The second forecast for the 2023-2024 orange crop in the São Paulo and West-Southwest of Minas Gerais citrus belt, published by Fundecitrus, in cooperation with Markestrat, FEA-RP/USP, and FCAV/Unesp2, is 307.22 million boxes of 40.8 kg each. Of this total estimated production, approximately 27.60 million boxes are expected to come from the Triângulo Mineiro region.

In this update, the initial projection is reduced by 2.12 million boxes, corresponding to 0.7 %. This adjustment reflects the balance considering all varieties. The oranges from early varieties, already harvested almost entirely, benefited from abundant rains at the beginning of the year, resulting in a production exceeding the estimated 2.27 million boxes …

1Hamlin, Westin, Rubi, Valencia Americana, Seleta, Pineapple, Alvorada, Pera Rio, Valencia, Valencia Folha Murcha and Natal. 2Department of math and science, FCAV/Unesp Jaboticabal Campus.

The World Citrus Organisation (WCO) has released its annual Northern Hemisphere Citrus Forecast for the upcoming citrus season (2023-24). The Forecast was released on the occasion of the Global Citrus Outlook conference organized by WCO. The forecast is based on data from Egypt, Greece, Israel, Italy, Morocco, Spain, Tunisia, Turkey, and the United States. This year, the Forecast shows that citrus production is projected to reach 28,976,001 T, which represents a 12.2 % increase compared to the previous peak low season. The 2023/2024 forecast is 1.48 % higher than the average of the last 4 seasons.

WCO, the World Citrus Organisation, released its annual Northern Hemisphere citrus forecast for the upcoming season (2023-24). The preliminary Forecast is based on data from industry associations from the Mediterranean region and the United States. Total citrus exports are expected to follow a similar trend at 9,483,770 T, up by 11.4 % from last season and 4.5 % from the last four seasons’ average.

Philippe Binard, WCO Secretary General, summarised the outcome of the Forecast. “The market insights we received indicate a recovery from the low point of last season. The growth is mainly influenced by growth in Turkey and Egypt while other countries are stable or only recorded marginal gains”. Eric Imbert from CIRAD added, “While this year’s forecast shows a recovery with variable conditions across the producing countries and citrus categories, many parameters have to be taken into account for the market analysis”. He added: “Climatic issues, such as late frost, drought, heat waves, or new pests and diseases influenced the quality, colouring, or harvest date for the production. The market will still be impacted by geopolitical instability while consumer demand is under pressure due to limitation of purchasing power and inflation”.

Looking at the country-specific figures for the largest producers in the EU, Spain’s citrus production at 5.9 MT is up by 2 % to previous seasons, with stable soft citrus compared to last year, fewer oranges (- 6 %) and more lemons. Italy is up by 6 % at 2.6 MT, with more oranges (+ 20 %) and less soft citrus and lemons (- 10 % each), while Greece is down by 7 % to 1.1 MT. In the other Mediterranean countries, Turkey is now the market leader with a first production estimate of 6.5 MT (+ 45 %), with strong growth across all categories. The Turkish production forecast could even exceed 7 MT. This results from the increased acreage and productivity, alternance, and favourable climatic conditions. Egypt at 5.4 MT is up by 10 % from the previous season and 15 % from the average of the last 4 years. The main category is oranges with 3,7 MT (+ 5 %) while soft citrus’s double-digit growth should almost reach 1.3 MT. Morocco’s production is expected to partially recover, bouncing back to just over 2 MT, with 1 MT of soft citrus (+ 11 %) and 930,000 T of oranges. Israel’s production is estimated at 365,000 T, but the recent conflict and attack on the country is a source of multiple challenges regarding supply, logistics, and human resources for harvesting and packing. The production in the United States will be up by 1 % at 4.5 MT with more oranges ( + 10 % at 2.4 MT) but less soft citrus (- 2 % at 856,000 T) and even less so for lemon ( – 12 % at 889,000 T).

Philippe Binard added: “WCO is also setting some trends for the expected utilization of citrus for the upcoming season. The global citrus exports will be up by 11 % to reach 9,4 MT, while processing will increase by 8 % to reach 4,7 MT, leaving 14.7 MT for domestic sales (+ 14 %.). Next April, the WCO will release the 2024 production and export forecast for the Southern Hemisphere.

All Oranges 20.5 Million Boxes

The 2023-2024 Florida all orange forecast released by the USDA Agricultural Statistics Board is carried forward from October at 20.5 million boxes, up 30 percent from last season’s final production. The total includes 7.50 million boxes of non-Valencia oranges (early, midseason, and Navel varieties) and 13.0 million boxes of Valencia oranges. The Navel orange forecast, at 300,000 boxes, accounts for 4 percent of the non-Valencia total …

Please download the full citrus crop production forecast: www.nass.usda.gov

All Oranges 20.5 Million Boxes

The 2023-2024 Florida all orange forecast released by the USDA Agricultural Statistics Board is 20.5 million boxes, up 30 percent from last season’s final production. The total includes 7.50 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 13.0 million boxes of Valencia oranges. The Navel orange forecast, at 300,000 boxes, accounts for 4 percent of the non-Valencia total.

The estimated number of bearing trees for all oranges is 38.7 million. Trees planted in 2020 and earlier are considered bearing for this season. Field work for the latest Commercial Citrus Inventory was completed in June 2023. Attrition rates were applied to the results to determine the number of bearing trees used to weigh and expand objective count data in the forecast model.

An 8-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma, and the 2022-2023 season, which was affected by Hurricanes Ian and Nicole. Average fruit per tree includes both regular bloom and the first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

With the first part of this year’s harvesting on its way, the World Apple and Pear Association (WAPA) has started revising its annual Apple and Pear Crop Forecast based on the latest insights from its members on the season. The first EU apple estimates, which were released on 3 August 2023 during the Prognosfruit Conference, indicated a 3,3 % decrease compared to last year, to a total of 11.410.681 t. The EU pear crop for 2023 was estimated to decrease by 12,9 % compared to last year’s crop with a total of 1.745.632 t.

The early forecast is released during Prognosfruit, when harvesting is just about to start. The crop can therefore still be impacted by nature and climatic factors up to late October, with either a positive or negative impact on the quantity and quality of the harvest. Historically, these adjustments to the forecast amounted to small percentage variations.

The first updates from Prognosfruit’s network of national producing associations indicate that climate change- related conditions negatively affected the crop in the weeks following the publication of the original estimates. The climatic havoc included droughts, floodings, hail, warm nights, and an increased risk of pests across the EU. In other cases, rains and colder nights have positively impacted the size development and colouring respectively in some producing regions.

Regarding this season, while the apple harvesting is still expected to carry on for several weeks, based on the first regional adjustments (both upward and downward) WAPA estimates that the 2023 apple crop is expected to settle at just below 11 million t (about 4 % lower than the original forecast).

In regard to pears, a further decline of the forecast in Italy, Spain, Belgium, and the Netherlands will lead to a lower crop, even lower than in 2021. The final pear crop is expected to be around 1.720.000 T, about 6 % lower than the initial forecast.

WAPA will continue to monitor closely the harvesting developments in Europe, with the objective of consolidating the most accurate and recent figures into its final Crop Forecast later this year once harvesting is completed.

Orange production is expected to be low in Florida for one more year. According to estimates from the USDA released on October 12th, the harvest of the 2023/24 crop in FL is forecast to total 20.5 million boxes of 40.8 kilograms each, of which 7.5 million of early and mid-season varieties and 13 million, valência oranges.

Although that volume is considered low, it is still 30 % higher than that from last season, when two hurricanes hit Florida – Ian, in September 2022, and Nicole, in November 2022. Although hurricane Idalia hit Florida State in late August/23, damages were not that severe.

It is important to mention that this output is not enough to meet the demand from the US, thus, the country is expected to continue to import high amounts of orange juice – and Brazil is the major supplier of the commodity to them. This scenario becomes worse when the local inventories are considered, since they are decreasing year after year.

Brazilian market

Liquidity was high in the Brazilian orange market in the first fortnight of October, despite the holiday on the 12th (Day of Our Lady of Aparecida). According to Cepea collaborators, lower supply and higher demand underpinned prices. On the other hand, for tahiti lime, values dropped, influenced by lower demand and rising supply.

The higher demand for orange juice from the United States raised the Brazilian exports of the commodity in the first two months of the 2023/24 exporting season (July and August). The average price paid for the national juice increased in that period too, influenced by low inventories and the lower output in Brazil. The higher volume exported and the valuation of the Brazilian juice abroad resulted in a significant increase in the revenue of exporters.

According to data from Secex (Foreign Trade Secretariat), Brazil exported 182.9 thousand tons of Frozen Concentrate Orange Juice (FCOJ) Equivalent in July and August, 4% more than the volume shipped in the same period of 2022. Revenue totaled USD 397.9 million, a staggering 20% up in the same comparison.

As for the types of juice exported, shipments of Not-From-Concentrate (NFC) orange juice increased 19 %, and revenue, 25 %; of FCOJ, the volume exported decreased 3 %, while the revenue rose 17 %. The different performances of the exports of these types of juice are linked to the higher demand from the US for NFC juice, whose volume sent to the North-American country rose a staggering 51 %.

The United States

For one more season, the US have been importing orange juice from Brazil. In the first two months of the current season (23/24), the US imported 50.5 thousand tons of FCOJ, an increase of 38 % compared to that in the same period of 2022/23. Revenue totaled USD 113.2 million, 57 % higher, in the same comparison.

Lower orange production in the US because of the 2022/23 crop of Florida – which has decreased 62 %, according to the USDA – and lower supply from Mexico, the second major supplier of orange juice to the US, led the country to raise imports from Brazil.

European Union

To the European Union, Brazil exported, in July and August, 112.6 thousand tons of orange juice, a slight 3 % up from that last season. Revenue totaled USD 241.9 million in the two first months of the season, 14 % higher, in the same comparison.

Crop Estimates

According to data released this week by Fundecitrus, the 2023/24 harvest in the citrus belt (São Paulo State + the Triângulo Mineiro) is expected at 309.34 million boxes of 40.8-kg each, stable compared to that estimated in May but 1.5 % lower than the output from last season. It is important to highlight that this volume is a lot lower than the industry’s needs to meet the demand from abroad and replenish inventories, which are currently very low.

Orange Juice

Global orange juice production for 2022/23 is estimated 9 percent lower to 1.5 million tons (65 degrees brix). Production is down due to reduced fruit available for processing in Brazil, the European Union, Mexico, and the United States. Consumption is mostly flat while exports are estimated down with the reduced available supplies …

The Prognosfruit Conference, Europe’s leading annual event of the apple and pear sector, is right around the corner. On 2-4 August 2023, the Italian region of Trentino (Italy) will welcome an estimated 300 delegates from Europe and beyond. Registration is still open for sector representatives interested in getting the latest updates on the preparations for the upcoming apple and pear season.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in Trentino, Italy, from the 2nd to the 4th of August 2023. Prognosfruit 2023 is organised by WAPA in cooperation this year with APOT (Associazione Produttori Ortofrutticoli Trentini). After more than 20 years, the Italian region of Trentino is ready to welcome back a delegation of 300 leaders from the apple and pear sector from Europe and beyond. Registration is open on the Prognosfruit website until 25 July 2023, along with all the information to book accommodation in Trento.

The complete programme of Prognosfruit 2023 is available on the Prognosfruit website. The three-day event will gather the most important representatives of the sector to learn about the upcoming European apple and pear production and latest market trends, covering as well as the EU neighbourhood and the USA, China, and India. Philippe Binard, Secretary General of WAPA commented: “Prognosfruit is a long-established event for the European apples and pears sector. It has been on the agenda of the sector for 48 years. Besides the session that will reveal the key features for the Northern Hemisphere 2023/2024 apple and pear production forecast and corresponding market analysis, we are pleased this year to complement the programme with insightful new sessions on the demand side with an organic market outlook and a retail panel on adapting to consumer’s expectation. Mr Binard added “Despite on-going challenges of rising costs impacting both the sector and consumers and unpredictable climatic events, the first indicators for both apples and pears look very promising and will lead to interesting exchange during the conference in the middle of one of the most important production places”. To facilitate the debate, simultaneous translation will be available in Italian, English, French, and German.

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 15.9 million boxes. The total is comprised of 6.15 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties), unchanged from the June forecast, and 9.70 million boxes of Valencia oranges, up 100,000 boxes from the June forecast. The forecast of all Florida grapefruit production is lowered 10,000 boxes to 1.81 million boxes. Of the total grapefruit forecast, 250,000 boxes are white, and 1.56 million boxes are the red varieties. The Florida all tangerine and tangelo forecast is now 480,000 boxes. …

Please download the full citrus crop production forecast: www.nass.usda.gov

World apple production for 2022/23 is forecast down 4.3 million metric tons (tons) to 78.4 million on weather‐induced losses in China. Exports are estimated down over 1.0 million tons to 5.5 million on significantly reduced shipments from China, Iran, and Moldova.

China production is expected to shrink nearly 5.0 million tons to 41.0 million on reduced output in the top‐producing provinces of Shaanxi and Shandong as high temperatures during bloom reduced fruit set. Low market returns are encouraging tree removals in several northern and western provinces, while an aging farmer population is also impacting management of orchards. Exports are estimated to drop over 20 percent to 770,000 tons as a result of lower supplies. Shipments to Russia have resumed after an August 2019 ban due to pests was lifted in February 2022, but these volumes are expected to only partially offset weaker sales to other markets. Imports are projected up 10,000 tons to 85,000 on greater shipments from New Zealand at the start of the marketing year (July‐June) …

The Prognosfruit Conference is Europe’s leading annual event for the apple and pear sector, gathering growers from across Europe and beyond. Following last year’s successful return as an in-person event, Prognosfruit 2023 will take place in Trentino, Italy, from the 2nd to the 4th of August 2023. Registration is now open, and stakeholders and journalists are welcome to register via the Prognosfruit website.

Prognosfruit, the leading annual event for the apple and pear sector, will take place in Trentino, Italy, from the 2nd to the 4th of August 2023. Prognosfruit 2023 is organised by WAPA in cooperation with APOT (Associazione Produttori Ortofrutticoli Trentini). Registration is now open on the Prognosfruit website.

Alessandro Dalpiaz (APOT) commented on the event’s return to Trentino: “We are honoured to host in Trentino the most important international conference dedicated to apples and pears. Prognosfruit is certainly an important opportunity to present to the participants the ability of an organised system to deal with environmental issues, geopolitical crises, and market uncertainties. Prognosfruit also represents an occasion to bring the attention of the participants to those understated yet relevant values of mountain areas, with their arts, traditions, stories, and landscapes that attract and make millions of visitors think every year”.

Since 1976, Prognosfruit has released the annual forecast of apple and pear production for the upcoming season. This year, the three-day event during which the report will be released will see representatives of the sector gather to discuss the Northern Hemisphere situation as well as global perspectives for apples and pears. Following the Prognosfruit Conference on August 3rd, the delegates will have the opportunity to participate in technical and cultural visits to Melinda’s Underground Warehouses, San Romedio Sanctuary, and Valer Castle.

WAPA Secretary General Philippe Binard stated: “Last year’s edition reminded us all how important Prognosfruit and its three-day programme are for the apple and pear sector. Prognosfruit provides the opportunity for the delegates to meet up and discuss the latest developments and the future of the market, which is especially important in challenging times like the ones the sector is currently dealing with”.

The draft programme of Prognosfruit 2023 and the online registration form to attend the conference are both available on the Prognosfruit website.

2023 -2024 orange crop forecast

The 2023 – 2024 orange crop forecast for the São Paulo and West-Southwest Minas Gerais citrus beltby Fundecitrus in cooperation with Markestrat and full professors at FEA-RP/USP and FCAV/Unesp, is 309.34 million boxes (40.8 kg). Total orange production includes:

56.11 million boxes of the Hamlin, Westin and Rubi varieties;

18.22 million boxes of the Valencia Americana, Seleta, Pineapple and Alvorada;

98.95 million boxes of the Pera Rio variety;

105.23 million boxes of the Valencia and Valencia Folha Murcha varieties;

30.83 million boxes of the Natal variety.

Approximately 27.02 million boxes are expected to be produced in the Triângulo Mineiro region.

The projected volume is lower only by 1.55 percent as compared to the previous crop, which totaled 314.21 million boxes. That minor difference maintains the production at the same level as in the previous crop season and within the average range for the last ten years, as shown in Graph 1. As compared to the average volume produced in the last decade, the current crop shows a slight increase of 1.04 percent …

Orange production for the 2022-2023 crop season totaled 314.21 million boxes1

The 2022-2023 orange crop for the São Paulo and West-Southwest Minas Gerais citrus belt, published on April 10, 2023 by Fundecitrus – performed in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp2 – is 314.21 million boxes of 40.8 kg each (90 lbs), divided as follows …

1Hamlin, Westin, Rubi, Valencia Americana, Seleta, Pineapple, Alvorada, Pera Rio, Valencia, Valencia Folha Murcha and Natal. 2Department of math and science, FCAV/Unesp Jaboticabal Campus.

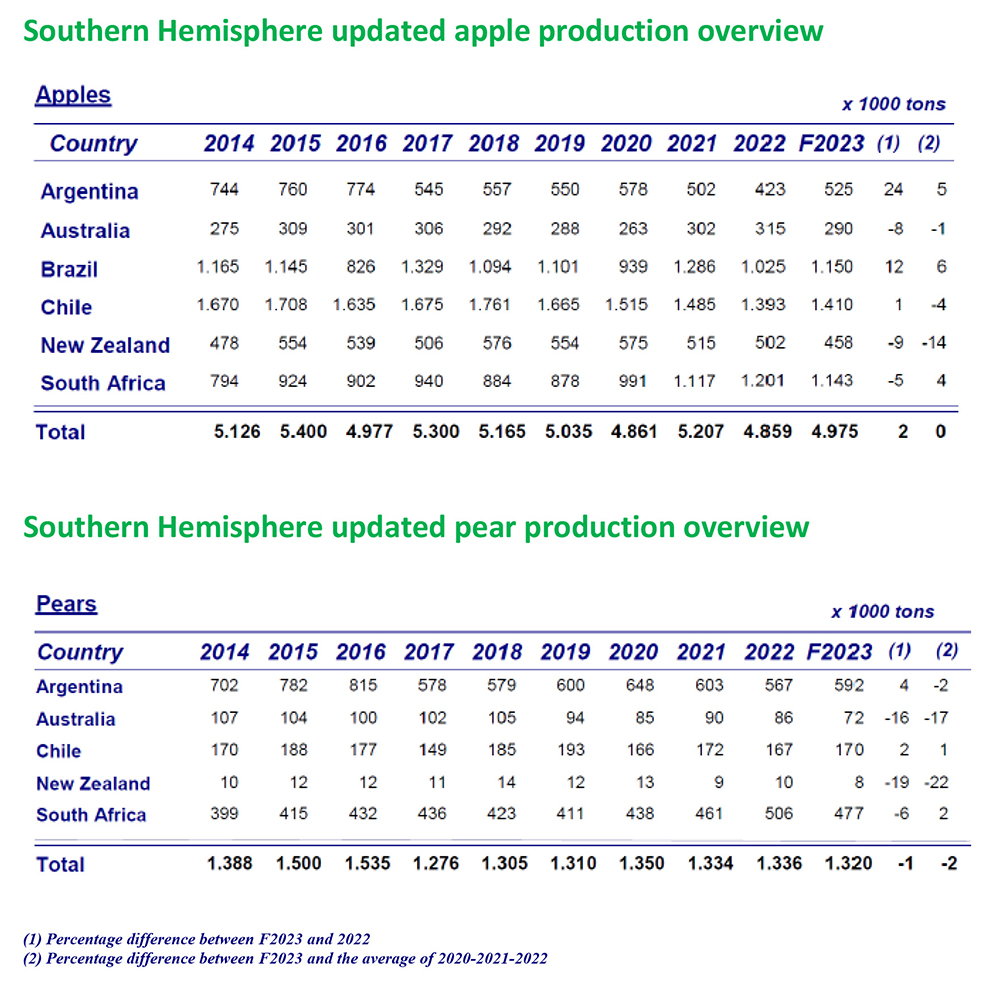

Following the intense weather events that affected several countries in the Southern Hemisphere, the World Apple and Pear Association (WAPA) has released an update of the Southern Hemisphere apple and pear crop forecast that was originally presented during the Association’s latest Annual General Meeting in Berlin’s Fruit Logistica. According to the revised forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple production is set to increase by 2,38 % to reach 4.974.990 T, while pear production is expected to decrease by 1,25 % to a total of 1.319.601 T.

During its latest Annual General Meeting in Berlin’s Fruit Logistica, the World Apple and Pear Association (WAPA) presented the Southern Hemisphere apple and pear crop forecast for the upcoming season. The yearly report is compiled with the support of ASOEX (Chile), CAFI (Argentina), ABPM (Brazil), Hortgro (South Africa), APAL (Australia), and New Zealand Apples and Pears, and therefore provides consolidated data from the six leading Southern Hemisphere countries. The initial forecast for the 2023 season, which estimated a 6 % and 1 % increase for apples and pears respectively compared to 2022, has been revised in light of the intense weather events that affected several countries in the Southern Hemisphere. New Zealand’s and South Africa’s apple crop forecasts have been revised downward by 77.902 T and 77.276 T respectively. New Zealand’s pear crop estimates have also been slightly decreased compared to the initial forecast (- 323 T), as well as South Africa’s (- 28.726 T).

Regarding apples, the updated Southern Hemisphere 2023 crop forecast suggests an increase of 2 % to a total of 4.974.990 T compared to last year (4.859.026 T). A smaller apple crop is expected in New Zealand, (457.675 T, – 9 % compared to 2022), Australia (- 8 % compared to 2022, to a total of 290.000 T), and South Africa (1.142.880 T, down 5 %). Chile remains the largest producer (1.409.633 T, in line with 2022), now followed by Brazil (1.150.000 T, + 12 %). Argentina’s apple production should reach 525.000 T (+ 24 % compared to 2022). Exports are also expected to decrease (- 3 % compared to 2022) to a total of 1.556.668 T. Chile remains the largest exporter (604.000 T) followed by South Africa (509.158 T), whose exports are forecasted to decrease by 10 %. Exports from New Zealand (286.823 T) and Australia (2.687 T) are also expected to decrease by 15 % and 1 % respectively. Brazil’s (70.000 T) and Argentina’s exports (84.000 T), on the other hand, are expected to recover from the low 2022 figures. With 1.843.130 T, Gala remains by far the most popular variety, with its production expected to increase by 4 % compared to 2022.

Regarding pears, the Southern Hemisphere growers predict a slight decrease of the crop (- 1 %), which will drop to 1.319.601 T. While Argentina and Chile are expected to increase their production by 4 % and 2 % respectively, South Africa’s (- 6 %), Australia’s (- 16 %), and New Zealand’s (- 19 %) production levels are all expected to decrease. Argentina remains the largest producer in the Southern Hemisphere (592.000 T), followed by South Africa (477.419 T), Chile (170.000 T), Australia (72.016 T), and New Zealand (8.120 T). Packham’s Triumph remains the most produced variety (481.049 T, in line with 2022), followed by Williams’ bon chrétien pears (332.447 T). Export figures are expected to be stable (670.054 T), with a 12 % increase in Argentinian exports and a 13 % decrease in exports from South Africa.

(Photo: WAPA)

All oranges 16.1 million boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 16.1 million boxes, increased 100,000 boxes from the February forecast. If realised, this will be 61 percent less than last season’s final production. The forecast consists of 6.10 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 10.0 million boxes of Valencia oranges. A 9-year regression has been used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular and first late bloom. …

Please download the full citrus crop production forecast: www.nass.usda.gov

The processing of the oranges from the 2022/23 crop is beginning to slow down in Brazil, but it is still higher than the usual for this time of the year. In February, five plants – of the large-sized processors – were operating, the same as that last year but much more than that in 2020 and in 2021, when only a single plant was processing oranges.

According to Cepea collaborators, last year, the orange harvest was delayed, which explained the higher volume being processed in February. However, in the 2022/23 season, late processing is due to rains, which are hampering crop activities – although workers manage to get into the groves to harvest oranges, transportation is being difficulted.

The end of processing is still uncertain. Agents from processors reported that planning has been postponed because of the difficulties in crop activities. So far, some plants are expected to continue to process oranges in March.

A frequent concern among agents from processors is the yield of the oranges being harvested, majorly in 2023. They reported that, with frequent rainfall, the quality of the fruits for juice production has decreased, raising the number of boxes needed to the produce a ton of concentrated juice – higher moisture raises water absorption by fruits.

As for prices in the spot market, they were up to BRL 38.00 per 40.8-kilo box (harvested and delivered to processor) in February, considering large-sized companies. At smaller-sized processors, the prices paid for pear and late oranges reached BRL 40.00/box.

For the new crop (2023/24), whose processing is expected to begin in May/June, bids from large-sized processors have been up to BRL 38.00/box. Agents from processors reported that, despite the increase compared to the first bids for the 2022/23 crop, farmers expected higher prices, and, thus, many of them postponed deals.

ORANGE JUICE – Despite the valuation of concentrated orange juice at ICE Futures in recent months, there have not been major reflexes on processors’ revenue. According to Cepea collaborators, most of the juice is being sold through contracts with fixed prices. Since Jan. 1st, the contract due in March has valued 19%%, closing at USD 3,543/ton on Feb. 23rd.

TAHITI LIME – Tahiti lime processing was high in February but is expected to slow down in March. The company that processes tahiti lime aims to receive lower volumes of the fruit in the coming weeks. In February, two plants were receiving tahiti lime, but from March onwards, only one of them is expected to keep activities going. The prices paid by large and small-sized processors for tahiti lime are between BRL 12 and BRL 14/box.

The demand for oranges in the in natura market has been increasing since mid-January. The supply, in turn, is low, especially for out of season pear oranges, which present higher quality compared to others. Therefore, pear orange prices are moving up, operating above BRL 50.00 per 40.8-kilo box (on tree). The average price for pear oranges was at BRL 47.59 per box (on tree) between Feb 13 and 16, for an increase of 3.4 % from that in the week before.

The supply of late fruits is also low, but slightly higher than that for pear oranges, and the ripening level is more advanced, which is leading some purchasers away from trades.

Concerning the tahiti lime, prices are at low levels and have not been enough to cover production costs for most citrus growers. However, in mid-February, players surveyed by Cepea reported a slight price rise because of the firm demand (as the carnaval period was close in Brazil, the demand to prepare drinks usually increases) and of the quality improvement in some areas – fruits that are close to the ideal standard have higher prices. In spite of that, tahiti prices may not recover significantly up to the end of February, since the supply is expected to continue high.

ORANGE JUICE EXPORTS – Brazilian shipments of orange juice continue to increase in the partial of the 2022/23 season (from July/22 to January/23). Secex data indicate that the volume totaled 707.7 thousand tons, 15% up compared to the same period in 2021/22. The revenue totaled USD 1.3 billion, for an increase of 35% in the same comparison.

Updated orange production1 forecast totals 316.23 million boxes

The third 2022-2023 orange crop forecast for the São Paulo and West-Southwest Minas Gerais citrus belt, published on February 10, 2023 by Fundecitrus in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp2 amounted to 316.23 million boxes of 40.8 kg each, a volume 0.7 % higher than the projected scenario in December 2022. This increase is mainly due to the production of the Pera Rio variety, whose harvest is close to the end with higher-than-expected yield. The heavy rains that occurred in the last two months could have further expanded the crop yield, since they contributed to the growth and weight increase of oranges. However, the highly frequent and intense rainfall (many in the form of storms), also significantly intensified the premature fruit drop, offsetting the positive effect of weight gain. This was especially true for the late varieties, as most of these cultivars had not been harvested when the heavy rains started …

1Hamlin, Westin, Rubi, Valencia Americana, Seleta, Pineapple, Alvorada, Pera Rio, Valencia, Valencia Folha Murcha and Natal. 2Department of math and science, FCAV/Unesp Jaboticabal Campus.

All Oranges 16.0 Million Boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 16.0 million boxes, down 2.00 million boxes from the January forecast. If realised, this will be 61 percent less than last season’s final production. The forecast consists of 6.00 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 10.0 million boxes of Valencia oranges. A 9-year regression has been used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular and first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

All oranges 18.0 million boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 18.0 million boxes, down 2.00 million from the December forecast. If realised, this will be 56 percent less than last season’s final production. The forecast consists of 7.00 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 11.0 million boxes of Valencia oranges. A 9-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular bloom and the first late bloom.

Please download the full citrus crop production forecast: www.nass.usda.gov

All Oranges 20.0 Million Boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 20.0 million boxes, down 8.00 million boxes from the October forecast. If realised, this will be 51 percent less than last season’s final production. The forecast consists of 7.00 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 13.0 million boxes of Valencia oranges. A 9-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular bloom and the first late bloom.

Please download the full citrus crop production forecast: www.nass.usda.gov

All Oranges 28.0 Million Boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is carried forward from October at 28.0 million boxes, down 32 percent from last season’s final production. The total includes 11.0 million boxes of non-Valencia oranges (early, midseason, and Navel varieties) and 17.0 million boxes of Valencia oranges. The Navel orange forecast, at 300,000 boxes, accounts for 3 percent of the non-Valencia total. The estimated number of bearing trees for all oranges is 44.0 million. …

Please download the full citrus crop production forecast: www.nass.usda.gov

All Oranges 28.0 Million Boxes

The 2022-2023 Florida all orange forecast released by the USDA Agricultural Statistics Board is 28.0 million boxes, down 32 percent from last season’s final production. The total includes 11.0 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 17.0 million boxes of Valencia oranges. The Navel orange forecast, at 300,000 boxes, accounts for 3 percent of the non-Valencia total.

The estimated number of bearing trees for all oranges is 44.0 million. Trees planted in 2019 and earlier are considered bearing for this season. Field work for the latest Commercial Citrus Inventory was completed in June 2022. Attrition rates were applied to the results to determine the number of bearing trees used to weigh and expand objective count data in the forecast model.

A 9-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular bloom and the first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

The first 2022-2023 orange crop forecast update for the São Paulo and West-Southwest Minas Gerais citrus belt published by Fundecitrus – performed in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp1 –, is 314.09 million boxes of 40.8 kg each. That figure represents a decrease of 2.86 million boxes in relation to the initial estimate published in May this year and corresponds to -0.9 %. Approximately 22.97 million boxes of the total crop are expected to be produced in the Triângulo Mineiro …

Please download the full orange crop forecast update under www.fundecitrus.com.

1Department of math and science, FCAV/Unesp Jaboticabal Campus.

Prognosfruit’s 2022 European apple and pear crop forecast reveals that apple production is set to increase by 1 % compared to 2021, while the upcoming pear crop is estimated to increase by 20 % compared to last year’s record low crop of the decade and by 5 % compared to the 3-year average. On 4 August 2022, more than 200 international representatives from the apple and pear sector joined Prognosfruit 2022 in Belgrade, Serbia, the first in-person Prognosfruit event after two online editions, to discuss the 2022 production forecast for apples and pears.

The World Apple and Pear Association (WAPA) released the 2022/2023 European apple and pear crop estimate on the occasion of the 47th edition of the Prognosfruit, which took place on August 3-5 in Belgrade, Serbia, returning as an in-person event after two years of online editions. Philippe Binard stated: “The apple production in the EU27 and UK is estimated to increase by 1 % to reach 12.167.887 T compared to last year. This year’s crop is also forecasted to be 9 % above the average of 2019-2020- 2021”. The European crop continues its adaptation to the varieties and quality specifications demanded by consumers. Dominik Wozniak, President of WAPA, indicated: “The prospects for the upcoming season are positive, although the sector will have to be prepared to face a variety of challenges including significant rising costs impacting the competitiveness of the sector, intense weather conditions, logistical issues, inflation, and difficulty to secure seasonal workers, with the ultimate goal of increasing consumption thanks to the quality of the products of the season and reverse the recent negative trend”.

Philippe Binard added: ”The EU pear crop for 2022 is estimated to increase by 20 % compared to last year’s record low crop of the decade and by 5 % compared to the 3-year average, rising to 2.077.000 T, mainly due to Italy and France more than doubling their production compared to 2021 (reaching 473.690 T and 137.000 T respectively), although, in the case of the former, the crop remains below its full potential.”. WAPA will continue to monitor the developments of the Northern Hemisphere crop and will issue updates when available.

The 2022 Prognosfruit Conference gathered more than 200 apple and pear sector experts from 23 countries. The event, organised by WAPA and Serbia Does Apples, featured the forecast and market analysis for the European apple and pear market as well as an overview of the latest trends in processing, organic, and the cider market. Luc Vanoideek (COPA COGECA-VBT) commented: “ The Belgrade meeting was the ideal opportunity to learn more about the development in the EU neighbourhood, including Serbia, Moldova, Ukraine, Turkey, as well as the Central Asia and Caucasus region” He further explained: “The additional contributions from representatives of China, India, and the USA provided to the conference a global outreach with the full picture of the whole Northern Hemisphere crop forecast.”

Prognosfruit is the compass for the apple and pear sector. Philippe Binard concluded: “The strong attendance at this first in-person Prognosfruit Conference after two years of online meetings is a clear sign that the sector representatives also very much appreciate the sense of community and networking opportunities that Prognosfruit provides. We look forward to continuing this tradition next year in Trento, Italy from 2 to 4 August 2023”.

Citrus Forecast

The 2021-2022 Florida all orange forecast released today by the USDA Agricultural Statistics Board is 41.0 million boxes. The total is comprised of 18.3 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties), up slightly from the June forecast, and 22.7 million boxes of Valencia oranges, up 1 percent from the June forecast. The forecast of all Florida grapefruit production is up 1 percent at 3.33 million boxes. Of the total grapefruit forecast, 500,000 boxes are white, and 2.83 million boxes are the red varieties. The Florida all tangerine and tangelo forecast remains at 750,000 boxes …

Please download the full citrus crop production forecast: www.nass.usda.gov

The 2022/23 harvesting of early fruits is advancing in São Paulo state. In this scenario, industrial processing activities are following the harvesting pace and requiring more fruits.

According to players from the industry, the ratio of early fruits has improved and practically all fruits have been allowed for delivery, both in the spot market or for contracts. The industrial yield, however, is still low, which is common at the beginning of the crop.

Crushing activities are now taking place in eight processors in São Paulo: Araraquara, Araras, Bebedouro, Catanduva, Colina, Conchal and two in Matão. The companies have already been receiving some volumes of pera orange, but the majority is early fruits – the pera orange availability tends to increase from mid-September onwards.

In the spot market, values are ranging from 27.00 and 28.00 BRL per 40.8-kilo box, on tree, harvested and delivered at the processor. As for contracts, quotations may hit 31.00 BRL per box in big companies. In small processing companies, values are at 35.00 BRL/box.

For marketing year (MY) 2021/22, Post revises its estimates for fresh lemon production to 1.90 million metric tons (MMT), up by 15 percent, due to favourable weather conditions. Fresh orange production is projected to increase to 920,000 metric tons (MT), and fresh tangerine production is expected to increase to 400,000 MT. Recent relatively favourable weather conditions for both sweet citrus fruits have allowed trees to recuperate from a stressful period characterised by drought followed by heavy rains. Lemon exports are projected to increase to 250,000 MT due to larger production, and sweet citrus exports are expected to increase slightly to 65,000 MT for tangerines and to 88,000 MT for oranges. Container availability shortages and higher fleet costs, due to the COVID-19 pandemic and global inflation, are impacting the activity of the Argentine citrus industry, increasing export costs by 100 percent.

The Brazilian orange crop for Marketing Year (MY) 2021/22 is forecast at 414.4 million 40.8-kg boxes (MBx) or 16.91 million metric tons (MMT), an increase of 15 percent vis-à-vis the current season, supported by good weather conditions as of October 2021. Production costs are estimated at over R$ 33,000 per hectare (ha) or US$6,600/ha, up 27 percent compared to the previous crop, supported by high fertiliser, ag chemicals, and diesel prices. Total Brazilian FCOJ 65 Brix equivalent exports for MY 2021/22 are forecast to be relatively stable at 1.04 million metric tons (MT), an increase of 30,000 MT vis-à-vis MY 2020/21 …

Turkey’s citrus production for MY 2021/22 is forecasted up year-over-year in large part due to improved weather conditions compared to the previous year’s hot weather. While production is up, growers are seeing profit margins shrink as input costs, such as fuel and fertiliser, increase at a faster clip than farm gate prices. To cut losses, some grapefruit, orange and mandarin growers opted to leave their crops unharvested. With the exception of oranges, more than 50 percent of Turkey’s citrus production is expected to be exported in MY 2021/22. Looking ahead to MY 2022/23, citrus production will likely decline because of freezing weather that damaged blossoms in March of this year …

On 1 June 2022 World Citrus Organisation (WCO) members gathered for the organisation’s Annual General Meeting (AGM). During the AGM the WCO Secretariat presented the consolidation of the production and export forecasts for the forthcoming Southern Hemisphere citrus season 2022. This preliminary forecast is collected from member industry associations in Argentina, Australia, Bolivia, Brazil, Chile, Peru, South Africa, and Uruguay. Along with citrus market development updates, the meeting also saw the re-election of WCO’s current co-chairs for a second mandate. Both South Africa and Spain, represented by the Citrus Growers’ Association and Ailimpo, were re-elected to head the organisation for another two years.

During WCO’s AGM, the preliminary forecast for the upcoming Southern Hemisphere citrus season was presented to the representatives from the citrus sector. According to the forecast, which is based on information provided by industry associations in Argentina, Australia, Bolivia, Brazil, Chile, Peru, South Africa, and Uruguay, citrus production is expected to increase by 4.85% compared 2021 to reach 24,832,270 tonnes. Exports are also projected to increase to 4,140,547 tonnes, 4.91 % up from the previous season. Philippe Binard, WCO Secretary General, explained, “Following the outbreak of the COVID-19 pandemic, a positive trend of consumers’ demand for fruit and vegetables was noted, in particular for citrus fruit, widely recognised for its high nutritional value, notably in terms of vitamin C content. The large volume available is positive news as it will meet this increased demand”. On the processing side, a total of 13,210,832 tonnes of citrus are expected to be destined to the juice market – an 8.32 % increase compared to 2021.

Orange production is forecasted to increase by 5.01 % compared to 2021, reaching 16,596,973 tonnes. Soft citrus production is expected to remain stable (-0.11 %, 3,044,652 tonnes in total). An 8.28 % growth is projected for lemon production (4,754,260 tonnes in total), while grapefruit production should decrease slightly (-0.58 % compared to 2021, down to 436,386 tonnes). Eric Imbert, CIRAD – Technical Secretariat of WCO, indicated, “The Southern Hemisphere citrus export continues to grow, especially lemons and easy peelers. The Southern Hemisphere today represents 27 % of the global citrus market”. Forecast information was followed by a review of the past season’s results and analysis of the estimations for the current season with a focus on ongoing market challenges, including rising costs and logistics disruptions.

WCO is led by a co-chairmanship of two country full members. Both South Africa and Spain, who have co- chaired the organisation since its inception, were re-elected to head the organisation for a second mandate of two years. South Africa is represented by the Citrus Growers’ Association under the guidance of Justin Chadwick and Spain is represented by Ailimpo under the helm of José Antonio Garcia Fernandez. WCO additionally welcomed new members, with the organisation’s membership now totalling 34 associations and companies.

All Oranges 40.7 Million Boxes

The 2021-2022 Florida all orange forecast released today by the USDA Agricultural Statistics Board is 40.7 million boxes. The total includes 18.2 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 22.5 million boxes of Valencia oranges …

Please download the full citrus crop production forecast: www.nass.usda.gov

The 2022-2023 orange crop forecast for the São Paulo and West-Southwest Minas Gerais citrus belt, published on May 26, 2022 by Fundecitrus in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp, is 316.95 million boxes (40.8 kg). Total orange production includes:

59.48 million boxes of the Hamlin, Westin and Rubi varieties;

17.52 million boxes of the Valencia Americana, Seleta, Pineapple and BRS Alvorada;

93.95 million boxes of the Pera Rio variety;

106.78 million boxes of the Valencia and Valencia Folha Murcha varieties;

39.22 million boxes of the Natal variety.

Approximately 22.99 million boxes are expected to be produced in the Triângulo Mineiro.

The projected volume is 20.53 % higher than the previous crop that totaled 262.97 million boxes and represents an increase of 1.11 % in relation to last ten years’ average, …

Orange production for the 2021-2022 crop season totaled 262.97 million boxes1

The 2021-2022 orange crop for the São Paulo and West-Southwest Minas Gerais citrus belt, published on April 11, 2022, by Fundecitrus – performed in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp2 is 262.97 million boxes of 40.8 kg each. Approximately 23.35 million boxes were produced in West Minas Gerais.

This final figure was 10.61 % smaller than the initially expected volume published in May 2021, corresponding to a significant crop loss of 31.20 million boxes. Although this was an “on-year” for the alternate-bearing, when plants produced a larger amount of fruit, a sharp decrease in rainfall and more intense atypical frosts inhibited the growth of oranges and contributed to an increased early fruit drop, therefore reducing the number of oranges at harvest. Under those conditions, there was a yield loss in groves, which made the crop decrease 2.11 % as compared to the previous one, resulting in a small crop for the second consecutive year. Total orange production included:

47.16 million boxes of the Hamlin, Westin and Rubi early-season varieties;

14.85 million boxes of the Valencia Americana, Seleta and Pineapple early-season varieties;

74.78 million boxes of the Pera Rio mid-season variety;

96.59 million boxes of the Valencia and Valencia Folha Murcha late-season varieties;

29.59 million boxes of the Natal late-season variety.

The May 2021 forecast considered that the yield of groves would be affected due to the lower rainfall volume that was already forecast for 2021. However, forecasts did not point to climate conditions as extreme as those observed, which brought greater than expected damage. The prolonged dry spell turned out to be the worst drought in almost a century, with water shortage in practically all regions of the citrus belt. That critical situation severely impacted rainfed groves, which encompass approximately 70 % of the total area and inevitably rely on rainfall. But even irrigated groves were affected by drought. In many locations, rivers and reservoirs reached the most critical levels ever recorded, restricting water use for irrigation. This crop’s most critical period was from May to September 2021, when accumulated rainfall was almost 70 % below historical average. The scenario started to improve in late September and early October when spring came …

1Hamlin, Westin, Rubi, Valencia Americana, Seleta, Pineapple, Pera Rio, Valencia, Valencia Folha Murcha and Natal. 2Department of math and science, FCAV/Unesp Jaboticabal Campus.

All Oranges 41.2 Million Boxes

The 2021-2022 Florida all orange forecast released by the USDA Agricultural Statistics Board is 41.2 million boxes, down

2.30 million boxes from the February forecast. If realized, this will be 22 percent less than last season’s final production. The forecast consists of 18.2 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 23.0 million boxes of Valencia oranges. A 9-year regression has been used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular and first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

In late February, the large-sized processors in São Paulo made their first purchase proposals for the oranges from the 2022/23 crop. Of the three companies in the state, two of them are interested in closing deals, bidding from BRL 30 – BRL 32.00 per 40.8-kilo box, harvested and delivered. The third processing plant was only renewing existing contracts. However, the number of deals closed is still low, since farmers expect prices to rise higher, due to both firm demand from the industry and, largely, higher production costs.

Indeed, data recently released by CitrusBR show that the volume of orange juice stocked by the end of the current season (in June 2022) will not be enough to supply the international market until the middle of next season. According to CitrusBR, ending stocks of Frozen Concentrate Orange Juice (FCOJ) Equivalent in the 2021/22 season are expected to total 126.574 thousand tons – possibly ranging between 115 and 135 thousand tons. It is important to mention that previous estimates (from September 2021) pointed to stocks between 170 and 190 thousand tons, but bad weather conditions (drought and frosts) reduced processing and hampered fruits development and ripening (influencing industrial yield).

If CitrusBR’s forecasts are confirmed, the volume stocked is expected to be much lower than the strategic level, of 250 thousand tons, scenario that may be observed at least until the end of the 2022/23 season (in June 2023) if the number of oranges produced is not high.

Cepea calculations show that, for stocks to surpass the strategic level by the end of next season, the number of boxes harvested in the citrus belt in São Paulo and the Triângulo Mineiro needs to be over 340 million – and of this total, 300 million need to be allocated to the industry. For these results were considered sales of a million tons (slightly lower than the average) and the average industrial yield of the past five crops.

Although it seems juice supply in Brazil will be tight for at least one more season, agents from processors have not reported any significant valuations for the commodity yet. This would be the major reason why bids for the new season have not been higher. On Feb. 23, the May contract at ICE Futures closed at USD 1,993/ton, 2 % down from that on December 30. However, it is important to mention that values at ICE Futures do not reflect real sales prices of processing plants.

One of the facts that may be constraining juice valuations abroad is the fear of bottling plants as for the negative effects of higher prices in Brazil. In the major destinations for the Brazilian orange juice, the United States and the European Union, demand for the product has been fading for some years, majorly because of the wide variety of other beverages, such as flavoured water, energy drinks and other types of juice, for instance.

On the occasion of its Annual General Meeting, the World Apple and Pear Association (WAPA) has released the Southern Hemisphere apple and pear crop forecast for the upcoming season. According to the forecast, which consolidates the data from Argentina, Australia, Brazil, Chile, New Zealand, and South Africa, apple and pear production is estimated to decrease by 7 % and 6 % respectively in 2022 compared to the previous year.

On 24 February 2022, on the occasion of its Annual General Meeting, the World Apple and Pear Association (WAPA) has released its 2022 apple and pear crop estimate for the Southern Hemisphere. This report has been compiled with the support of ASOEX (Chile), CAFI (Argentina), ABPM (Brazil), Hortgro (South Africa), APAL (Australia) and New Zealand Apples and Pears, and therefore provides consolidated data from the six leading Southern Hemisphere countries. WAPA’s Secretary General Philippe Binard commented “This forecast is released for the global apples and pears sector on the background of many uncertainties, including the geopolitical tension, the increasing costs for production, the impact of the rise of logistic costs and limited container availability, labour shortage and the increasing concerns of declining consumption due to economic situation”

The 2022 Southern Hemisphere apple crop forecast suggests a decrease of 7 % to a total of 4.864.000 T compared to last year (5.217.000 T), mainly due to the 30 % decrease in Brazil and the 11 % decrease in Argentina. Australia and Chile are also forecasted to decrease their production by 3 % and 2 % respectively. New Zealand and South Africa are the only countries where apple production is expected to increase (15 % and 4 % respectively). Chile is expected to remain the largest Southern Hemisphere apple producer in 2022 (1.455.000 T), followed by South Africa (1.163.000 T), Brazil (900.000 T), New Zealand (590.000 T), Argentina (445.000 T), and Australia (311.000 T). With 1.706.000 T, Gala remains by far the most popular variety, although its production is expected to decrease by 7 % compared to 2021. Despite the decrease in production, exports are forecasted to remain stable overall at 1.744.762 T, with the larger volumes exported by New Zealand (+ 17 %) and South Africa (+ 6 %) compensating for the 65 % decrease in Brazilian apple exports.

Regarding pears, the Southern Hemisphere growers predict a 6 % decrease of the crop, which will drop to 1.229.000 T. This is mainly due to the 13 % decrease in Argentina, the 11 % decrease in Chile, and the 6 % decrease in Australia. New Zealand and South Africa, on the other hand, are expected to increase their production by 31 % and 5 % respectively. Argentina remains the largest producer in the Southern Hemisphere (522.000 T), followed by South Africa (492.000 T), Chile (122.000 T), Australia (81.000 T), and New Zealand (11.000 T). Packham’s Triumph remains the most produced variety (444.000 T, despite a 4 % decrease compared to 2021), followed by Williams’ bon chrétien pears (306.000 T). Export figures are expected to decrease by 6 % compared to 2021 to a total of 641.207 T, mainly because of a 14 % decrease in Argentinian exports.

In the Northern Hemisphere, the stocks in the USA stood at 1.478.180 T (- 1 % compared to last year) for apples and 149.553 T for pears (+ 32 % compared to last year) on the 1st of February. In Europe, apple and pear stocks stood at 3.606.980 T (7 % up from last year) and 408.340 T (30 % down from last year). Philippe Binard commented: “Season developments clearly demonstrate the impact of logistics and costs on international trade also for Northern Hemisphere suppliers, with the USA concentrating sales for apples and pears in North America. European markets continue to be affected by the Belarus embargo, while the recent developments in Ukraine will also impact sales to all the destinations in Eastern Europe, including Russia, for all global apples and pears suppliers. It is important to continue building efforts to stimulate the consumption”. WAPA’s Annual General Meeting also hosted a discussion on CO2 emissions and how apple and pear production can reach carbon neutrality or even have a positive contribution to the environment. WAPA will continue to cooperate on this topic with its members in a dedicated working group based on the input and expertise of the University of Bolzano (Italy).

Finally, the Annual General Meeting also confirmed that Prognosfruit will return as an in-person event in the first half of August 2022 in Belgrade (Serbia). The exact date of the event will soon be announced.

All Oranges 43.5 Million Boxes

The 2021-2022 Florida all orange forecast released by the USDA Agricultural Statistics Board is 43.5 million boxes, down 2 percent from the January forecast. If realized, this will be 18 percent less than last season’s final production. The forecast consists of 17.5 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 26.0 million boxes of Valencia oranges. A 9-year regression has been used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular and first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

Orange prices increased in the Brazilian in natura market in the first fortnight of February. According to Cepea collaborators, frequent rains in the citrus belt (São Paulo State) favoured the quality (majorly the size) of oranges, making them suitable for sale in the in natura segment and allowing farmers to raise asking prices. Besides, rainfall also hampered the harvesting, limiting supply. In that scenario, values remained firm.

Usually, orange availability is not high in February – a month that may even be considered offseason –, however, as the 2021/22 season is late, supply is currently higher. Still, there is not an orange surplus in the domestic market, since processing at industries has been faster than usual this month.

So far, the number of early varieties to be harvested is not high – activities are expected to step up only from March onwards. However, supply may be constrained by the low flower set in the first blooming. Thus, the oranges currently available in the in natura market are mostly late varieties and pear oranges out of the ideal period.

TAHITI LIME – The production of tahiti lime is also being favoured by rains, however, farmers reported difficulties to harvest the fruits, which underpinned prices in the first fortnight of February, although it is currently the peak of harvest for tahiti lime in Brazil.

Despite the recent valuations for oranges and tahiti lime, Cepea collaborators have reported that the current economic scenario in Brazil is still constraining higher price rises. With high unemployment and inflation rates and lower income, the purchase power of many consumers is weak.

ESTIMATES – Although rains have favoured the quality of part of the fruits in orchards, they have not been enough to reverse all the damages caused by the drought to the oranges from the 2021/22 season.

According to data from Fundecitrus released on Feb. 10, the orange output (São Paulo + Triângulo Mineiro) in the 2021/22 season is still estimated at 264.14 million boxes of 40.8 kilograms, the same as that estimated in December, but 10 % below that forecast at the beginning of the season.

According to Somar/Climatempo (weather forecast agency), rainfall in SP between May/21 and Jan/22 was 25 % below the average for the period. In the Triângulo Mineiro, rains were 5 % higher than the average. Thus, orange growth was hampered, and the average fruit weight decreased. However, it is important to consider that the oranges harvested in February and in March 2022 are expected to be slightly larger, since they have been favoured by recent rains.

The volume harvested is still enough to replenish ending stocks at the processing plants in SP. According to CitrusBR, by the end of the 2021/22 season (in June 2022), the volume of Frozen Concentrate Orange Juice (Equivalent) stocked is expected to total 170 – 190 thousand tons, lower than the strategic level (250 thousand tons). It is important to consider that new estimates are supposed to be released until the end of February.

In this scenario, the harvest in 2022/23 needs to be large enough to raise stocks at least to the strategic level and thus prevent a world shortage of orange juice. Cepea calculations show that the orange output next season needs to total, at least, 330 million boxes in order to raise juice stocks to 250 thousand tons.

PROGRESS OF THE 2021/22 HARVESTING – According to Fundecitrus’ report, 82 % of the orange orchards had been harvested by mid-January/22, similar to that in the same period last season (81 %).

All oranges 46.0 million boxes

The 2021-2022 Florida all orange forecast released by the USDA Agricultural Statistics Board is 46.0 million boxes, down 1.0 million boxes from the October forecast. If realized, this will be 13 percent less than last season’s final production. The forecast consists of 18.0 million boxes of the non-Valencia oranges (early, mid-season, and Navel varieties) and 28.0 million boxes of the Valencia oranges. A 9-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular bloom and the first late bloom …

Please download the full citrus crop production forecast: www.nass.usda.gov

The current number of flowers in the orange orchards in São Paulo – which will give origin to the fruits from the 2022/23 season – is considered satisfactory in most citrus-producing regions within the state. In general, while in irrigated orchards blooming was observed from September onwards, in non-irrigated orchards, flowers were only observed in October, after the late arrival of rainfall.

Agents have been concerned about the possible effects of the lack of rains this year on the vigor of orange trees, since low moisture may hamper fruit set, increasing the rate of fruitlet fall in irrigated orchards and, largely, in the orchards in dryland.

According to forecasts from the National Oceanic and Atmospheric Administration (NOAA), there is a 90 % chance of La Niña forming in Brazil until the end of 2021. If this is confirmed, rainfall in the coming months may be lower than usual in the southeastern region of the country. However, La Niña is forecast to be weak in Brazil.

This scenario may have a negative influence on the output from the 2022/23 season, since the development stage of plants in the coming months demands good amounts of water. With estimates for low ending stocks of orange juice in the 2021/22 season, the output from 2022/23 needs to be high in order to ensure comfortable inventories for world supply.

Cepea calculations show that, for ending stocks in the 2022/23 season (June 2023) to return to the strategic level of 250 thousand tons, the output next season needs to surpass 330 million boxes of 40.8 kilograms each. In this context, the average productivity would have to be around a thousand boxes per hectare, which has only been observed in seasons favored by the weather.

The World Citrus Organisation (WCO) has released its annual Northern Hemisphere Citrus Forecast for the upcoming season (2021-22). The Forecast, which will be presented during the second edition of the Global Citrus Congress on 16-17 November, is based on data from Egypt, Greece, Israel, Italy, Morocco, Spain, Tunisia, Turkey, the United States and shows that citrus production is projected to reach 29.342.000 T, which represents a 1.27 % decrease compared to the previous season.

The WCO Secretariat has released its annual Northern Hemisphere Citrus Forecast for the upcoming season (2021-22). The preliminary Forecast is based on data from industry associations from Egypt, Greece, Israel, Italy, Morocco, Spain, Tunisia, Turkey, in addition to the United States (based on USDA reports for Arizona, California, Florida, and Texas). Philippe Binard, Secretary General of WCO stated: “The Forecast shows that the 2021-22 Northern Hemisphere citrus crop is projected to reach 29.342.000 T, which represents a 1.27 % decrease compared to the previous season”.

Orange production is projected to decrease by 3.45% to a total of 15.485.106 T. A slight decrease is also expected for grapefruit (-0.34 %, 946.521 T) and soft citrus (-0.70 %, 8.456.112 T) production. Lemon production, on the other hand, is estimated to increase by 5.64 % and reach 4.454.327 T. In Europe Union, citrus production is forecasted to experience a 9.35 % decrease in Greece, a 7.74 % decrease in Spain, and a 2.62 % decrease in Italy. In the Southern rim of the Mediterranean, production is projected to decrease in Tunisia (-21.97 %), remain stable in Egypt (-0.06 %), and increase in Israel (+26.63 %), Turkey (+21.85 %), and Morocco (+5.53 %). The citrus crop in the United States is expected to decrease by 11.79 % compared to last year.

Mr Binard added: “WCO has also engaged for citrus with the China’s Chamber of Commerce for foodstuffs (CFNA) and Ministry of Agriculture (MoA) to collect their estimates. This has overall provided an overview of the Northern Hemisphere covering a grand total of 83.2 Mio T of citrus from the Northern Hemisphere for the next season” This is the result of the forecast in China, for an increase in citrus production by 5.23 %, reaching 53.900.000 T in the upcoming season (volumes not included in NH forecast figures provided in table below).

Natalia Santos-Garcia Bernabe, WCO’s deputy Secretary General stated: “WCO will present its Forecast during the second edition of the Global Citrus Congress, which is organised in cooperation with Fruitnet Media International and the support of CIRAD. The event will stream live on 16-17 November from London, Los Angeles and Melbourne” This is allowing viewers around the globe to pick their most convenient time to take part live or to watch on-demand. Last year’s Congress drew more than 1,300 delegates from 59 countries, bringing together producers, exporters, importers, retailers, and service providers from all over the world. 1075 delegates have already registered to next week’s second edition of the Congress. More information and last minutes’ registration are available on citruscongress.com.

All Oranges 47.0 Million Boxes

The 2021-2022 Florida all orange forecast released by the USDA Agricultural Statistics Board is 47.0 million boxes, down 11 percent from last season’s final production. The total includes 19.0 million boxes of non-Valencia oranges (early, mid-season, and Navel varieties) and 28.0 million boxes of Valencia oranges. The Navel orange forecast, at 450,000 boxes, accounts for 2 percent of the non-Valencia total.

The estimated number of bearing trees for all oranges is 49.4 million. Trees planted in 2018 and earlier are considered bearing for this season. Field work for the latest Commercial Citrus Inventory was completed in June 2021. Attrition rates were applied to the results to determine the number of bearing trees used to weigh and expand objective count data in the forecast model.

A 9-year regression was used for comparison purposes. All references to “average”, “minimum”, and “maximum” refer to the previous 10 seasons, excluding the 2017-2018 season, which was affected by Hurricane Irma. Average fruit per tree includes both regular bloom and the first late bloom. …

Please download the full citrus crop production forecast: www.nass.usda.gov

Estimates about the 2021/22 orange season in the Brazilian citrus belt (São Paulo and the Triângulo Mineiro) have been revised down, due to weather issues in Brazil. Data released by Fundecitrus (Citrus Defense Fund) in September estimated the harvest to be 8.9 % lower than that forecast in the first report, released in May, at 267.87 million boxes. In light of that, the output may be similar to that in the previous season (268.63 million boxes). Although the 2021/22 season is a positive biennial cycle, oranges have been smaller, which explains lower production.

Although the estimates from May considered rainfall below the average, weather issues have increased since then, with frosts and severe drought. Between May and August, rainfall accounted for 30 % of the usual for the period, according to data from Somar/Climatempo Meteorologia (weather forecast agency).

The lack of rains has been damaging majorly the plants in dryland, however, agents from Fundecitrus highlight that even irrigated orchards (which account for 30 % of the trees in the citrus belt) have been debilitated by the drought, due to the limited availability of water at reservoirs. It is important to mention that the scenario has worsened since the frosts in late July.

Besides the smaller size of the oranges, the rate of premature fall of fruits is one of the highest. As the weather is forecast to continue unfavourable until the end of the season, the scenario is not expected to change, raising expectations for low production in 2021/22. Also, the chance of La Niña phenomena to occur until late 2021 is high, which may result in lower rainfall in southeastern Brazil in the second semester. This scenario would limit the growth of late varieties.

INDUSTRY – With the probable lower harvest of oranges in the 2021/22 season, the number of fruits allocated to processors is supposed to be lower too. CitrusBR (Brazilian Association of Citrus Exporters) has not revised processing estimates yet, but Cepea forecasts the industry to purchase around 225 million boxes of oranges (40-8 kilograms each) this season. If this is confirmed and sales of orange juice are near the usual, juice inventories are expected to decrease steeply, to less than 200 thousand tons (Frozen Concentrate Orange Juice Equivalent), even with higher yield at processing plants, which usually happens in years of low rainfall.

This context will demand high orange production in the 2022/23 season (higher than 330 million boxes) so that ending stocks are replenished with no risk of world shortages. This situation may favor the prices paid to farmers in Brazil.

Orange1 production forecast update totals 267.87 million boxes

The first 2021-2022 orange crop forecast update for the Sao Paulo and West-Southwest Minas Gerais citrus belt by Fundecitrus – performed in cooperation with Markestrat, FEA-RP/USP and FCAV/Unesp2 – is 267.87 million boxes of 40.8 kg each, differently from the 294.17 million estimated in May this year. The reduction of 26.30 million in relation to the initial expectation corresponds to – 8.9 %. The main reason for this crop loss is the poorer rainfall regime constituting the most severe water crisis ever to hit Brazil for the last 91 years3. The combination of this drought never before experienced by citriculture and successive frosts in July culminated in a gradual crop decline that has been seen as harvests progress and disclose totally atypical figures. Field surveys also show results other than expected for this time of the year for orange planted areas yet to be harvested. In general, oranges are excessively small, and early fruit drop reaches one of its highest rates. These factors make production go back to the same levels of last crop season that totaled 268.63 million boxes, despite fruit load being 12.50 % larger since this is an “on” year. In view of this data and the perspective of climate conditions remaining adverse until harvests end, fruit should present the most critical size and drop rate in historical data. If this scenario is confirmed, there will no longer be an increase in this crop in relation to the previous season, estimated at 9.51 % in May, but rather a smaller volume than the production in the last season (- 0,28 %). …

1Hamlin, Westin, Rubi, Valencia Americana, Seleta, Pineapple, Pera Rio, Valencia, Valencia Folha Murcha and Natal. 2Department of math and science, FCAV/Unesp Jaboticabal Campus. 3National operator of the energy system – ONS. Data for the Parana River basin, encompassing the states of São Paulo, Minas Gerais, Paraná, Santa Catarina, Rio Grande do Sul, Mato Grosso do Sul, Goiás and Distrito Federal.

Prognosfruit’s 2021 European apple and pear crop forecast revealed that while apple production is set to increase by 10 %, the upcoming pear crop is expected to decrease by 28 %. On 5 August 2021, more than 150 international representatives from the apple and pear sector joined the Prognosfruit 2021 Online Conference, the second virtual edition of the event in its 46 years, to discuss the 2021 production forecast for apples and pears.

Philippe Binard (Photo: freshfel)

The World Apple and Pear Association (WAPA) released the 2021/2022 European apple and pear crop estimate on the occasion of the 46th edition of the Prognosfruit. WAPA Secretary General Philippe Binard stated: “The apple production in the EU for the 21 top producing countries contributing to this report is estimated for the 2021/2022 season to be 11.735,000 T. Overall, this year’s crop is estimated to be 10 % higher than last year, but 1 % only up from the 3-year average. It is therefore perceived to be a season with a balanced outlook”.

Philippe Binard added ”While the EU apple crop is larger, the EU pear crop for 2021/2022 is estimated to decrease by 28 % compared to last year to 1.604.000 T and by 27 % compared to the three-year average. This is the smallest decade crop for pears” On the varieties, this translates into a decrease of Conference pear by 18% to 805.000 T. Abate is also impacted with a crop reduced to 66.000 T, down by 73 %”.

WAPA will continue to monitor the developments of the Northern Hemisphere crop and will issue updates when available.

The 2020-2021 Florida all orange forecast released by the USDA Agricultural Statistics Board is 52.8 million boxes. The total is comprised of 22.7 million boxes of non-Valencia oranges (early, midseason, and Navel varieties), unchanged from the June forecast, and 30.1 million boxes of Valencia oranges, up slightly from the June forecast. The forecast of all Florida grapefruit production is unchanged at 4.10 million boxes. Of the total grapefruit forecast, 620,000 boxes are white, and 3.48 million boxes are the red varieties. The Florida all tangerine and tangelo forecast remains at 890,000 boxes …

Please download the full citrus crop production forecast: www.nass.usda.gov

All Oranges 52.7 Million Boxes

The 2020-2021 Florida all orange forecast released by the USDA Agricultural Statistics Board is raised 1.0 million boxes to 52.7 million boxes. The total includes 22.7 million boxes of the non-Valencia oranges (early, mid-season, and Navel varieties) and 30.0 million boxes of Valencia oranges. …

Please download the full citrus crop production forecast: www.nass.usda.gov

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.