The resilience of the global economy is being tested by the evolving conflict in the Middle East, which has generated new inflationary pressures while creating significant uncertainty, according to the OECD’s latest Interim Economic Outlook.

Global growth was steady heading into 2026, supported by the strength of technology-related production, lower effective tariffs on US imports and the momentum carried over from 2025. The energy supply shock following the onset of the conflict in the Middle East is expected to significantly weigh on global growth while putting new upward pressure on inflation.

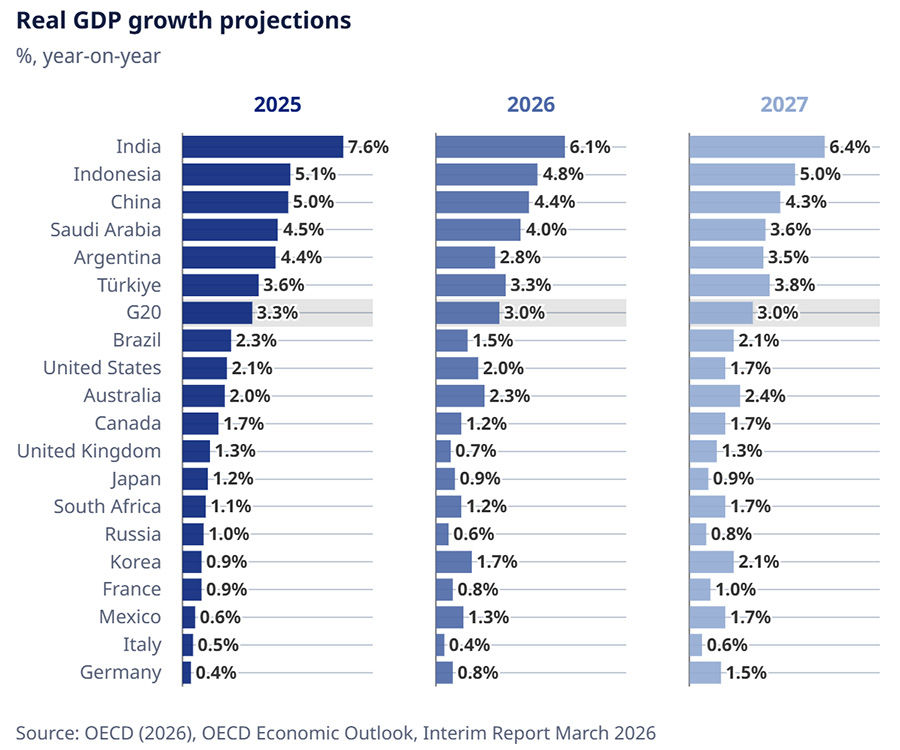

As a result of these developments, the Outlook projects global growth of 2.9 % in 2026 and 3.0 % in 2027. The evolution of the conflict in the Middle East is highly uncertain and poses considerable risks to these baseline projections. A more long-lasting disruption, with energy prices remaining elevated beyond mid-2026, would further reduce growth prospects.

GDP growth in the United States is projected at 2.0 % in 2026, before moderating to 1.7 % in 2027. In the euro area, growth is projected to be 0.8 % in 2026 and 1.2 % in 2027. China’s growth is projected to slow to 4.4 % in 2026 and 4.3 % in 2027.

Inflation pressures will persist for a longer period, with inflation now expected to be higher in 2026 than previously projected, reflecting the surge in global energy prices. Headline inflation in G20 countries is projected to be 4.0 % in 2026, easing to 2.7 % in 2027.

(Photo: OECD)

“The energy supply shock from the evolving conflict in the Middle East is testing the resilience of the global economy. We project global growth will remain robust, but it will be slower than the pre-conflict trajectory, with significantly higher inflation,” OECD Secretary-General Mathias Cormann said. “Any policy measures adopted to cushion the impact of the energy price shock should be targeted towards those most in need, temporary, and ensure incentives to save energy are preserved. Increasing renewable energy generation and energy efficiency can enhance economic security while boosting resilience to future price shocks.”

The Outlook highlights a range of risks. The expected decline in future energy prices is based on assumptions that current disruptions to supply will ease over time, and be limited in 2027. Longer-lasting closure of oil and gas production facilities in the region or persistent disruptions to exports through the Strait of Hormuz would likely have more significant adverse consequences on energy prices, inflation expectations and future growth.

The Outlook points out that higher energy and fertiliser prices could spur increases in food prices, particularly affecting vulnerable households. Higher energy prices could also increase the cost for European countries carrying out necessary annual replenishing of natural gas stocks. Financial markets may experience additional volatility while rising long-term sovereign yields increase fiscal risks.

Given these challenges, the Outlook highlights key priorities for policymakers. Central banks should remain vigilant and ensure expectations are well-anchored. Stronger efforts are needed to safeguard the sustainability of public finances. Any measures to cushion the economic impact of the energy shock will need to be targeted, temporary and take into account limited fiscal space facing most governments. Lowering trade barriers would boost output and reduce inflationary risks. Over the medium term, improving energy efficiency and reducing dependency on fossil fuel imports can lower exposure to future supply shocks.

In an increasingly complex global landscape shaped by inflation, rising tariffs, and political volatility, consumer behavior is undergoing a profound transformation. Cost-of-living pressures and trade policy disruptions are not only fueling economic anxiety but also prompting tangible shifts in how and why consumers shop. These forces are accelerating a move toward value-driven decision-making, increased scrutiny of product origin, and a growing preference for local alternatives, according to the Q1 2025 consumer survey* by GlobalData, a leading data and analytics company.

Concerns over trade-related inflation are widespread. More than half (56 %) of global consumers say they are “extremely” or “quite concerned” about the impact of trade wars and import tariffs on the prices of the products they buy. This concern is even more pronounced in countries directly affected by US trade policy, including Canada (66 %) and Mexico (62 %). Despite being at the center of trade friction, China stands out for its lower levels of concern, with 40% of respondents saying they are not worried about tariffs, highlighting regional differences in public perception and economic insulation.

Prerana Manral, Senior Consumer Analyst at GlobalData, comments: “These concerns are not abstract. They are driving tangible changes in consumer behavior across everyday categories such as food, drinks, toiletries, clothing, and homewares. According to the survey, 54 % of consumers are now checking or comparing prices online before making a purchase, and 47 % are switching to cheaper brand alternatives.

“Private labels are seeing a notable rise, with 33% of consumers saying they are buying more store-owned brands to manage costs. Additionally, 38 % of shoppers are turning to discount retailers or cheaper outlets, while nearly one-third (32 %) have stopped buying certain products altogether because they have become too expensive.”

Manral continues: “Trade policy is no longer just an economic lever; it’s a force that is reshaping everyday consumer choices. What we’re seeing is a structural shift in how people engage with brands and pricing. Consumers are now making sharper, more value-conscious decisions, and many are actively abandoning higher-priced products or stores.”

Beyond pricing responses, the survey highlights a growing ideological and environmental awareness in consumer preferences, particularly around product origin. On average, 68 % of the respondents globally say they prefer to buy local products: 67 % cite price, or 65 % say environmental friendliness, as the main reasons, while 71 % say they do so to support local brands.

Political sentiment is also playing an influential role, with 58 % of global consumers* reporting that recent political events have made them more attentive to the country of origin of products they purchase. This intersection of cost-consciousness and conscious consumerism is emerging as a powerful force in a politically volatile economy. While affordability remains the entry point, values such as environmental impact and national loyalty are increasingly determining purchasing behavior.

Manral concludes: “As consumers increasingly respond to rising tariffs and price pressures by shifting toward local products and value-driven alternatives, FMCG companies must recognize this as a long-term behavioral shift rather than a temporary adjustment. To remain competitive and relevant, brands should invest in localized sourcing and production, expand affordable and private-label offerings, and strengthen communication around value, sustainability, and origin.”

*GlobalData 2025 Q1 global consumer survey, 22,000 respondents across 42 countries.

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.