AGRANA Group recently confirmed its annual guidance on 10 October 2024 in the context of publishing its results for the first half of 2024/25. Significantly lower EBIT* was forecast for the 2024/25 financial year compared to the prior year (2023/24: € 151.0 million), with a decline of 10 % to 50 %.

It had already been communicated that, due to higher sugar inventories and sharply falling sugar prices (in the EU and globally), AGRANA’s Sugar segment in particular would continue to face very challenging times in the coming months. Since the full-blown start of the sugar beet processing campaign in October 2024, it has also become evident that the campaign costs of the new 2024/25 sugar marketing year will be higher than expected. In the meantime, the evaluation of September’s flooding damages (primarily in Austria) has also been largely completed. The negative impact on earnings in the current financial year has been higher than originally forecast, mainly due to the production stoppage at the plant in Pischelsdorf, Austria, in the Starch segment.

These developments are primarily responsible for the forecast now that the 2024/25 financial year will be characterised by a very significant decline in EBIT* of more than 50 % at the Group level. The operating profit before exceptional items and results of equity-accounted joint ventures is expected to be in the range of € 55 million to € 75 million.

The publication of the results for the first three quarters of 2024/25, including details of the outlook for all segments in the remainder of the 2024/25 financial year, will be on 14 January 2025 as scheduled.

*EBIT: operating profit after exceptional items and results of equity-accounted joint ventures

Stephan Büttner (Photo: AGRANA)

In the first quarter of the 2024/25 financial year (the three months ended 31 May 2024), AGRANA, the fruit, starch and sugar company, generated operating profit (EBIT) of € 32.3 million, a significant reduction of 49.1 % from the first quarter of the prior year. Revenue eased slightly, by 2.3 %, to € 944.3 million. “After the robust results of the full year 2023/24, as expected we had a weaker start to the 2024/25 financial year. The significant decline in profit resulted from the highly challenging market environment in the Sugar and Starch segments, where sales prices fell. Business in the Fruit segment was better, leading to a significant increase in Fruit EBIT,” says AGRANA Chief Executive Officer Stephan Büttner.

Results in each business segment for the first quarter of 2024/25

FRUIT segment

The Fruit segment’s revenue in the first quarter was € 415.6 million, up 3.6% from the same period one year earlier. The increase occurred both in the fruit preparations and fruit juice concentrate businesses and resulted from volume growth.

EBIT of the segment as a whole grew to € 27.0 million in the first three months of the financial year (Q1 prior year: € 24.4 million). In the fruit preparations activities, EBIT was significantly above the year-ago level. The improvement was attributable partly to a positive business performance in the Europe region (including Ukraine) and in Mexico.

STARCH segment

Revenue in the Starch segment in the first quarter was € 265.5 million, a reduction of 16.3% from the year-earlier comparative period (Q1 prior year: € 317.1 million), when the war in Ukraine had led to powerful increases in market prices. Owing to the decline in raw material and energy prices, market prices for the segment’s products decreased noticeably year-on- year, which impacted the selling prices obtained for the entire Starch portfolio. Ethanol sales prices, for instance, fell by about 25 % amid a substantial drop in Platts quotations.

At € 9.4 million, EBIT in the Starch segment was down very significantly year-on-year. A key reason for this was the margin decline in starch and saccharification products driven by significantly lower sales prices for core and by-products.

SUGAR segment

Sugar segment revenue was € 263.2 million, up 6.2 % from the first quarter of the previous year. The negative effect of lower sugar sales prices was more than made up for by higher sales volumes. The trajectory of the sugar market was most recently driven by the sugar imports from Ukraine and the expectation of increased EU sugar production in the 2024/25 campaign.

The Sugar EBIT result in the financial first quarter was a deficit of € 4.1 million, a pronounced deterioration from the year-earlier period. This reflected especially the significant fall in sugar selling prices, which was steepest in the regions heavily affected by the imports of Ukrainian sugar.

Outlook

For the full 2024/25 financial year, AGRANA expects a significant reduction in operating profit (EBIT) compared to the previous year. Group revenue is projected to show a moderate decrease.

Total investment across the three business segments in the 2024/25 financial year, at approximately € 120 million, is to be moderately below the 2023/24 value and in line with budgeted depreciation. About 12 % of this capital expenditure will be for emission reduction measures in the Group’s own production operations under the AGRANA climate strategy.

Based on provisional results, AGRANA generated operating profit (EBIT) of € 151.0 million in its 2023/24 financial year (1 March 2023 to 29 February 2024), which is in line with its guidance of a very significant improvement compared to the prior year (2022/23: € 88.3 million). Earnings per share rose to € 1.04 (prior year: € 0.25).

Consolidated revenue amounted to € 3,786.9 million (prior year: € 3,637.4 million).

As previously communicated in the Q3 results published in January 2024, AGRANA sees itself confronted with an increasingly challenging business environment since the fourth quarter of 2023/24 and forecasts EBIT for the 2024/25 financial year which will be significantly below the comparable figure in 2023/24. This decline in results will already become apparent in the first quarter of 2024/25.

The Management Board of AGRANA Beteiligungs-AG has today also decided – subject to a corresponding resolution passed by the Supervisory Board – to propose a dividend payout in the amount of € 0.90 per share for the 2023/24 financial year (dividend for 2022/23: € 0.90 per share) to the 37th Annual General Meeting to be held on 5 July 2024. This corresponds to a dividend yield of 6.7 % based on the closing price on the balance sheet date (29 February 2024).

The publication of the Annual Report 2023/24 and all the details relating to the annual results for 2023/24 and to the outlook for 2024/25 will take place as scheduled on 14 May 2024.

In the first quarter of the 2023/24 financial year (the three months ended 31 May 2023), AGRANA, the fruit, starch and sugar company, achieved very significant growth of 23.1 % in operating profit (EBIT) to EUR 63.5 million. Revenue increased by 9.0 % to EUR 966.1 million. “We have made a successful start to the 2023/24 financial year and are especially pleased with the continuing healthy profit trend in the Sugar segment and the good performance in the Fruit segment, where structural measures to boost profitability of the fruit preparations business are already producing results. In the Starch segment, the expectation of a challenging financial year was proved correct in the first three months. EBIT declined significantly in this business segment, due especially to a lower ethanol performance driven by sales prices,” explains AGRANA CEO Markus Mühleisen.

Results in each business segment for the first quarter of 2023/24

Fruit segment

The Fruit segment’s revenue in the first quarter was EUR 401.1 million, up 11.2 % from one year earlier. The revenue expansion both in the fruit preparations and fruit juice concentrate businesses was the result of price changes. EBIT of the segment as a whole increased to EUR 24.4 million in the first three months of the financial year (Q1 prior year: EUR 19.9 million). The earnings result in fruit preparations was significantly above the year-ago level. The improvement was attributable mainly to a positive business performance in the Europe region. The fruit juice concentrate business as well further grew its earnings compared to the already very good year-earlier quarter. This was driven by improved contribution margins of apple juice concentrate made from the 2022 crop.

Starch segment

The Starch segment’s revenue of EUR 317.1 million in the first quarter was steady year-on-year (Q1 prior year: EUR 319.1 million), as lower sales volumes coincided with higher selling prices. Across most product categories, customers now are not fully utilising sales contracts that were concluded in fall and winter 2022 against the backdrop of the then-prevailing tight availability and resulting high market prices. Demand for native and modified food starches as well as saccharification products is more restrained, even in the normally stable food market. Many customers are facing weaker consumption and are increasingly running down their inventories. At EUR 22.1 million, EBIT in the Starch segment was down significantly from one year earlier (Q1 prior year: EUR 29.3 million). A key reason lay in the low-margin ethanol business, as a result of a considerable decline in Platts quotations.

Sugar segment

Revenue in the Sugar segment was EUR 247.9 million, up 20.0 % from the first quarter of the previous year. This growth was driven by a substantial increase in sugar selling prices. EBIT, at EUR 17.0 million, represented a marked improvement from the year-earlier period. The Sugar segment’s very good EBIT in the first quarter of 2023|24 reflected the significantly increased sugar sales prices in particular, as well as many reorganisation measures taken previously.

Positive consolidated EBIT guidance for the full 2022|23 financial year remains unchanged

Besides the ongoing war in Ukraine and the volatility on energy and commodity markets, the rising costs of capital in particular necessitated an impairment test of the cash generating unit Fruit to coincide with the end of the first half year (31 August 2022). This resulted in non-cash impairments of assets and goodwill in the amount of € 91.3 million on the operating profit (EBIT) in the first half year 2022|23 (1 March to 31 August 2022).

The operating profit before any exceptional items and results of equity-accounted joint ventures of the Group in H1 2022|23 was better than anticipated and, at € 86.5 million, was considerably higher than the prior year level (H1 2021|22: € 41.0 million). One of the drivers of the strong operational performance was the improvement in ethanol operations. It was also possible to return the Sugar segment to profitability. Revenue in H1 2022|23 rose by nearly 26 % to € 1,792.3 million.

The guidance of a very significant increase (by more than +50%) in consolidated EBIT in the full financial year 2022|23 remains valid despite the asset and goodwill impairment charge (EBIT 2021|22: € 24.7 million). A significant increase (ranging from +10% to +50%) in the operating profit before any exceptional items and results of equity-accounted joint ventures is forecast (operating result 2021|22: € 86.5 million).

The above guidance is based on assumptions that the war in Ukraine remains regional, physical supplies of energy and other commodities are sustained and that the sharp rises in prices, particularly in the commodities and energy sectors, can be passed on in revised customer contracts.

In the first three quarters of the 2021/22 financial year (the nine months ended 30 November 2021), AGRANA, the fruit, starch and sugar company, generated an operating profit (EBIT) of EUR 76.0 million (Q1-Q3 prior year: EUR 84.3 million). Revenue was EUR 2,169.6 million (Q1-Q3 prior year: EUR 1,965.3 million).

Markus Mühleisen (Photo: AGRANA)

AGRANA Chief Executive Officer Markus Mühleisen says: “Since the beginning of the financial year we have been forecasting that, after a weaker first six months of 2021/22, earnings in the second half of the year would be better than one year earlier. This outlook was confirmed in the third quarter with quarterly EBIT of EUR 31.2 million (Q3 prior year: EUR 28.5 million). Following this positive trend in Q3, we also expect a very significant year-on-year improvement in EBIT in the fourth quarter. We therefore remain optimistic that, for the full financial year, we will exceed the prior year’s EBIT significantly, i.e., by at least 10 %. Getting there has, however, become much more difficult in the past few months amid a very strong rise in raw material and energy prices.”

Results in each business segment

Fruit segment

Fruit segment revenue in the first three quarters grew to EUR 939.1 million, a moderate increase of 5.3 %. The fruit preparations business saw revenue growth stemming mostly from higher sales prices. Revenue in the fruit juice concentrate activities declined slightly for volume reasons. Segment EBIT in the first nine months was EUR 36.2 million, off 12.3 % from one year earlier. The principal reason for the deterioration lay in weaker sales of fruit juice concentrates from the 2020 crop, which were marked by reduced delivery volumes in combination with lower contribution margins of apple juice concentrates in the first half of 2021/22.

Starch segment

Revenue in the Starch segment in the first three quarters of 2021/22 was EUR 737.8 million, or a significant 18.8 % more than a year ago. Higher volumes of core products and by-products were demanded than in the same period of the prior year. In the ethanol business, Platts quotations reached historic highs in the third quarter and averaged 24 % stronger in the first three quarters of 2021/22 than in the prior-year comparable period. Segment EBIT in the first nine months, at EUR 53.5 million, eased by 8.5 % from the year-earlier level. The main reason was a significant year-on-year increase in prices for raw materials (wheat and corn/maize) and energy, which could not yet be fully offset by adjusting product prices.

Sugar segment

The Sugar segment’s revenue in the first three quarters of 2021/22 grew to EUR 492.7 million, up 8.8 % from one year earlier. In addition to renewed high sales volumes with resellers, there was also a recovery in the industrial customer segment, where more sugar was sold than in the same period last year. While the EBIT result in the first three quarters of 2021/22 was better than in the year-ago period, it remained negative at the nine-month mark, at a deficit of EUR 13.7 million. This still reflected the fact that AGRANA’s own sugar production had been below average after the pest-related small 2020 harvest, with a resulting lower margin from the necessary compensatory reselling and refining of sugar.

Outlook

For the full 2021/22 financial year, AGRANA continues to expect significant growth in Group EBIT, in other words, an EBIT increase of at least 10 %. Group revenue is projected to show moderate growth. It should be noted, however, that due to the extreme volatility in commodity and energy prices and a once again more acute COVID-19 situation – the fourth wave in combination with the advent of the new Omicron variant – the forecast for the full year is subject to a very high degree of uncertainty.

In the 2021/22 financial year, the AGRANA Group is investing EUR 92 million, an amount significantly less than the budgeted depreciation of about EUR 120 million.

Group EBIT target for full year unchanged

At € 31.2 million (Q3 2020|21: € 28.5 million), the consolidated EBIT of AGRANA Beteiligungs-AG in the third quarter of 2021/22 (1 September to 30 November 2021) was higher than expected. The key driver was considerably higher revenues in the Starch segment due to an all-time high of ethanol prices.

As a result, in the first three quarters of 2021/22 (1 March to 30 November 2021), AGRANA generated earnings before interest and tax (EBIT) of € 76.0 million (Q1-3 2020|21: € 84.3 million). Group revenue amounted to € 2,169.6 million (Q1-3 2020|21: € 1,965.3 million).

The guidance for the full financial year 2021/22, according to which Group EBIT will increase significantly, remains unchanged; the forecast is for earnings before interest and tax to rise by at least 10 %.

Due to the extreme volatility in terms of commodity and energy prices as well as the COVID-19 situation again intensifying – the fourth wave in combination with the appearance of the Omikron variant – the forecast for the full year is characterised by a very high degree of uncertainty.

Further details relating to the development of business in the first three quarters of 2021/22 and more information about the various segments will be published by the Group as scheduled on 13 January 2022.

To date, AGRANA had been expecting an overall annual EBIT in 2020/21 of at least € 87.1 million. Following a provisional review of the figures, the Group is now expected to achieve provisional earnings before interest and tax (EBIT) in its 2020/21 financial year in an amount of € 78.7 million (prior year: € 87.1 million). Group revenue will amount to around € 2,550 million (2019/20: € 2,480.7 million).

Besides the anticipated, significantly weaker, operating performance in the fourth quarter 2020|21, extraordinary items in the fruit preparations business are the main reason why EBIT in 2020|21 is below the level of the prior year.

The 2020/21 annual report will be published as planned on 11 May 2021.

Forecast: EBIT at least matching prior-year level

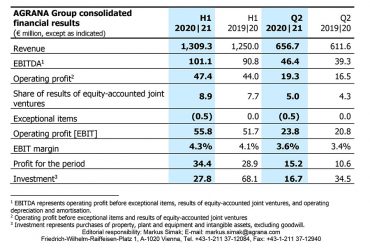

AGRANA, the fruit, starch and sugar company, generated operating profit (EBIT) of € 55.8 million in the first half of the 2020|21 financial year, a moderate increase of 7.9 % year-on-year (H1 prior year: € 51.7 million). The Group’s revenue rose slightly to € 1,309.3 million (H1 prior year: € 1,250.0 million).

AGRANA Chief Executive Officer Johann Marihart says: “Much of our positive business performance can be credited to the diversification of our business activities, which enables us to balance out fluctuating economic conditions in the various segments. Thus, in the first half of the year, the Starch segment was able to maintain the prior year’s EBIT earnings despite significantly weaker starch sales in the paper sector, thanks to the very strong performance in bioethanol especially in the second quarter.”

Helping make the year-on-year growth in Group EBIT possible was the Sugar segment, which, as in the first quarter, saw a year-on-year improvement in earnings in the second quarter as a result of higher sugar prices. The Sugar segment’s EBIT nonetheless remained negative. In the Fruit segment, AGRANA was able to hold earnings in the fruit preparations business in line with the first half of the prior year. The performance of the fruit juice concentrate business was down significantly due to lower available volumes from the 2019 apple crop.

(All Photos: Agrana)

Net financial items amounted to an expense of € 9.1 million (H1 prior year: expense of € 7.9 million). After an income tax expense of € 12.3 million, corresponding to a tax rate of about 26.3 % (H1 prior year: 34.0 %), profit for the period was € 34.4 million (H1 prior year: € 28.9 million). Earnings per share attributable to AGRANA shareholders increased to € 0.54 (H1 prior year: € 0.43).

Net debt at 31 August 2020 amounted to € 479.6 million, up € 15.6 million from the year-end level of 29 February 2020 (year-ago level of 31 August 2019: € 423.6 million). The gearing ratio rose accordingly to 36.1 % as of the quarterly balance sheet date (29 February 2020: 33.5 %; 31 August 2019: 31.2 %).

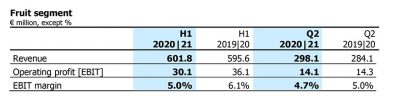

The Fruit segment’s revenue in the first half of 2020|21 rose slightly year-on-year, by 1.0 %. In the fruit preparations business, revenue remained stable despite somewhat lower sales volumes. Revenue in the fruit juice concentrate activities saw an increase from a year ago, thanks largely to higher prices for apple juice concentrate produced from the 2019 crop. EBIT of the Fruit segment was off 16.6 % from the first half of 2019|20. The reason for the deterioration lay in lower delivery volumes in the fruit juice concentrate business combined with reduced contribution margins for apple juice concentrate from the 2019 harvest.

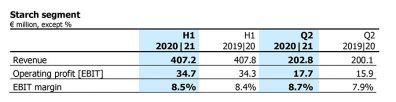

Starch segment revenue in the first half of 2020|21 was steady at the prior-year level. With the full operation of the new, second wheat starch plant, sales volumes and revenues of the products manufactured in-house increased. At the same time, revenue from resold merchandise declined sharply, as the sale of sugar by-products is now charged on a commission basis and the corresponding sales are no longer included in the Starch segment’s revenue. Ethanol quotations, after collapsing in March 2020 amid the COVID-19 lockdown and the steep fall in demand for petrol, recovered again progressively especially in the second financial quarter and even reached a new all-time high in August. Sales volumes of saccharification products, on the other hand, were negatively affected by the COVID-19 crisis, particularly with the beverage industry.

EBIT in the Starch segment slightly exceeded the year-earlier result, by 1.2 %. The earnings were driven by the high selling prices for ethanol, which made up for the lower market demand for starch and starch products.

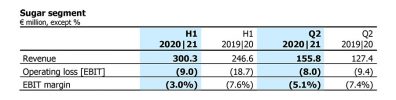

The Sugar segment’s revenue in the first half of 2020|21 was up 21.8 % from one year earlier. This growth was attributable both to higher sugar selling prices and increased sugar sales volumes, especially with food retailers. Although EBIT was still negative, it marked a substantial improvement from the same period of the prior year due to a more benign sales price environment.

Outlook

Taking into account potential impacts of the coronavirus crisis, AGRANA expects Group EBIT for the full 2020|21 financial year to at least match the prior-year level. Group revenue is projected to show slight to moderate growth of up to 10%. Due to the ongoing COVID-19 pandemic and the associated high volatility in all business segments, this forecast remains characterised by a very high degree of uncertainty. It also does not yet include any financial effects of a possible closure of the sugar plant in Leopoldsdorf, Austria, after the 2020 campaign.

The drive to secure grower contracts with beet farmers is underway, with the aim of increasing next year’s beet cultivation area in Austria to at least 38,000 hectares by the middle of November 2020. With a three-year contract and guaranteed minimum prices, AGRANA is offering farmers long-term predictability for beet cultivation. Depending on the contracting status in mid-November, a decision will be made on whether to continue operations at the Leopoldsdorf factory or close it down after the end of the campaign.

In the 2020|21 financial year, the AGRANA Group’s investment is expected to amount to € 73 million, which is significantly below the year’s depreciation of about € 120 million following the very high capital expenditure of prior years.

Despite more challenging growth conditions Chr. Hansen delivers a strong EBIT margin and a healthy cash flow, while also making significant progress on key strategic priorities

CEO Mauricio Graber says: “2018/19 was a solid year for Chr. Hansen, although it was not without its challenges as tougher market conditions especially in emerging markets made it more difficult to grow to the level of our ambition. We ended the year with 7 % organic growth for the group, at the low end of the guidance provided in June. However, we are satisfied that we delivered well on the financial targets for EBIT margin and free cash flow that we set at the beginning of the year, with EBIT margin before special items reaching 29.6 % and 17 % growth in free cash flow before acquisitions and special items. For the full year, Food Cultures & Enzymes delivered solid organic growth of 8 %, while Health & Nutrition delivered 9 % and Natural Colors delivered 3 %. In Q4, organic growth came down as expected for all three business areas, as we continued to see macroeconomic challenges in emerging markets, primarily impacting Food Cultures & Enzymes and Natural Colors.

We made very good progress on our strategic priorities: Plant Health had a very strong year in Latin America, and is set to have another strong year, selling in both Latin America and North America. We’ve reached an important milestone for our Human Microbiome lighthouse with the Bacthera joint venture, and while bioprotection did not have a very strong year, it still delivered double-digit growth, and we are confident in the commercial pipeline and have accelerated the development of the 3rd generation technology.

We have a cautious outlook for 2019/20, given the market challenges we are facing. After a first quarter with flat to low-single digit growth, we expect to improve the momentum in Food Cultures & Enzymes and Health & Nutrition for the rest of the year to end at 4-8 % organic growth for the group, with an EBIT margin on par with 2018/19 and an improved operating cash flow.

Over the next six months, we will conduct our biennial review of the Nature’s no. 1 strategy and will present the results at a Capital Markets Day in April 2020. Given our strong belief in the opportunities inherent in the strategy, fundamental changes from our focus on microbial and natural solutions produced via fermentation should not be expected. Until then, our business focus in 2019/20 will be to improve on our execution of the strategy.”

Bioprotection continues to show impressive momentum

Chr. Hansen reports strong organic revenue growth of 10 % in the first three months of 2017/18: Food Cultures & Enzymes 12 %, Health & Nutrition 10 % and Natural Colors 4 %. EBIT before special items decreased by 1 % to EUR 65 million, corresponding to an EBIT margin before special items of 25.4 %. The overall outlook for 2017/18 is unchanged.

CEO Cees de Jong says: “We have had a solid start to the year, with Food Cultures & Enzymes’ organic growth better than expected. Sales of bioprotective solutions continue to show impressive momentum, and this is still without any significant impact from the second-generation FreshQ® products that we launched at the beginning of this financial year. We have also introduced ProKids®, an innovative product concept for a children’s drinking yogurt containing our LGG® probiotic strain. As expected, organic sales growth in Natural Colors was below our long-term ambition.

“Our EBIT margin before special items in Q1 was lower than last year, mainly due to the sale of a property in Argentina in Q1 2016/17, adverse currency impacts and costs related to starting up our new production capacity in Copenhagen. The new capacity is producing ahead of schedule, and we expect to see improving margins from this toward the end of the financial year.

“We are encouraged by the solid start to the year, and we maintain our overall guidance for the full year. We increase our expectations to organic growth for Food Cultures & Enzymes to be even stronger and above the long term 7 – 8 % growth target that we have for this business. At the same time, we lower our expectations to organic growth in Health & Nutrition for the full year to be below our long term guidance for this business due to the challenging market conditions in North America.”

You are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.