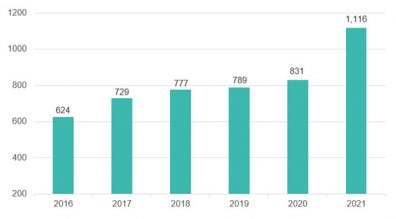

2021 was another record year for food and drink industry transactions, with 1,116 registered on the Zenith Global mergers and acquisitions database, an average of 21 each week.

The total is 34 % more than in 2020 and 79 % higher than 5 years ago. The number has risen every year since a dip in 2013. Funding rounds for early stage businesses have become an increasingly important element.

GLOBAL FOOD AND DRINK ACQUISITIONS 2016-21 (Photo: Zenith Global)

The most active sectors were ingredients on 97, packaging on 96, soft drinks on 56 and dairy on 54.

GLOBAL FOOD AND DRINK ACQUISITIONS BY SECTOR 2020-21 (Photo: Zenith Global)

The top 15 sectors saw some significant changes in 2021. Packaging, plant-based and vertical farming deals more than doubled, with plant-based rising 9 places to the top 5. Meat-free entered the top 10, outpacing meat.

Vertical farming, food delivery and CBD moved up to the top 15, while services, water drinks and beer dropped out.

The combination of plant-based (48), meat-free (41), cell-based (24), dairy-free (20), alcohol-free (10) and plant-based seafood (5) would make free-from by far the biggest category overall on 148, 13 % of the total. Water drinks (23) and water dispense (18), when taken together at 41, would come 8th.

5 categories had declared transaction values in excess of $10 billion. These were packaging, food delivery, ingredients, plant-based and dairy.

8 more categories exceeded $5 billion – fresh produce, nutrition, meat, soft drinks, snacks, equipment, water drinks and tea.

Meat-free surpassed USD2 billion, while vertical farming and cell-based both exceeded USD1 billion.

GEA Group presented end of September ist „Mission 26“ strategy in London as part of its Capital Markets Day. The plan for the next five years defines seven key levers to accelerate sustainable, profitable growth. The focus is on sustainability, innovation and digital solutions, New Food, as well as excellence initiatives in sales, service and operations. The company is also looking at targeted acquisitions.

“We have set ourselves the goal of being at the forefront of the mechanical and plant engineering industry,” says Stefan Klebert, CEO GEA. “We take it upon ourselves to protect future generations by offering sustainable solutions for the food and pharmaceutical industries. In these attractive markets, we want to continue to grow profitably while contributing to a better world, as anchored in our purpose – engineering for a better world.”

Ambitious financial targets set for 2026

“Mission 26” sets ambitious financial targets for 2026. Organic sales growth of 4.0 to 6.0 percent per year is expected, leading to sales of around EUR 6 billion (FY 2020: EUR 4.635 billion). The EBITDA margin before restructuring expenses is projected to grow to a record level of more than 15 percent (FY 2020: 11.5 %). The Group-wide return on capital employed (ROCE) is anticipated to increase significantly to over 30 percent (FY 2020: 17.1 %).

In the context of further targets, a stable ratio of net working capital to sales of 8.0 to 10.0 percent is expected by 2026. Capital expenditure (CAPEX) is projected to be around EUR 200 million annually until 2026. Overall, this leads to strong free cash flow generation of around EUR 2 billion from 2022 until 2026.

“We are creating significant value for our shareholders through 2026 and beyond,” says Marcus Ketter, CFO. “Our shareholders will participate in this success with sustainable dividend increases.”

Holistic climate and sustainability approach

In June 2021, GEA presented its interim targets for reducing its own greenhouse gas emissions alongside its net zero ambition for 2040. Greenhouse gas emissions in Scopes 1 and 2 are to be reduced by 60 percent and in Scope 3 by 18 percent by 2030 (base year 2019). The Science Based Targets initiative (SBTi), the globally recognized independent body for reviewing climate targets, validated GEA’s CO2 reduction targets in September 2021. SBTi thus confirms that GEA’s interim targets follow the latest climate science and make an effective contribution to achieving the 1.5-degree Celsius target of the Paris Climate Agreement

In addition to the climate targets already communicated, GEA has set ambitious ESG targets. Combined, these measures focus on environmentally sustainable customer solutions and responsible operations. Furthermore, GEA aims to be the employer of choice in the industry.

“Sustainability is firmly anchored in the company’s DNA and is therefore also an essential part of Mission 26,” says Klebert. “With our ambitious approach, we help our customers achieve their own environmental goals. Likewise, we strive for the highest standards in our operations and support our employees in developing their skills. In this way, we live up to our social responsibility and ensure GEA’s lasting success.”

GEA drives product innovation with R&D and digitalization

“Innovation & Digitalization” are also expected to make a significant contribution to realizing the goals of “Mission 26”. Here, GEA aims to increase the proportion of sales of products that are less than five years old – from the current level of 10 percent to about 30 percent. To fuel this development, GEA will increase its research & development spending by approximately 45 percent over the next few years.

In addition to introducing new products, GEA will offer customers more digital solutions to further enhance their processes and GEA machine efficiency. To drive the digital customer journey and the development of digital solutions forward, these competencies haven been combined under the newly created position of Chief Digital Officer (CDO), effective August 1, 2021.

Growth market New Food: GEA with unique position

In the dynamically growing New Food market, GEA will expand its already strong position and become a market leader. Here, the company intends to leverage its strengths in scaling industrial applications and its unique position as a full-line supplier. GEA anticipates order intake for newly developed and existing machines from this segment to exceed EUR 400 million per year by 2026. “Consumer expectations around food are changing. For example, environmental impact and animal welfare are increasingly prioritized, and demand for high-quality, protein-rich foods is growing rapidly. GEA is optimally positioned to meet this demand,” explains Klebert.

GEA has already demonstrated its strength in this dynamic market by winning one of the largest orders in the company’s history: Novozymes, the world’s largest supplier of enzyme and microbial technologies in Denmark, is entrusting GEA with the turnkey fitting of a large-scale plant in the U.S. to produce plant-based proteins.

Excellence initiatives in sales, service and operations

Further growth opportunities for “Mission 26” lie in sales, service, purchasing and production. In GEA’s regions and countries, sales effectiveness and presence will be better exploited by deploying more of the company’s own sales staff in key markets. Sales of new machines are expected to grow by 4.0 to 5.0 percent per year until 2026.

Further growth potential was also identified in the service area, which is a resilient and profitable business for GEA. The aim is to increase coverage and expand the service business with customers by 2026, thereby boosting recurring revenue. This approach is expected to generate annual organic revenue growth of 5.0 to 6.0 percent in the service business until 2026.

The optimization measures announced at the 2019 Capital Markets Day impacting purchasing, production and logistics will be continued. In the process, purchasing activities were bundled in a central purchasing organization, the production network was improved, and greater flexibility was created at sites. The aim is to enable a transition to best-in-class procurement by 2026, further optimize the production network and reduce delivery times to customers.

“Global Operations is undergoing a comprehensive and long-term transformation process,” explains Johannes Giloth, COO GEA: “In addition to cost reductions, this also involves creating structures for further growth. In this way, Global Operations will continue to have a significant positive impact on profitability in the future.” Between 2022 and 2026, further optimizations in purchasing (EUR 90 million) and production (EUR 60 million) are expected to have a total net impact on EBITDA of EUR 150 million.

GEA examines possible acquisitions

Strong cash generation and a solid balance sheet will enable external growth. GEA will therefore examine value-enhancing acquisitions to strengthen its portfolio.

Outlook for business development in 2021 and 2022 confirmed

GEA confirms the guidance for fiscal year 2021 that was raised in July 2021. Organic growth of 5.0 to 7.0 percent is expected for revenue. EBITDA before restructuring expenses at constant exchange rates is anticipated to be in a range between EUR 600 million and EUR 630 million. The outlook for ROCE at constant exchange rates is likely to be in the range between 23 to 26 percent.

At the Capital Markets Day in September 2019, GEA communicated its targets up to 2022. In March 2021, when the annual figures for 2020 were presented, GEA adjusted its medium-term financial targets for 2022 upwards. GEA has confirmed these again. Group revenue is expected to grow by an average of 2.0 to 3.0 percent annually from 2019 until 2022, the EBITDA margin before restructuring expenses is to increase to a target corridor of 12.5 to 13.5 percent (Capital Markets Day 2019: 11.5 to 13.5 percent) and the ratio of net working capital to revenue is to be reduced to the range between 8.0 and 10.0 percent (Capital Markets Day 2019: 12.0 to 14.0 percent).

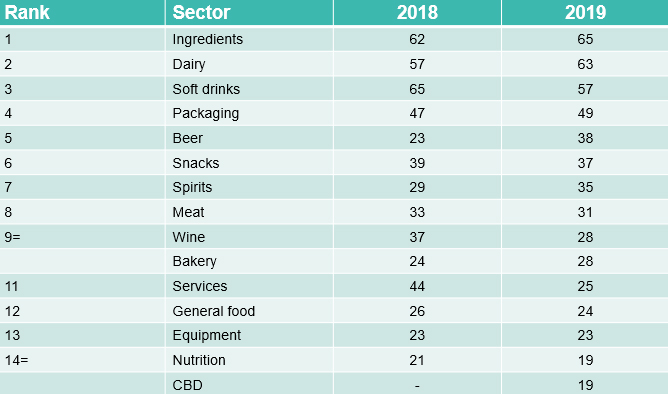

2019 broke records again for the number of food and drink transactions around the world, with 789 registered on the Zenith Global mergers and acquisitions database, an average of 15 each week.

The total is 12 more than in 2018 and 41 % higher than 5 years ago. The number has increased every year since a dip in 2013.

The most active sectors were ingredients on 65, dairy on 63, soft drinks on 57 and packaging on 49. Beer on 38 was ahead of spirits on 35 and wine on 28.

Global food and drink acquisitions by sector 2018-2019 (Photo: Zenith Global)

The top 15 sectors were the same as 2018, with the exception of CBD replacing confectionery. The combination of plant-based (15) with dairy-free (14) and meat-free (11) totalled 40. Bottled water and water coolers added up to 23. Vertical farming was a newcomer with 8.

The biggest increases were for CBD (+19) and beer (+15). Many of the main categories saw declines, led by services (-19), confectionery (-18) and wine (-9).

Europe’s drinks industry saw a rise of 73.9 % in overall deal activity during Q2 2019, when compared to the four-quarter average, according to GlobalData, a leading data and analytics company.

A total of 40 deals worth $76.18m were announced for the region during Q2 2019, against the last four-quarter average of 23 deals.

Of all the deal types, merger and acquisition (M&A) saw the most activity in Q2 2019 with 24, representing a 60 % share for the region.

In second place was venture financing with ten deals, followed by private equity deals with six transactions, respectively capturing a 25 % and 15 % share of the overall deal activity for the quarter.

In terms of value of deals, M&A was the leading category in Europe’s drinks industry with $55.98m, while venture financing deals totaled $20.2m.

Europe drinks industry deals in Q2 2019: Top deals

The top five drinks deals accounted for 80.9 % of the overall value during Q2 2019.

The combined value of the top five drinks deals stood at $61.65m, against the overall value of $76.18m recorded for the quarter. The top announced drinks deal tracked by GlobalData in Q2 2019 was Cafento Coffee Factory S.L’s $33.58m acquisition of Java Republic.

In second place was the $20.39m asset transaction with The Glenturret by Lalique Group and in third place was Five Seasons Ventures and New Ground Ventures’ $4.73m venture financing of YFood Labs.

The $1.68m venture financing of Champagne EPC by Cedric Sellin, Cedric Sire and Kima Ventures and AG Barr’s stake acquisition of Elegantly Spirited for $1.27m held fourth and fifth positions, respectively.

Out of a record 777 food and drink transactions covered by the bevblog.net mergers and acquisitions database for 2018, 28 involved sums over USD 1,000 million. This was below the 33 recorded in 2017, but higher than the numbers for 2015 and 2016.

The USD 104 billion combined value of the top 10 was 36 % higher than the USD 77 billion for the top 10 of 2017, but 39 % lower than the USD 171 billion for the top 10 of 2016 and little more than a quarter of the USD 365 billion for the top 10 of 2015.

The 28 over USD 1 billion totalled USD 141 billion, compared with USD 115 billion for the 33 over USD 1 billion in 2017, USD 190 billion for the 22 over USD 1 billion in 2016 and USD 403 billion for the 27 over USD 1 billion in 2015.

2017 was another record year for food and drink industry transactions, with 727 registered in the bevblog.net mergers and acquisitions database, an average of almost 14 each week.

The total is 103 more than in 2016 and 40 % higher than five years ago. The number has increased each year apart from a dip in 2013.

The most active sectors were dairy on 72, ingredients and soft drinks on 68, then packaging on 54. Beer on 40 was ahead of spirits on 37 and wine on 30.

The top 15 sectors were the same as 2016, with the exception of plant-based replacing bottled water.

Plant-based deals quadrupled (+13), with nutrition up 121 % (+17), meat up 67 % (+16), snacks up 52 % (+11), ingredients up 36 % (+18) and dairy up 24 % (+14). Wine activity dropped by 36 % (-17) and packaging by 16 % (-10).